A value-added tax (VAT or goods and services tax (GST), general consumption tax (GCT)), is a consumption tax that is levied on the value added at each stage of a product's production and distribution. VAT is similar to, and is often compared with, a sales tax. VAT is an indirect tax because the consumer who ultimately bears the burden of the tax is not the entity that pays it. Specific goods and services are typically exempted in various jurisdictions.

Products exported to other countries are typically exempted from the tax, typically via a rebate to the exporter. VAT is usually implemented as a destination-based tax, where the tax rate is based on the location of the producer. VAT raises about a fifth of total tax revenues worldwide and among the members of the Organisation for Economic Co-operation and Development (OECD).[1]:14 As of June 2023, 175[2] of the 193 countries with UN membership employ a VAT, including all OECD members except the United States.[1]:14

History

Germany and France were the first countries to implement a VAT, enacting a general consumption tax during World War I.[3] German industrialist Wilhelm von Siemens proposed the concept in 1918. The modern variation of VAT was first implemented by France in 1954 in its Ivory Coast (Côte d'Ivoire) colony. Assessing the experiment as successful, France introduced it domestically in 1958.[3]Maurice Lauré, Joint Director of the France Tax Authority (Direction Générale des Impôts) implemented VAT on 10 April 1954, Initially directed at large businesses, it was extended over time to include all business sectors. In France it is the largest source of state finance, accounting for nearly 50% of state revenues.[4]

A Belgian VAT receipt

Implementation

VAT can be accounts-based or invoice-based.[5] All countries except Japan use the invoice method.[6][7][8]

Using invoices, each seller pays VAT on their sales and passes the buyer an invoice that indicates the amount of tax paid excluding deductions (input tax). Buyers who themselves add value and resell the product pay VAT on their own sales (output tax). The difference between output tax and input tax is the amount paid to the government (or refunded, in the case of a negative amount).

Using accounts, the tax is calculated as a percentage of the difference between sales and purchases from taxed accounts.[6][7][8]

Incentives

VAT provides an incentive for businesses to register and keep invoices, and it does this in the form of zero rated goods and VAT exemption on goods not resold.[9] Through registration, a business documents its purchases, making them eligible for a VAT credit.

The main benefit of VAT is that in relation to many other forms of taxation, "it does not distort firms' production decisions, it is difficult to evade, and it generates a substantial amount of revenue."[10]

Many countries offer VAT refunds to international travelers on purchased goods that they take out of the country. While VAT refunds are commonly utilized by tourists, the process for business travelers to reclaim VAT can be more complex. As a result, eligible refunds for business travelers are often left unclaimed.

Some countries, particularly in Western Europe, offer VAT refunds on business-related expenses to encourage the hosting of business meetings, events, and conferences within their borders. These refunds often extend to costs incurred during trade fairs and exhibitions. In certain countries, VAT paid on meals and fuel may also be eligible for a refund.

Imports

For VAT purposes, an importer is assumed to have contributed 100% of the value of a product imported from outside of the taxing jurisdiction. The importer thus pays VAT on the entire sales price of the import, and has no invoices to use to reduce the amount, even if the foreign manufacturer paid taxes. This is in contrast to the US income tax system, which allows businesses to expense costs paid to foreign manufacturers. For this reason, VAT is often considered by US manufacturers to be a trade barrier, as further discussed below.

In general, countries that have a VAT system require most businesses to register for VAT purposes. VAT-registered businesses can be natural persons or legal entities. Regulations specifying which businesses must register vary by country. VAT-registered businesses are required to add VAT to their sales.

Comparison with income tax

Unlike VAT, income taxes are based on some definition of income, which comes with many complexities reflecting considerations of things such as income source, income level, and household status. Notable differences:[11]

VAT is paid by businesses, while income tax is paid both by businesses and individuals.

VAT rates are uniform across all taxed products, making it a flat tax.

Comparison with sales tax

VAT has no effect on how businesses organize, because the same amount of tax is collected regardless of how many times goods change hands before arriving at the ultimate consumer. By contrast, sales taxes are collected on each transaction, encouraging businesses to vertically integrate to reduce the number of transactions and thereby reduce the amount of tax. For this reason, VAT has been gaining favor over traditional sales taxes.

Another difference is that VAT is collected at the national level, while in countries such as India and the US, sales tax is collected at the point of sale by the local jurisdiction, leading them to prefer the latter method.

The main disadvantage of VAT is the extra accounting required by those in the supply chain. When the VAT system has few, if any, exemptions such as with GST in New Zealand, payment of VAT is even simpler.[12]

A general economic idea is that if tax rates are high enough, people scheme to evade them. However, VAT rates have risen above 10% without widespread evasion because of the collection mechanism. However VAT is subject to frauds like missing trader fraud, which can significantly reduce tax payments.

Examples

Untaxed

Without any tax

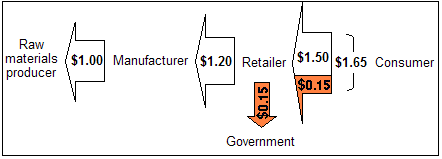

A widget manufacturer, for example, spends $1.00 on raw materials and uses them to make a widget.

The widget is sold wholesale to a widget retailer for $1.20, at a gross margin of $0.20.

The widget retailer then sells the widget to a widget consumer for $1.50, at a gross margin of $0.30.

Sales tax

10% sales tax:

With a 10% sales tax

The manufacturer spends $1.00 for the raw materials, certifying it is not a final consumer.

The manufacturer charges the retailer $1.20, checking that the retailer is not a consumer, leaving the same gross margin of $0.20.

The retailer charges the consumer ($1.50 × 1.10) = $1.65 and pays the government $0.15, leaving the gross margin of $0.30.

So the consumer pays 10% ($0.15) extra, compared to the no taxation scheme, and the government collects this amount. The retailers pay no tax directly, but the retailer has to do the tax-related paperwork. Suppliers and manufacturers have the administrative burden of supplying correct state exemption certifications that the retailer must verify and maintain.

The manufacturer is responsible for ensuring that their customers (retailers) are only intermediates and not end consumers (otherwise the manufacturer charges the tax). In addition, the retailer tracks what is taxable and what is not, along with the various tax rates in each city where it operates.

Value-added tax

10% VAT:

With a 10% VAT

The manufacturer spends ($1 × 1.10) = $1.10 to buy raw materials, and the seller of the raw materials pays the government $0.10.

