A tax is a compulsory financial charge or some other type of levy imposed on a taxpayer by a governmental organization in order to collectively fund government spending, public expenditures, or as a way to regulate and reduce negative externalities. Tax compliance refers to policy actions and individual behaviour aimed at ensuring that taxpayers are paying the right amount of tax at the right time and securing the correct tax allowances and tax relief. The first known taxation took place in Ancient Egypt around 3000–2800 BC. Taxes consist of direct or indirect taxes and may be paid in money or as its labor equivalent.

A flat tax is a tax with a single rate on the taxable amount, after accounting for any deductions or exemptions from the tax base. It is not necessarily a fully proportional tax. Implementations are often progressive due to exemptions, or regressive in case of a maximum taxable amount. There are various tax systems that are labeled "flat tax" even though they are significantly different. The defining characteristic is the existence of only one tax rate other than zero, as opposed to multiple non-zero rates that vary depending on the amount subject to taxation.

An income tax is a tax imposed on individuals or entities (taxpayers) in respect of the income or profits earned by them. Income tax generally is computed as the product of a tax rate times the taxable income. Taxation rates may vary by type or characteristics of the taxpayer and the type of income.

A regressive tax is a tax imposed in such a manner that the tax rate decreases as the amount subject to taxation increases. "Regressive" describes a distribution effect on income or expenditure, referring to the way the rate progresses from high to low, so that the average tax rate exceeds the marginal tax rate.

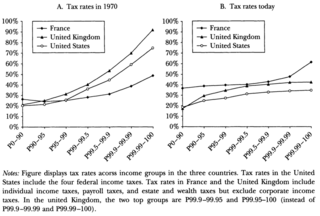

A progressive tax is a tax in which the tax rate increases as the taxable amount increases. The term progressive refers to the way the tax rate progresses from low to high, with the result that a taxpayer's average tax rate is less than the person's marginal tax rate. The term can be applied to individual taxes or to a tax system as a whole. Progressive taxes are imposed in an attempt to reduce the tax incidence of people with a lower ability to pay, as such taxes shift the incidence increasingly to those with a higher ability-to-pay. The opposite of a progressive tax is a regressive tax, such as a sales tax, where the poor pay a larger proportion of their income compared to the rich

In a tax system, the tax rate is the ratio at which a business or person is taxed. The tax rate that is applied to an individual's or corporation's income is determined by tax laws of the country and can be influenced by many factors such as income level, type of income, and so on. There are several methods used to present a tax rate: statutory, average, marginal, flat, and effective. These rates can also be presented using different definitions applied to a tax base: inclusive and exclusive.

An indirect tax is a tax that is levied upon goods and services before they reach the customer who ultimately pays the indirect tax as a part of market price of the good or service purchased. Alternatively, if the entity who pays taxes to the tax collecting authority does not suffer a corresponding reduction in income, i.e., the effect and tax incidence are not on the same entity meaning that tax can be shifted or passed on, then the tax is indirect.

A consumption tax is a tax levied on consumption spending on goods and services. The tax base of such a tax is the money spent on consumption. Consumption taxes are usually indirect, such as a sales tax or a value-added tax. However, a consumption tax can also be structured as a form of direct, personal taxation, such as the Hall–Rabushka flat tax.

Income tax in Australia is imposed by the federal government on the taxable income of individuals and corporations. State governments have not imposed income taxes since World War II. On individuals, income tax is levied at progressive rates, and at one of two rates for corporations. The income of partnerships and trusts is not taxed directly, but is taxed on its distribution to the partners or beneficiaries. Income tax is the most important source of revenue for government within the Australian taxation system. Income tax is collected on behalf of the federal government by the Australian Taxation Office.

Tax policy refers to the guidelines and principles established by a government for the imposition and collection of taxes. It encompasses both microeconomic and macroeconomic aspects, with the former focusing on issues of fairness and efficiency in tax collection, and the latter focusing on the overall quantity of taxes to be collected and its impact on economic activity. The tax framework of a country is considered a crucial instrument for influencing the country's economy.

