Related Research Articles

MCI, Inc. was a telecommunications company. For a time, it was the second-largest long-distance telephone company in the United States, after AT&T. WorldCom grew largely by acquiring other telecommunications companies, including MCI Communications in 1998, and filed for bankruptcy in 2002 after an accounting scandal, in which several executives, including CEO Bernard Ebbers, were convicted of a scheme to inflate the company's assets. In January 2006, the company, by then renamed MCI, was acquired by Verizon Communications and was later integrated into Verizon Business.

Ernst & Young Global Limited, trade name EY, is a multinational professional services partnership. EY is one of the largest professional services networks in the world. Along with Deloitte, KPMG and PwC, it is considered one of the Big Four accounting firms. It primarily provides assurance, tax, information technology services, consulting, and advisory services to its clients.

Certified Public Accountant (CPA) is the title of qualified accountants in numerous countries in the English-speaking world. It is generally equivalent to the title of chartered accountant in other English-speaking countries. In the United States, the CPA is a license to provide accounting services to the public. It is awarded by each of the 50 states for practice in that state. Additionally, all states except Hawaii have passed mobility laws to allow CPAs from other states to practice in their state. State licensing requirements vary, but the minimum standard requirements include passing the Uniform Certified Public Accountant Examination, 150 semester units of college education, and one year of accounting-related experience.

Forensic accounting, forensic accountancy or financial forensics is the specialty practice area of accounting that investigates whether firms engage in financial reporting misconduct, or financial misconduct within the workplace by employees, officers or directors of the organization. Forensic accountants apply a range of skills and methods to determine whether there has been financial misconduct by the firm or its employees.

Equity Funding Corporation of America was a Los Angeles-based U.S. financial conglomerate that marketed a package of mutual funds and life insurance to private individuals in the 1960s and 70s. It collapsed in scandal in 1973 after former employee Ronald Secrist and securities analyst Ray Dirks blew the whistle on massive accounting fraud, including a computer system dedicated exclusively to creating and maintaining fictitious insurance policies. Investigation found that from 1964 onward, as many as 100 company employees had engaged in organized deception of investors, auditors, reinsurers and regulatory authorities.

Institute of Chartered Accountants of India (ICAI) is India's largest professional accounting body under the administrative control of Ministry of Corporate Affairs, Government of India. It was established on 1 July 1949 as a statutory body under the Chartered Accountants Act, 1949 enacted by the Parliament for promotion, development and regulation of the profession of Chartered Accountancy in India.

Accounting ethics is primarily a field of applied ethics and is part of business ethics and human ethics, the study of moral values and judgments as they apply to accountancy. It is an example of professional ethics. Accounting was introduced by Luca Pacioli, and later expanded by government groups, professional organizations, and independent companies. Ethics are taught in accounting courses at higher education institutions as well as by companies training accountants and auditors.

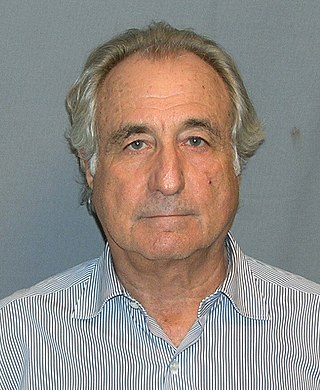

Bernard Lawrence Madoff was an American financial criminal and financier who was the admitted mastermind of the largest known Ponzi scheme in history, worth an estimated $65 billion. He was at one time chairman of the Nasdaq stock exchange. Madoff's firm had two basic units: a stock brokerage and an asset management business; the Ponzi scheme was centered in the asset management business.

Marc Stuart Dreier is an American former lawyer who was sentenced to 20 years in federal prison in 2009 for committing investment fraud using a Ponzi scheme. He is scheduled to be released from FCI Sandstone on June 30, 2025. On May 11, 2009, he pleaded guilty in the United States District Court for the Southern District of New York to eight charges of fraud, which included one count of conspiracy to commit securities fraud and wire fraud, one count of money laundering, one count of securities fraud, and five counts of wire fraud in a scheme to sell more than $950 million in fictitious promissory notes. Civil charges, filed in December 2008 by the U.S. Securities and Exchange Commission, are pending. The 2011 documentary Unraveled states that "Drier stole over $740 million from 4 clients, 4 individuals, and 13 hedge funds".