The manufacturer charges the retailer ($1.20 × 1.10) = $1.32 and pays the government ($0.12 minus $0.10) = $0.02, leaving the same gross margin of ($1.32 – $1.10 – $0.02) = $0.20.

The retailer charges the consumer ($1.50 × 1.10) = $1.65 and pays the government ($0.15 minus $0.12) = $0.03, leaving the same gross margin of ($1.65 – $1.32 – $0.03) = $0.30.

Manufacturer and retailer gross margins are a smaller percent of the total perspective. If the cost of raw material production were shown, this would also be true of the raw material supplier's gross margin on a percentage basis.

Note that the taxes paid by both the manufacturer and the retailer to the government are 10% of the values added by their respective business practices (e.g. the value added by the manufacturer is $1.20 minus $1.00, thus the tax payable by the manufacturer is ($1.20 – $1.00) × 10% = $0.02).

In the VAT example above, the consumer has paid, and the government received, the same dollar amount as with a sales tax. At each stage of production, the seller collects a tax and the buyer pays that tax. The buyer can then be reimbursed for paying the tax, but only by successfully selling the value-added product to the buyer at the next stage. In the previous examples, if the retailer fails to sell some of its inventory, it suffers a greater financial loss in the VAT scheme, in comparison to the sales tax regulatory system, by having paid a higher wholesale price on the product it wants to sell.

Each business is responsible for handling the necessary tax paperwork. However, businesses have no obligation to request certifications from purchasers who are not end users, or of providing such certifications to their suppliers, but they incur increased accounting costs for collecting the tax.

Limitations

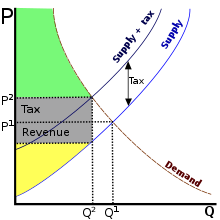

The simplified examples assume incorrectly that taxes are non-distortionary: the same number of widgets were made and sold both before and after the introduction of the tax. However, the supply and demandeconomic model suggests that any tax raises the cost of the product for someone. In raising the cost, the supply curve shifts leftward. Consequently, the quantity of a good purchased decreases, and/or the price at which it is sold increases.

VAT, like most taxes, distorts economic behavior. Because the price rises, the quantity of goods traded typically decreases.[citation needed] This reduces consumer welfare, worker and business incomes, and corresponding income tax revenues. This is known as a deadweight loss, because the VAT produces no revenue from transactions that do not take place. If these losses are greater than the VAT on transactions that do take place, the tax is inefficient.

Of course, the tax on transactions that do take place, if used effectively, can potentially offset the deadweight loss. Despite these losses, consumption taxes such as VAT may induce smaller distortions to incentives to invest, save and work vs other types of taxation–in that VAT discourages consumption rather than production.

In the diagram:

Deadweight loss: the area of the triangle formed by the right side of the tax income box, the original supply curve, and the demand curve

Government's tax income: the grey rectangle captioned “Tax Revenue”

As a consumption tax, VAT usually replaces sales tax. Ultimately, it taxes the same people and businesses the same amounts of money, despite its different internal mechanism. VAT and sales tax significantly differ for imports and exports:

VAT is charged for exports while sales tax is not.

Sales tax is paid for the full price of imports, while VAT is charged only for value added by the importer and the reseller.

Without an adjustment, exports would be taxed twice if exported from a VAT country to a sales tax country. Conversely, imports from a sales tax country into a VAT country pay no sales tax and VAT on only a fraction of the value. Countries differ in taxation for imports/exports. Sales tax is charged in the same way for both imported and domestic goods, and is never charged twice.

To address this problem, nearly all VAT countries adjust their rules for imported and exported goods:

All imports are charged VAT for their full price when they are sold for the first time.

In Germany a product is sold to a German reseller for $2,500+VAT ($3,000). The German reseller gets a VAT rebate (the refund time change in base of local laws and states) and will then charge the VAT to the customer.

In the US a product is sold to another US reseller for $2,500 (without the sales tax) with a certificate of exemption. The US reseller will charge the sales tax to the customer.

Note: The European VAT system affects company cashflow due to compliance costs[13] and fraud risk for governments due to overclaimed taxes.[citation needed]

B2B sales between countries have different rules, such that the reverse charge (VAT) or sales tax exemption are applied; in the case of B2C sales the seller pays the VAT or sales tax to the receiving jurisdiction (creating the controversial situation of a foreign company paying taxes of their taxable residents/citizens without jurisdiction on seller).

Criticisms

4 May 2010 "Campaña no más IVA" in Spain

VAT has been criticized as its burden falls on consumers. It is a regressive tax, meaning that the poor pay more, as a percentage of their income, than the rich, given their higher marginal propensity to consume.[14] Defenders reply that relating taxation levels to income is an arbitrary standard and that the VAT is in fact a proportional tax. An OECD study found that VAT could be slightly progressive.[15][16] VAT's effective regressivity can be reduced by applying a lower rate to products that are more likely to be consumed by the poor.[14] Some countries compensate by implementing a progressive income tax or by transfer payments targeted to the poor.[17]

VAT revenues are frequently lower than expected because they are difficult and costly to administer and collect.[citation needed] However, collection of other taxes may face similar or worse challenges. VAT has become more important in many jurisdictions as tariff levels have fallen worldwide due to trade liberalization, as VAT has effectively replaced reduced tariff revenues. Whether the costs and distortions of are lower than the economic inefficiencies and enforcement issues (e.g. smuggling) from high import tariffs is debated, but theory suggests VATs are far more efficient.[citation needed]

Certain industries (small-scale services, for example) tend to have more VAT avoidance, particularly where cash transactions predominate, and VAT may be criticized for encouraging this.[citation needed] From the perspective of government, however, VAT may be acceptable because it captures at least some transactions. Another criticism is that consumer costs increase.