The Fair Tax Act is a bill in the United States Congress for changing tax laws to replace the Internal Revenue Service (IRS) and all federal income taxes, payroll taxes, corporate taxes, capital gains taxes, gift taxes, and estate taxes with a national retail sales tax, to be levied once at the point of purchase on all new goods and services. The proposal also calls for a monthly payment to households of citizens and legal resident aliens as an advance rebate of tax on purchases up to the poverty level. The impact of the FairTax on the distribution of the tax burden is a point of dispute. The plan's supporters argue that it would decrease tax burdens, broaden the tax base, be progressive, increase purchasing power, and tax wealth, while opponents argue that a national sales tax would be inherently regressive and would decrease tax burdens paid by high-income individuals.

Goods and Services Tax (GST) in Singapore is a value added tax (VAT) of 9% levied on import of goods, as well as most supplies of goods and services. Exemptions are given for the sales and leases of residential properties, importation and local supply of investment precious metals and most financial services. Export of goods and international services are zero-rated. GST is also absorbed by the government for public healthcare services, such as at public hospitals and polyclinics.

Tax deferral refers to instances where a taxpayer can delay paying taxes to some future period. In theory, the net taxes paid should be the same. Taxes can sometimes be deferred indefinitely, or may be taxed at a lower rate in the future, particularly for deferral of income taxes.

Optimal tax theory or the theory of optimal taxation is the study of designing and implementing a tax that maximises a social welfare function subject to economic constraints. The social welfare function used is typically a function of individuals' utilities, most commonly some form of utilitarian function, so the tax system is chosen to maximise the aggregate of individual utilities. Tax revenue is required to fund the provision of public goods and other government services, as well as for redistribution from rich to poor individuals. However, most taxes distort individual behavior, because the activity that is taxed becomes relatively less desirable; for instance, taxes on labour income reduce the incentive to work. The optimization problem involves minimizing the distortions caused by taxation, while achieving desired levels of redistribution and revenue. Some taxes are thought to be less distorting, such as lump-sum taxes and Pigouvian taxes, where the market consumption of a good is inefficient, and a tax brings consumption closer to the efficient level.

The Robin Hood effect is an economic occurrence where income is redistributed so that economic inequality is reduced. That is a redistribution of economic resources due to which the economically disadvantaged gain at the expense of the economically advantaged. The effect is named after English folkloric figure Robin Hood, said to have stolen from the rich to give to the poor.

The Suits index of a public policy is a measure of tax progressiveness, named for economist Daniel B. Suits. Similar to the Gini coefficient, the Suits index is calculated by comparing the area under the Lorenz curve to the area under a proportional line. For a progressive tax, the Suits index is positive. A proportional tax has a Suits index of zero, and a regressive tax has a negative Suits index. A theoretical tax where the richest person pays all the tax has a Suits index of 1, and a tax where the poorest person pays everything has a Suits index of −1. Tax preferences also have a Suits index.

Economic theory evaluates how taxes are able to provide the government with required amount of the financial resources and what are the impacts of this tax system on overall economic efficiency. If tax efficiency needs to be assessed, tax cost must be taken into account, including administrative costs and excessive tax burden also known as the dead weight loss of taxation (DWL). Direct administrative costs include state administration costs for the organisation of the tax system, for the evidence of taxpayers, tax collection and control. Indirect administrative costs can include time spent filling out tax returns or money spent on paying tax advisors.

Taxes in Germany are levied at various government levels: the federal government, the 16 states (Länder), and numerous municipalities (Städte/Gemeinden). The structured tax system has evolved significantly, since the reunification of Germany in 1990 and the integration within the European Union, which has influenced tax policies. Today, income tax and Value-Added Tax (VAT) are the primary sources of tax revenue. These taxes reflect Germany's commitment to a balanced approach between direct and indirect taxation, essential for funding extensive social welfare programs and public infrastructure. The modern German tax system accentuate on fairness and efficiency, adapting to global economic trends and domestic fiscal needs.

In general, the United States federal income tax is progressive, as rates of tax generally increase as taxable income increases, at least with respect to individuals that earn wage income. As a group, the lowest earning workers, especially those with dependents, pay no income taxes and may actually receive a small subsidy from the federal government.

Taxation in Brazil is complex, with over sixty forms of tax. Historically, tax rates were low and tax evasion and avoidance were widespread. The 1988 Constitution called for an enhanced role of the State in society, requiring increased tax revenue. In 1960, and again between 1998 and 2004, efforts were made to make the collection system more efficient. Tax revenue gradually increased from 13.8% of GDP in 1947 to 37.4% in 2005. Tax revenue has become quite high by international standards, but without realising commensurate social benefit. More than half the total tax is in the regressive form of taxes on consumption.