The Satyam Computer Services scandal was India's largest corporate fraud until 2010. The founder and directors of India-based outsourcing company Satyam Computer Services, falsified the accounts, inflated the share price, and stole large sums from the company. Much of this was invested in property. The swindle was discovered in late 2008 when the Hyderabad property market collapsed, leaving a trail back to Satyam. The scandal was brought to light in 2009 when chairman Byrraju Ramalinga Raju confessed that the company's accounts had been falsified.

Frank DiPascali Jr. was an American fraudster and financier who was a key lieutenant of Bernie Madoff for three decades. He referred to himself as the company's "director of options trading" and as "chief financial officer". For a number of years, he played a key part in the daily operation of the Madoff investment scandal, later recounting how he helped manipulate billions of dollars in account statements so clients would believe that they were creating wealth for them.

Ira Lee Sorkin is an American attorney. He is best known for representing Bernard Madoff, the American businessman who pleaded guilty to perpetrating the largest investor fraud ever committed by a single person.

The Madoff investment scandal was a major case of stock and securities fraud discovered in late 2008. In December of that year, Bernie Madoff, the former Nasdaq chairman and founder of the Wall Street firm Bernard L. Madoff Investment Securities LLC, admitted that the wealth management arm of his business was an elaborate multi-billion-dollar Ponzi scheme.

Participants in the Madoff investment scandal included employees of Bernard Madoff's investment firm with specific knowledge of the Ponzi scheme, a three-person accounting firm that assembled his reports, and a network of feeder funds that invested their clients' money with Madoff while collecting significant fees. Madoff avoided most direct financial scrutiny by accepting investments only through these feeder funds, while obtaining false auditing statements for his firm. The liquidation trustee of Madoff's firm has implicated managers of the feeder funds for ignoring signs of Madoff's deception.

The recovery of funds from the Madoff investment scandal has been underway since the scandal broke in December 2008. That month, recovery trustee Irving Picard received funds from the Bank of New York account where Bernard Madoff held new investments into his Ponzi scheme. As it has been concluded that no legitimate investments were made on the investors' behalf for at least the last 12 years of operation, recovery has proceeded on a "money in/money out" basis. Investors are entitled to receive no more than the nominal cash amounts that they paid in and did not subsequently withdraw, without regard to inflation, interest, opportunity cost or the false statements that Madoff provided them. Those statements combined to a total balance of approximately $64 billion, while the admitted claims amount to $19.5 billion. As of March 2023, the trustee had recovered $14.6 billion toward these claims through legal action against Madoff associates, feeder funds and beneficiaries of the scheme, and had made fourteen distributions to investors. Action by the Department of Justice has recovered an additional $4 billion.

Accounting scandals are business scandals which arise from intentional manipulation of financial statements with the disclosure of financial misdeeds by trusted executives of corporations or governments. Such misdeeds typically involve complex methods for misusing or misdirecting funds, overstating revenues, understating expenses, overstating the value of corporate assets, or underreporting the existence of liabilities; these can be detected either manually, or by the means of deep learning. It involves an employee, account, or corporation itself and is misleading to investors and shareholders.

Daniel Bonventre is one of five former Madoff employees charged in the Madoff investment scandal.

Whether providing services as an accountant or auditor, a certified public accountant (CPA) owes a duty of care to the client and third parties who foreseeably rely on the accountant's work. Accountants can be sued for negligence or malpractice in the performance of their duties, and for fraud.

Shana Diane Madoff, sometimes referred to as Shana Madoff Skoller Swanson, is an American former attorney who is now a yoga teacher.

The WorldCom scandal was a major accounting scandal that came into light in the summer of 2002 at WorldCom, the USA's second-largest long-distance telephone company at the time. From 1999 to 2002, senior executives at WorldCom led by founder and CEO Bernard Ebbers orchestrated a scheme to inflate earnings in order to maintain WorldCom's stock price.