Deadweight loss

The incidence of VAT may not fall entirely on consumers as traders tend to absorb VAT so as to maintain sales volumes. Conversely, not all cuts in VAT are passed on in lower prices. VAT consequently leads to a deadweight loss if cutting prices pushes a business below the margin of profitability. The effect can be seen when VAT is cut or abolished. Sweden reduced VAT on restaurant meals from 25% to 12.5%, creating 11,000 additional jobs.[18]

Fraud

VAT offers distinctive opportunities for evasion and fraud, especially through abuse of the credit and refund mechanism.[19] VAT overclaim fraud reached as high as 34% in Romania.[20]

Exports are generally zero-rated, creating opportunity for fraud. In Europe, the main source of problems is carousel fraud.[citation needed] This fraud originated in the 1970s in the Benelux countries. VAT fraud then became a major problem in the UK.[21] Similar fraud possibilities exist inside a country. To avoid this, countries such as Sweden hold the major owner of a limited company personally responsible.[22]

Churning

Because VAT is included in the price index to which state benefits such as pensions and welfare payments are linked in some countries, as well as public sector pay, some of the apparent revenue is churned – i.e. taxpayers are given the money to pay the tax, reducing net revenue.[23]

Business cashflow

Refund delays by the tax administration can damage businesses.[13]

Compliance costs

Compliance costs are seen as a burden on business.[24] In the UK, compliance costs for VAT have been estimated to be about 4% of the yield, with greater impacts on smaller businesses.[25]

Trade criticism

National VAT act as a tariff on imports and their exports are exempt from VAT (zero-rated).

Under a sales tax system, only businesses selling to the end-user are required to collect tax and bear the accounting cost of collecting the tax. Under VAT, manufacturers and wholesale companies also incur accounting expenses to handle the additional paperwork required for collecting VAT, increasing overhead costs and prices.

The American Manufacturing Trade Action Coalition in the United States consider VAT charges on US products and rebates for products from other countries to be an unfair trade practice. AMTAC claims that so-called "border tax disadvantage" is the greatest contributing factor to the US current account deficit, and estimated this disadvantage to US producers and service providers to be $518 billion in 2008 alone. US politicians such as congressman Bill Pascrell, advocate either changing WTO rules relating to VAT or rebating VAT charged on US exporters.[26] A business tax rebate for exports was proposed in the 2016 GOP tax reform policy paper.[27][28] The assertion that this "border adjustment" would be compatible with the rules of the WTO is controversial; it was alleged that the proposed tax would favour domestically produced goods as they would be taxed less than imports, to a degree varying across sectors. For example, the wage component of the cost of domestically produced goods would not be taxed.[29]

A 2021 study reported that value- added taxes were unlikely to distort trade flows.[30]

The VAT rate is 20%. However, the expanded application is zero VAT for many operations and transactions. That zero VAT is the source of controversies between its trading partners, mainly Russia, which is against the zero VAT and promotes wider use of tax credits. VAT is replaced with fixed payments, which are utilized for many taxpayers, operations, and transactions. Legislation is based largely on the EU VAT Directive's principles.[31]

The system is input-output based. Producers are allowed to subtract VAT on their inputs from the VAT they charge on their outputs and report the difference.[31] VAT is purchased quarterly. An exception occurs for taxpayers who state monthly payments. VAT is disbursed to the state's budget on the 20th day of the month after the tax period.[32] The law took effect on January 1, 2022.[33]

The goods and services tax (GST) is a VAT introduced in Australia in 2000. Revenue is redistributed to the states and territories via the Commonwealth Grants Commission process. This works as a program of horizontal fiscal equalisation. The rate is set at 10%, although many domestically consumed items are effectively zero-rated (GST-free) such as fresh food, education, health services, certain medical products, as well as government charges and fees that are effectively taxes.

VAT was introduced in 1991, replacing sales tax and most excise duties. The Value Added Tax Act, 1991 triggered VAT starting on 10 July 1991, which is observed as National VAT Day.[34][35][36][37] VAT became the largest source of government revenue, totaling about 56%. The standard rate is 15%. Export is zero rated. Several reduced rates, locally called Truncated Rates, apply to service sectors and range from 1.5% to 10%. The Value Added Tax and Supplementary Duty Act of 2012 automated administration.[38][35]

The National Board of Revenue (NBR) administers VAT. Other rules and acts include Development Surcharge and Levy (Imposition and Collection) Act, 2015;[39] and Value Added Tax and Supplementary Duty Rules, 2016.[40] Anyone who collects VAT becomes a VAT Trustee if they: register and collect a Business Identification Number (BIN) from the NBR; submit VAT returns on time; offer VAT receipts; store all cash-memos; and use the VAT rebate system responsibly. VAT Mentors work in the VAT or Customs department and deal with trustees. The VAT rate is a flat 15%.

VAT was introduced on 1 January 1997 and replaced 11 other taxes.[41] The original rate of 15% was increased to 17.5% in 2011.[42] The rate on restaurant and hotel accommodations is between 10% and 15% while certain foods and goods are zero-rated.[43] The revenue is collected by the Barbados Revenue Authority.[44]

VAT was 20% as of 2023. A reduced rate of 9% applies to baby foods and hygiene products, as well as on books. A permanent rate of 9% applies to physical or electronic periodicals, such as newspapers and magazines.

Advertised and posted prices generally exclude taxes, which are calculated at the time of payment; common exceptions are motor fuels, the posted prices for which include sales and excise taxes, and items in vending machines as well as alcohol in monopoly stores. Basic groceries, prescription drugs, inward/outbound transportation and medical devices are zero-rated. Other provinces that do not have a HST may have a Provincial Sales Tax (PST), which are collected in British Columbia (7%), Manitoba (7%) and Saskatchewan (6%). Alberta and all three territories do not collect either a HST or PST.

Chile

VAT was introduced in Chile in 1974 under Decreto Ley 825.[45] From 1998 there was implemented a 18% tax.[46] Since 2003, the standard rate of VAT is 19%. Since October 2003, the standard VAT rate has been 19%, applying to the majority of goods and some services. However certain items have been subjected to additional tax, for instance, alcoholic beverages (between 20.5= – 31.5% for fermented to distilled products), jewellery (15%), pyrotechnic items (50% or more for the first sale or import) or soft drinks with high sugar (18%). AS of 2023, the VAT tax includes majority of services excluding Education, Health and Transport, as well as taxpayers issuing fee receipts.[47] This tax makes the 41.2% of the total revenue of the country.[48]

VAT was implemented in 1984 and is administered by the State Administration of Taxation. In 2007, VAT revenue was 15.47 billion yuan ($2.2 billion), 33.9 percent of China's total tax revenue. [dubious–discuss] The standard rate is 13%. A reduced rate of 9% applies to products such as books and types of oils, and 6% for services except for PPE leases.[49]

Czech Republic

In 1993, a standard rate of 23% and a reduced rate of 5% for non-alcoholic beverages, sewerage, heat, and public transport was introduced. In 2015, rates were revised to 21% for the standard rate, and 15% and 10% reduced rates. The lowest reduced rate primarily targeted baby food, medicines, vaccines, books, and music shops, while maintaining a similar redistribution of goods and services for the other rates.

In 2024, a law aimed at reducing the national debt featured return to two rates: a standard rate of 21% and a reduced rate of 12%. Goods and services were redistributed among different tax rates.

There was only one services that shifted from the standard rate to the reduced rate and that were non-regular land passenger bus services. These are not taxi services, which apply a VAT rate of 21%. Books and printed materials, including electronic books, were zero rated.

Several services were moved from reduced rates to the standard rate. Examples include hairdressers and barbers, bicycle repairs, footwear and clothing repairs, freelance journalists and models, cleaning services, and municipal waste.[50][51][52]

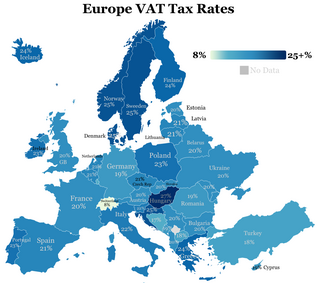

Each state must comply with EU VAT law,[53] which requires a minimum standard rate of 15% and one or two reduced rates not to be below 5%. Some EU members have a 0% VAT rate on certain items; these states agreed this as part of their accession (for example, newspapers and certain magazines in Belgium). Certain goods and services must be exempt from VAT (for example, postal services, medical care, lending, insurance, betting), and certain other items are exempt from VAT by default, but states may opt to charge VAT on them (such as land and certain financial services). Hungary charges the highest rate, 27%. Only Denmark has no reduced rate.[54]

Some areas of states (both overseas and on the European continent) that are outside the EU VAT area, and some non-EU states operate inside the EU VAT area. External areas may have no VAT or may have a rate lower than 15%. Goods and services supplied from external areas to internal areas are classified as imported.

VAT charged by a business is known as "output VAT". VAT paid by a business is known as "input VAT". A business is generally able to recover input VAT to the extent that the input VAT is used to make its taxable outputs. Input VAT is recovered by offsetting it against the output VAT, or, if there is an excess, by claiming a rebate.

People are generally allowed to buy goods in any member country, bring it home, and pay only VAT to the seller. Input VAT paid on VAT-exempt supplies[example needed] is not recoverable, although a business can increase prices so the customer effectively bears the cost of the "sticking" VAT (the effective rate is lower than the headline rate and depends on the balance between previously taxed input and labour at the exempt stage).

The United Arab Emirates (UAE) on 1 January 2018 implemented VAT. For companies whose annual revenues exceed $102,000 (Dhs 375,000), registration is mandatory. GCC countries agreed to an introductory rate of 5%.[55][56][57]Saudi Arabia's VAT system uses a 15% rate.[58]

Per 1 April 2022, maximum a Goods and Services Tax (GST) is levied at the rate of 11% at point of sales. Sales and services tax are exempt from cottage economies and industries.

A VAT rate of 0 (zero) percent is applied to the following taxable events:

export for taxable goods

export for intangible taxable goods

export for taxable services

VAT base on equivalent to the sale price/service fee or import/export value.

Supermarket receipt showing three categories of IVA

Value added tax or VAT, (in Italian Imposta sul valore aggiunto, or IVA) is a consumption tax charged at a standard rate of 22 percent, which came in on 1 July 2013 (previously 21 percent).

The first reduced VAT rate (10 percent) applies to water supplies, passenger transport, admission to cultural and sports events, hotels, restaurants and some foodstuff. The second reduced VAT rate (5 percent) applies to some foodstuff and social services. The super-reduced VAT rate (4 percent) applies to TV licenses, newspapers, periodicals, books and medical equipment for the disabled. A zero VAT rate (0 percent) applies to intra-community and international transport.

The filing deadline for VAT returns is 30 April of the next year.[59]

Value-added tax (VAT) in Israel, is applied to most goods and services, including imported goods and services. From 1 October 2015 the standard rate was decreased to 17%, from 18%.[60][61] It had been raised from 16% to 17% on 1 September 2012,[62] and to 18% on 2 June 2013.[63]

Certain items, such as exported goods and the provision of certain services to non-residents are zero-rated. VAT on imported goods is levied on value plus customs duty, purchase tax and other levies.[64][65]

Multinational companies that provide services to Israel through the Internet, such as Google and Facebook, must pay VAT.[66]

VAT was implemented in Japan in 1989.[68] Tax authorities debated VAT in the 1960s and 1970s, but decided against it at the time.[68]

The standard rate is 10%. Food, beverages, newspaper subscriptions with certain criteria and other necessities qualify for a rate of 8%. Transactions including land sales or lease, securities sales and the provision of public services are exempt.[69]

The Goods and Services Tax (GST) is an abolished value-added tax in Malaysia. GST is levied on most transactions in the production process, but is refunded with exception of Blocked Input Tax, to all parties in the chain of production other than the final consumer.

The existing standard rate for GST effective from 1 April 2015 is 6%. Many domestically consumed items such as fresh foods, water and electricity are zero-rated, while some supplies such as education and health services are GST exempted.

After Pakatan Harapan won the 2018 Malaysian general election, GST was reduced to 0% on 1 June 2018.[70] The then Government of Malaysia tabled the first reading of the Bill to repeal GST in Parliament on 31 July 2018 (Dewan Rakyat).[71] GST was replaced with the Sales Tax and Service Tax starting 1 September 2018.

Mexico

The existing sales tax (Spanish: impuesto a las ventas) was replaced by VAT (Spanish: Impuesto al Valor Agregado, IVA) on 1 January 1980. As of 2010, the general VAT rate was 16%. This rate was applied all over Mexico except for border regions (i.e. the United States border, or Belize and Guatemala), where the rate was 11%. Books, food, and medicines are zero-rated. Some services such as medical care are zero-rated. In 2014 the favorable tax rate for border regions was eliminated and the rate increased to 16% across the country.

Value Added Tax (VAT) is an indirect tax levied on the value creation or addition. The concept of VAT in Nepal was introduced in FY 2049/50 but the act was developed in BS 2050. VAT was implemented in 1998 and is the major source of government revenue. It is administered by the Inland Revenue Department of Nepal.

GST in New Zealand is designed to be a broad-based system with few exemptions, such as for rents collected on residential rental properties, donations, precious metals and financial services.[72] Because it is broad-based, it collects 31.4% of total taxation, GDP.[73]

The rate for GST, effective since 1 October 2010 as implemented by the National Party, is 15%.[74] This 15% tax is applied to the final price of the product or service being purchased and goods and services are advertised as GST inclusive. Reduced rate GST (9%) applies to hotel accommodation on a long-term basis (longer than 4 weeks). Zero rate GST (0%) applies to exports and related services; financial services; land transactions; international transportation.

Financial services, real estate, precious metals are also exempt (0%).

MOMS (Danish: merværdiafgift, formerly meromsætningsafgift), Norwegian: merverdiavgift (bokmål) or meirverdiavgift (nynorsk) (abbreviated MVA), Swedish: Mervärdes- och OMSättningsskatt (until the early 1970s labeled as OMS OMSättningsskatt only), Icelandic: virðisaukaskattur (abbreviated VSK), Faroese: meirvirðisgjald (abbreviated MVG) or Finnish: arvonlisävero (abbreviated ALV) are the Nordic terms for VAT. Like other countries' sales and VAT, it is an indirect tax.

Year

Tax level (Denmark)

Name

1962

9%

OMS

1967

10%

MOMS

1968

12.5658%

MOMS

1970

15%

MOMS

1977

18%

MOMS

1978

20.25%

MOMS

1980

22%

MOMS

1992

25%

MOMS

Denmark has the highest VAT, alongside Norway, Sweden, and Croatia. VAT is generally applied at one rate, 25%, with few exceptions. Services such as public transport, health care, newspapers, rent (the lessor can voluntarily register as a VAT payer, except for residential premises), and travel agencies.

In Finland, the standard rate is 24%.[75] A 14% rate is applied on food and animal feed, and a 10% rate is applied on public transport, cinema, exercise services, books, pharmaceuticals, and tickets to cultural and entertainment events. Zero rated services include medical care; social welfare services; education, financial and insurance services; lotteries and money games; cash transactions; real property including building land; certain transactions by blind persons and interpretation services for deaf persons. Åland, an autonomous area, is considered to be outside the EU VAT area, although its VAT rate is the same as for Finland. Goods brought from Åland to Finland or other EU countries are considered to be imports. This enables tax-free sales onboard passenger ships.

In Iceland, VAT is 24% for most goods and services. An 11% rate is applied for hotel and guesthouse stays, licence fees for radio stations (namely RÚV), newspapers and magazines, books; hot water, electricity and oil for heating houses, food for human consumption (but not alcoholic beverages), access to toll roads and music.[76]

In Norway, the general rate is 25%, 15% on foodstuffs, and 12% on hotels and holiday homes, on some transport services, cinemas.[77] Financial services, health services, social services and educational services,[78] newspapers, books and periodicals are zero-rated.[79]Svalbard has no VAT because of a clause in the Svalbard Treaty.

In Sweden, VAT is 25% for most goods and services, 12% for foods including restaurants, and hotels. It is 6% for printed matter, cultural services, and transport of private persons. Zero-rated services including public (but not private) education, health, dental care. Dance event tickets are 25%, concerts and stage shows are 6%, while some types of cultural events are 0%.

MOMS replaced OMS (Danish omsætningsafgift, Swedish omsättningsskatt) in 1967, which was a tax applied exclusively for retailers.

Philippines

The VAT rate is 12%. Senior citizens are exempted from paying VAT for most goods and some services for personal consumption.

Poland

VAT was introduced in 1993. The standard rate is 23%. Items and services eligible for an 8% include certain food products, newspapers, goods and services related to agriculture, medicine, sport, and culture. The complete list is in Annex 3 to the VAT Act. A 5% applies to basic food items (such as meat, fruits, vegetables, dairy and bakery products), children's items, hygiene products, and books. Exported goods, international transport services, supply of specific computer hardware to educational institutions, vessels, and air transport are zero rated. Taxi services have flat-rate tax of 4%. Flat-rate farmers supplying agricultural goods to VAT taxable entities are eligible for a 7% refund.[80]

The VAT rate is 20% with exemptions for some services (for example, medical care). VAT payers include organizations (industrial and financial, state and municipal enterprises, institutions, business partnerships, insurance companies and banks), enterprises with foreign investments, individual entrepreneurs, international associations, and foreign entities with operations in the Russian Federation, non-commercial organizations that conduct commercial activities, and those who move goods across the border of the Customs Union.[81][82][83]

Goods and Services Tax (GST) in Singapore is a value added tax (VAT) of 9% levied on import of goods, as well as most supplies of goods and services. Exemptions are given for the sales and leases of residential properties, importation and local supply of investment precious metals and most financial services.[84] Export of goods and international services are zero-rated. GST is also absorbed by the government for public healthcare services, such as at public hospitals and polyclinics.

Slovakia

The standard rate is 20%. A 10% rate primarily applies to essential goods such as (healthy) food, medicine, and books. A 5% rate covers building renovation.[85]

VAT (IVA in Spanish: impuesto sobre el valor añadido or impuesto sobre el valor agregado) is due on any supply of goods or services sold in Spain. The current normal rate is 21% which applies to all goods which do not qualify for a reduced rate or are exempt. There are two lower rates of 10% and 4%. The 10% rate is payable on most drinks, hotel services, and cultural events. The 4% rate is payable on food, books and medicines.[86] An EU directive means that all countries of the European Union have VAT. All exempt goods and services are listed below.

Education provided by the state

Tutoring

Sporting services

Cultural services

Insurance

Postal stamps

Artists, writers, and composers

As of January 1, 2013, new properties are taxed at a reduced rate of 10%. Second-hand properties are not subject to VAT, but a transfer tax, known as Impuestos Sobre Transmisiones Patrimoniales or ITP. The tax is levied by the autonomous regional governments and therefore varies by region. The rate varies from 6% to 8%.[86]

The value added tax (VAT; Mehrwertsteuer / Taxe sur la valeur ajoutée / Imposta sul valore aggiunto) is one of the Confederation's principal sources of funding. It is levied at a rate of 8.1 percent on most commercial exchanges of goods and services. Certain exchanges are subject to a reduced VAT of 2.6 percent:

Foodstuffs (except alcoholic beverages)

Cattle, poultry, fish

Seeds, living plants, cut flowers

Grains

Animal feed and fertilizer

Medications

Newspapers, magazines, books and other printed products without advertising character of the kinds to be stipulated by the Federal Council

Services of radio and television companies (exception: the normal rate applies for services of a commercial nature)

A special rate of 3.8% is in use in the hotel industry.[87] Yet other exchanges, including those of medical, educational and cultural services, are tax-exempt; as are goods delivered and services provided abroad.[88] The party providing the service or delivering the goods is liable for the payment of the VAT, but the tax is usually passed on to the customer as part of the price.[89]

In 2014 total revenue from VAT was nearly CHF 11 billion (short scale) on CHF 866 billion of taxable sales. In 2013 the revenue and sales were CHF 10.3 billion and 858 billion respectively.[90]

VAT in Taiwan is 5%. It is levied on all goods and services. Exceptions include exports, vessels, aircraft used in international transportation, and deep-sea fishing boats.[91]

Value added tax is levied on the supply of goods and service in Ukraine and on the import and export of goods and auxiliary services. Supplies to and from Crimea are treated as exports and imports for value added tax purposes. The standard VAT rate is 20% for domestic supplies and imported goods (including auxiliary services). A 7% rate applies to supplies of pharmaceuticals and healthcare products. Exported goods and auxiliary services are zero-rated. For VAT purposes, services that are included in the customs value of imported and exported goods are considered auxiliary services Certain supplies are not subject to VAT, including: issues of securities; insurance services; reorganization of legal entities; transfers and returns of property under operating lease arrangements; currency exchange; and imports and exports with a custom value of less than 150 EUR. VAT-exempt supplies include published periodicals; student notebooks, textbooks, books and certain educational services; certain public transport services; the provision of software products (until January 1. 2023); and the provision of healthcare services by licensed institutions. Registration is required (for residents and non-residents) if value of taxable supplies of goods or services exceeds ₴1 million during any 12-month period. A legal entity may apply for voluntary registration if it has no VATable activities or if the volume

of its VATable transactions is less than the registration threshold. Although not specifically provided for in the Tax Code, in practice a nonresident entity must register for Ukrainian VAT purposes via representative office and/or PE in Ukraine.

Puerto Rico replaced its 6% sales tax with a 10.5% VAT beginning 1 April 2016, leaving in place its 1% municipal sales and use tax. Materials imported for manufacturing are exempt.[95][96][97] However, two states enacted a form of VAT in lieu of a business income tax.

Michigan used a form of VAT known as the "Single Business Tax" (SBT) from 1975 until voter-initiated legislation repealed it, replaced by the Michigan Business Tax in 2008.[98]

Hawaii has a 4% General Excise Tax (GET) that is charged on gross business income. Individual counties add a .5% surcharge. Unlike a VAT, rebates are not available, such that items incur the tax each time they are (re)sold.[99]

Discussions about a federal VAT

This section needs expansion. You can help by adding to it. (February 2016)

Richard Nixon reportedly considered a federal VAT.[citation needed] Former 2020 Democratic presidential candidate Andrew Yang advocated for a national VAT in order to pay for his universal basic income proposal. A national subtraction-method VAT, often referred to as a "flat tax", has been repeatedly proposed as a replacement of the corporate income tax.[6][7][8]

All organizations and individuals producing and trading VAT taxable goods and services pay VAT, regardless of whether they have Vietnam-resident establishments.

Vietnam has three VAT rates: 0 percent, 5 percent and 10 percent. 10 percent is the standard rate.

A variety of goods and service transactions qualify for VAT exemption.[102]

Tax rates

Standard VAT or sales tax rateGeneral government revenue, in% of GDP, from VAT. For this data, the variance of GDP per capita with purchasing power parity (PPP) is explained in 3% by tax revenue.

10% for rental for the purpose of habitation, food, garbage collection, most transportation, etc. 13% for plants, live animals and animal food, art, wine (if bought directly from the winemaker), etc.[104]

18% (milk and dairy products, cereal products, hotels, tickets to outdoor music events) or 5% (pharmaceutical products, medical equipment, books and periodicals, some meat products, district heating, heating based on renewable sources, live music performance under certain circumstances) or 0% (postal services, medical services, mother's milk, etc.)[112]

10% (hotels, bars, restaurants and other tourism products, certain foodstuffs, plant protection products and special works of building restoration, home-use utilities: electricity, gas used for cooking and water) or 4% (e.g. grocery staples, daily or periodical press and books, works for the elimination of architectural barriers, some kinds of seeds, fertilizers)

14% on certain wines, 8% on public utilities, or 3% on books and press, food (including restaurant meals), children's clothing, hotel stays, and public transit[114]

TVA MwSt./USt MS

Taxe sur la Valeur Ajoutée Mehrwertsteuer/Umsatzsteuer Méiwäert Steier

13% for processed food, provision of services, and others such as oil and diesel, climate action focused goods and musical instruments and 6% for food products, agricultural services, and other deemed essential products such as farmaceutical products and public transport[118] 12% or 5% in Madeira and 9% or 4% in Azores[116][117]

12% (e.g. food, hotels and restaurants), 6% (e.g. books, passenger transport, cultural events and activities), 0% (e.g. insurance, financial services, health care, dental care, prescription drugs, immovable property)[123][124]

0% fresh food, medical services, medicines and medical devices, education services, childcare, water and sewerage, government taxes & permits and many government charges, precious metals, second-hand goods and many other types of goods. Rebates for exported goods and GST taxed business inputs are also available

12% or 0% (including but not limited to exports of goods or services, services to a foreign going vessel providing international commercial services, consumable goods for commercially scheduled foreign going vessels/aircraft, copyright, etc.)

VAT = Value Added Tax

Bahrain

10%

0% (pharmacies and medical services, road transport, education service, Oil and gas derivatives, Vegetables and fruits, National exports)

(VAT) ضريبة القيمة المضافة

Bangladesh

15%

4% for supplier, 4.5% for ITES, 5% for electricity, 5.5% for construction firm, etc.

Musok = Mullo songzojon kor মূসক = "মূল্য সংযোজন কর"

Barbados

17.5%

VAT = Value Added Tax

Belarus

20%

10% or 0.5%

ПДВ = Падатак на дададзеную вартасьць

Belize

12.5%

?

Benin

18%

?

Bolivia

13%

IVA = Impuesto al Valor Agregado

Bosnia and Herzegovina

17%

PDV = Porez na dodanu vrijednost

Botswana

12%

?

Brazil

20% (IPI) + 19% (ICMS) average + 3% (ISS) average

0%

*IPI – 20% = Imposto sobre produtos industrializados (Tax over industrialized products) – Federal Tax ICMS – 17 to 25% = Imposto sobre circulação e serviços (tax over commercialization and services) – State Tax ISS – 2 to 5% = Imposto sobre serviço de qualquer natureza (tax over any service)–City tax

Burkina Faso

18%

?

Burundi

18%

?

Cambodia

10%

?

Cameroon

19.25%

?

Canada

5% GST + 0–9.975% PST or 13-15% HST depending on province.

0% [lower-alpha 1] on GST or HST for Prescription drugs, medical devices, basic groceries, agricultural/fishing products, exported or foreign goods, services and travel. Other exemptions exist for PSTs and vary by province.

0% for fresh foods, education, healthcare, land public transportation and medicines. Sales and Services Tax (SST) was reintroduced by the Malaysian Government on 1 September 2018 to replace the Goods and Services Tax (GST) which had only been introduced just over three years before that, on 1 April 2015.[135]

TVA = Taxe sur Valeur Ajoutée (الضريبة على القيمة المضافة)

Mozambique

17%

?

Namibia

15%

0%

VAT = Value Added Tax

Nepal

13%

0%

VAT = Value Added Taxes

New Zealand

15%

0% (donated goods and services sold by non-profits, financial services, rental payments for residential properties, supply of fine metals, and penalty interest).[137]

6% on petroleum products, and electricity and water services 0% for senior citizens (all who are aged 60 and above) on medicines, professional fees for physicians, medical and dental services, transportation fares, admission fees charged by theaters and amusement centers, and funeral and burial services after the death of the senior citizen

RVAT = Reformed Value Added Tax, locally known as Karagdagang Buwis / Dungag nga Buhis

Republic of Congo

16%

?

Russia

20%

10% (essential food, goods for children and medical products)[141] or 0%

НДС = Налог на добавленную стоимость, NDS = Nalog na dobavlennuyu stoimost'

0% on basic foodstuffs such as bread, additionally on goods donated not for gain; goods or services used for educational purposes, such as school computers; membership contributions to an employee organization (such as labour union dues); and rent paid on a house by a renter to a landlord.[144]

VAT = Valued Added Tax has been in effect in Sri Lanka since 2001. On the 2001 budget, the rates have been revised to 12% and 0% from the previous 20%, 12% and 0%

↑ No reduced rate, but rebates generally available for certain services

↑ HST is a combined federal/provincial sales tax collected in some provinces. GST is a 5% federal sales tax collected separately if there is a PST. 5% of HSTs go to the federal government and the remainder to the province.

↑ The reduced rate was 14% until 1 March 2007, when it was lowered to 7%, and later changed to 11%. The reduced rate applies to heating costs, printed matter, restaurant bills, hotel stays, and most food.

↑ VAT is not implemented in 2 of India's 28 states.

↑ The VAT in Israel is in a state of flux. It was reduced from 18% to 17% in March 2004, to 16.5% in September 2005, then to 15.5% in July 2006. It was then raised back to 16.5% in July 2009, and lowered to the rate of 16% in January 2010. It was then raised again to 17% on 1 September 2012, and once again on 2 June 2013, to 18%. It was reduced from 18% to 17% in October 2015.

↑ The introduction of a goods and sales tax of 3% on 6 May 2008 was to replace revenue from Company Income Tax following a reduction in rates.

↑ In the 2014 Budget, the government announced that GST would be introduced in April 2015. Piped water, power supply (the first 200 units per month for domestic consumers), transportation services, education, and health services are tax-exempt. However, many details have not yet been confirmed.[134]

↑ The President of the Philippines has the power to raise the tax to 12% after 1 January 2006. The tax was raised to 12% on 1 February.[140]

VAT-free countries and territories

As of January 2022, the countries and territories listed remained VAT-free.[citation needed]

Just recent tax of 14.85% (hotels) and 10% (restaurants)

Timor Leste

—

Turks and Caicos Islands

British Overseas Territory

Tuvalu

—

United States

Sales taxes are collected by most states and some cities, counties, and Native American reservations. The federal government collects excise tax on some goods, but does not collect a nationwide sales tax.

A sales tax is a tax paid to a governing body for the sales of certain goods and services. Usually laws allow the seller to collect funds for the tax from the consumer at the point of purchase.

The goods and services tax is a value added tax introduced in Canada on January 1, 1991, by the government of Prime Minister Brian Mulroney. The GST, which is administered by Canada Revenue Agency (CRA), replaced a previous hidden 13.5% manufacturers' sales tax (MST).

Goods and Services Tax (GST) in Australia is a value added tax of 10% on most goods and services sales, with some exemptions and concessions. GST is levied on most transactions in the production process, but is in many cases refunded to all parties in the chain of production other than the final consumer.

An ad valorem tax is a tax whose amount is based on the value of a transaction or of a property. It is typically imposed at the time of a transaction, as in the case of a sales tax or value-added tax (VAT). An ad valorem tax may also be imposed annually, as in the case of a real or personal property tax, or in connection with another significant event. In some countries, a stamp duty is imposed as an ad valorem tax.

Goods and Services Tax (GST) is a value-added tax or consumption tax for goods and services consumed in New Zealand.

Tax-free shopping (TFS) is the buying of goods in another country or state and obtaining a refund of the sales tax which has been collected by the retailer on those goods. The sales tax may be variously described as a sales tax, goods and services tax (GST), value added tax (VAT), or consumption tax.

Income taxes are the most significant form of taxation in Australia, and collected by the federal government through the Australian Taxation Office. Australian GST revenue is collected by the Federal government, and then paid to the states under a distribution formula determined by the Commonwealth Grants Commission.

Taxation in Iran is levied and collected by the Iranian National Tax Administration under the Ministry of Finance and Economic Affairs of the Government of Iran. In 2008, about 55% of the government's budget came from oil and natural gas revenues, the rest from taxes and fees. An estimated 50% of Iran's GDP was exempt from taxes in FY 2004. There are virtually millions of people who do not pay taxes in Iran and hence operate outside the formal economy. The fiscal year begins on March 21 and ends on March 20 of the next year.

Goods and Services Tax (GST) in Singapore is a value added tax (VAT) of 9% levied on import of goods, as well as most supplies of goods and services. Exemptions are given for the sales and leases of residential properties, importation and local supply of investment precious metals and most financial services. Export of goods and international services are zero-rated. GST is also absorbed by the government for public healthcare services, such as at public hospitals and polyclinics.

The Tanzania Revenue Authority (TRA) is the government agency of Tanzania, charged with the responsibility of managing the assessment, collection and accounting of all central government revenue in Tanzania.

The European Union value-added tax is a value added tax on goods and services within the European Union (EU). The EU's institutions do not collect the tax, but EU member states are each required to adopt in national legislation a value added tax that complies with the EU VAT code. Different rates of VAT apply in different EU member states, ranging from 17% in Luxembourg to 27% in Hungary. The total VAT collected by member states is used as part of the calculation to determine what each state contributes to the EU's budget.

Taxation in Israel include income tax, capital gains tax, value-added tax and land appreciation tax. The primary law on income taxes in Israel is codified in the Income Tax Ordinance. There are also special tax incentives for new immigrants to encourage aliyah.

In Austria, taxes are levied by the state and the tax revenue in Austria was 42.7% of GDP in 2016 according to the World Bank The most important revenue source for the government is the income tax, corporate tax, social security contributions, value added tax and tax on goods and services. Another important taxes are municipal tax, real-estate tax, vehicle insurance tax, property tax, tobacco tax. There exists no property tax. The gift tax and inheritance tax were cancelled in 2008. Furthermore, self-employed persons can use a tax allowance of €3,900 per year. The tax period is set for a calendar year. However, there is a possibility of having an exception but a permission of the tax authority must be received. The Financial Secrecy Index ranks Austria as the 35th safest tax haven in the world.

The Goods and Services Tax (GST) is an abolished value-added tax in Malaysia. GST is levied on most transactions in the production process, but is refunded with exception of Blocked Input Tax, to all parties in the chain of production other than the final consumer.

Taxation in Norway is levied by the central government, the county municipality and the municipality. In 2012 the total tax revenue was 42.2% of the gross domestic product (GDP). Many direct and indirect taxes exist. The most important taxes – in terms of revenue – are VAT, income tax in the petroleum sector, employers' social security contributions and tax on "ordinary income" for persons. Most direct taxes are collected by the Norwegian Tax Administration and most indirect taxes are collected by the Norwegian Customs and Excise Authorities.

In the United Kingdom, the value added tax (VAT) was introduced in 1973, replacing Purchase Tax, and is the third-largest source of government revenue, after income tax and National Insurance. It is administered and collected by HM Revenue and Customs, primarily through the Value Added Tax Act 1994.

Taxation in Malta is levied by the State and it is administered by the Commissioner for Tax and Customs. The total tax revenues in 2014 amounted to €2.747 Billion, which represents 34.6% of the Maltese GDP. The main sources of tax revenue were value-added tax, income tax, and social security contributions.

A destination-based cash flow tax (DBCFT) is a cashflow tax with a destination-based border-adjustment. Unlike traditional corporate income tax, firms are able to immediately expense all capital investment. This ensures that normal profit is out of the tax base and only super-normal profits are taxed. Additionally, the destination-based border-adjustment is the same as how the Value-Added Tax treat cross-border transactions—by exempting exports but taxing imports.

The organization responsible for tax policy in Ukraine is the State Fiscal Service, operating under the Ministry of Finance of Ukraine. Taxation is legally regulated by the Taxation Code of Ukraine. The calendar year serves as a fiscal year in Ukraine. The most important sources of tax revenue in Ukraine are unified social security contributions, value added tax, individual income tax. In 2017 taxes collected formed 23% of GDP at ₴969.654 billion.

Ethiopia has a long history of taxing its population. As of 2002, reforms have changed the way the tax system works in the nation; these reforms have aimed to centralize tax authority. Currently the nation's federal government lobbies many different types of taxes on its population; these taxes include income taxes on four main schedules, property taxes, and value added taxes (VAT).

↑ Minh Le, Tuan (1 May 2003). Value Added Taxation: Mechanism, Design, and Policy Issues. World Bank. S2CID9409506. the mechanism provides strong incentives for firms to keep invoices

↑ Thacker, Sunil (2008–2009). "Taxation in the Gulf: Introduction of a Value Added Tax". Michigan State Journal of International Law. 17 (3): 721. SSRN1435988.

↑ Trinova Corp. v. Michigan Dept. of Treasury,498U.S.358, 362(United States Supreme Court1991)("Although in Europe and Latin America VAT's are common,...in the United States they are much studied but little used.").

↑ Gulino, Denny (18 September 2015). "Puerto Rico May Finally Get Attention of Republican Lawmakers". MNI. Retrieved 9 February 2016. The concept of a value added tax in any form as part of the U.S. tax regime has consistently raised the hackles of Republican policy makers and even some Democrats because of fears it could add to the tax burden rather than just redistribute it to consumption from earnings. For decades one of the most hotly debated tax policy topics, a VAT imposes a sales tax at every stage where value is added.

↑ "Value added tax". Portal of the Principality of Liechtenstein. Government Spokesperson's Office. Archived from the original on 18 April 2005. Retrieved 13 October 2010.

Ahmed, Ehtisham and Nicholas Stern. 1991. The Theory and Practice of Tax Reform in Developing Countries (Cambridge University Press).

Bird, Richard M. and P.-P. Gendron .1998. "Dual VATs and Cross-border Trade: Two Problems, One Solution?" International Tax and Public Finance, 5: 429–42.

Bird, Richard M. and P.-P. Gendron .2000. "CVAT, VIVAT and Dual VAT; Vertical 'Sharing' and Interstate Trade", International Tax and Public Finance, 7: 753–61.

Keen, Michael and S. Smith .2000. "Viva VIVAT!" International Tax and Public Finance, 7: 741–51.

Keen, Michael and S. Smith .1996. "The Future of Value-added Tax in the European Union", