In economics, a recession is a business cycle contraction that occurs when there is a general decline in economic activity. Recessions generally occur when there is a widespread drop in spending. This may be triggered by various events, such as a financial crisis, an external trade shock, an adverse supply shock, the bursting of an economic bubble, or a large-scale anthropogenic or natural disaster.

The early 1990s recession describes the period of economic downturn affecting much of the Western world in the early 1990s. The impacts of the recession contributed in part to the 1992 U.S. presidential election victory of Bill Clinton over incumbent president George H. W. Bush. The recession also included the resignation of Canadian prime minister Brian Mulroney, the reduction of active companies by 15% and unemployment up to nearly 20% in Finland, civil disturbances in the United Kingdom and the growth of discount stores in the United States and beyond.

The National Bureau of Economic Research (NBER) is an American private nonprofit research organization "committed to undertaking and disseminating unbiased economic research among public policymakers, business professionals, and the academic community". The NBER is known for proposing start and end dates for recessions in the United States.

A jobless recovery or jobless growth is an economic phenomenon in which a macroeconomy experiences growth while maintaining or decreasing its level of employment. The term was coined by the economist Nick Perna in the early 1990s.

The early 2000s recession was a decline in economic activity which mainly occurred in developed countries. The recession affected the European Union during 2000 and 2001 and the United States from March to November 2001. The UK, Canada and Australia avoided the recession, while Russia, a nation that did not experience prosperity during the 1990s, began to recover from it. Japan's 1990s recession continued.

The early 1980s recession was a severe economic recession that affected much of the world between approximately the start of 1980 and 1982. It is widely considered to have been the most severe recession since World War II until the 2007–2008 financial crisis.

Growth Recession is a term in economics that refers to a situation where economic growth is slow, but not low enough to be a technical recession, yet unemployment still increases.

The Great Moderation is a period in the United States of America starting from the mid-1980s until at least 2007 characterized by the reduction in the volatility of business cycle fluctuations in developed nations compared with the decades before. It is believed to be caused by institutional and structural changes, particularly in central bank policies, in the second half of the twentieth century.

The Great Recession was a period of marked general decline observed in national economies globally, i.e. a recession, that occurred in the late 2000s. The scale and timing of the recession varied from country to country. At the time, the International Monetary Fund (IMF) concluded that it was the most severe economic and financial meltdown since the Great Depression. One result was a serious disruption of normal international relations.

The Depression of 1920–1921 was a sharp deflationary recession in the United States, United Kingdom and other countries, beginning 14 months after the end of World War I. It lasted from January 1920 to July 1921. The extent of the deflation was not only large, but large relative to the accompanying decline in real product.

The 1990s economic boom in the United States was an economic expansion that began after the end of the early 1990s recession in March 1991, and ended in March 2001 with the start of the early 2000s recession during the Dot-com bubble crash (2000–2002). It was the longest recorded economic expansion in the history of the United States until July 2019.

The 1973–1975 recession or 1970s recession was a period of economic stagnation in much of the Western world during the 1970s, putting an end to the overall post–World War II economic expansion. It differed from many previous recessions by involving stagflation, in which high unemployment and high inflation existed simultaneously.

The Economic Cycle Research Institute (ECRI) based in New York City, is an independent institute formed in 1996 by Geoffrey H. Moore, Anirvan Banerji, and Lakshman Achuthan. It provides economic modeling, financial databases, economic forecasting, and market cycles services to investment managers, business executives, and government policymakers.

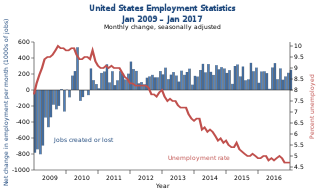

Unemployment in the United States discusses the causes and measures of U.S. unemployment and strategies for reducing it. Job creation and unemployment are affected by factors such as economic conditions, global competition, education, automation, and demographics. These factors can affect the number of workers, the duration of unemployment, and wage levels.

In the United States, the Great Recession was a severe financial crisis combined with a deep recession. While the recession officially lasted from December 2007 to June 2009, it took many years for the economy to recover to pre-crisis levels of employment and output. This slow recovery was due in part to households and financial institutions paying off debts accumulated in the years preceding the crisis along with restrained government spending following initial stimulus efforts. It followed the bursting of the housing bubble, the housing market correction and subprime mortgage crisis.

The United States entered recession in January 1980 and returned to growth six months later in July 1980. Although recovery took hold, the unemployment rate remained unchanged through the start of a second recession in July 1981. The downturn ended 16 months later, in November 1982. The economy entered a strong recovery and experienced a lengthy expansion through 1990.

The early 1990s recession saw a period of economic downturn affect much of the world in the late 1980s and early 1990s. The economy of Australia suffered its worst recession since the Great Depression.

In macroeconomics, the Sahm rule, or Sahm rule recession indicator, is a heuristic measure by the United States' Federal Reserve for determining when an economy has entered a recession. It is useful in real-time evaluation of the business cycle and relies on monthly unemployment data from the Bureau of Labor Statistics (BLS). It is named after economist Claudia Sahm, formerly of the Federal Reserve and Council of Economic Advisors.

{kind=link}