References

- ↑ "Free Birthday Database". Birthdatabase.com. November 27, 1959. Retrieved February 22, 2013.

- ↑ Chung, Joanna (March 22, 2009). "Madoff investigation is far from over - FT.com". Financial Times. Retrieved March 22, 2009.

- ↑ Steve Israel (March 22, 2009). "Madoff mess has local link". recordonline.com. Retrieved February 22, 2013.

- ↑ "Securities and Exchange Commission v. David G. Friehling, Friehling & Horowitz, CPAs, P.E." (PDF). United States District Court, Southern District Of New York. March 2009. Retrieved September 25, 2015.

This article incorporates text from this source, which is in the public domain .

This article incorporates text from this source, which is in the public domain . - 1 2 Hamblett, Mark. Madoff's Accountant Acknowledges Guilt, Casts Himself as Victim. New York Law Journal, November 4, 2009.

- ↑ Arrested Madoff accountant had Palm Beach Gardens partner. Palm Beach Post, March 4, 2009.

- 1 2 3 4 5 Ross, Brian (2015). The Madoff Chronicles. Kingswell. ISBN 9781401310295.

- ↑ Fitzgerald, Jim. Madoff's financial empire audited by tiny firm: one guy. Associated Press via Seattle Times, December 18, 2008.

- ↑ Markopolos, Harry (March 2010). No One Would Listen: A True Financial Thriller. Hoboken, New Jersey: John Wiley & Sons. ISBN 978-0-470-55373-2.

- 1 2 Abkowitz, Alyssa (December 17, 2008). "Madoff's auditor... doesn't audit?". CNN. Retrieved March 22, 2009.

{{cite journal}}: Cite journal requires|journal=(help) - ↑ Voreacos, David (December 16, 2008). "New York Prosecutor Drops Madoff Auditor Probe; Defers to U.S." Bloomberg News . Retrieved December 24, 2008.

- ↑ Dugan, Ianthe Jeanne; Crawford, David (February 18, 2009). "Accounting Firms That Missed Fraud at Madoff May Be Liable". The Wall Street Journal. Retrieved March 22, 2009.

- ↑ "Madoff trustee suit against JPMorgan Chase" (PDF). The Wall Street Journal. Retrieved February 22, 2013.

- ↑ Bray, Chad (July 18, 2009). "Madoff Ex-Auditor Friehling Enters a Plea of Not Guilty". The Wall Street Journal.

- 1 2 Lieberman, Steve. Sentencing of Madoff's New City auditor put off again. The Journal News, 2014-07-04.

- ↑ Pavlo, Walter (September 16, 2011). "David Friehling, Madoff's Accountant, Sentencing Postponed....Again". Forbes.

- ↑ United States v. David Friehling – Court’s Order Adjourning Sentencing to Sept. 3, 2010, United States v. David G. Friehling, The United States Department of Justice, retrieved July 25, 2010

- ↑ Pavlo, Walter (April 18, 2012). "Before Prison – Future Inmates Get in Their Vacation". Forbes. Retrieved February 22, 2013.

- ↑ Lieberman, Steve. Friehling remains free, testifying in Madoff Ponzi scam. The Journal News, 2014-12-15.

- 1 2 Matthew Goldstein, Madoff Accountant Avoids Prison Term, New York Times (May 28, 2015).

- ↑ "Press Release: SEC Charges Madoff Auditors With Fraud; 2009–60; March 18, 2009". Sec.gov. March 18, 2009. Retrieved February 22, 2013.

- ↑ Efrati, Amir (March 19, 2009). "Accountant Arrested for Sham Audits". The Wall Street Journal.

- 1 2 Lisa Cornell, Jeremy Friehling, Son of Bernard Madoff's Accountant, Kills Himself in Ohio, Huffington Post (November 18, 2012).

- ↑ "Son of Madoff's accountant a suicide in Ohio". USA TODAY. Retrieved September 30, 2023.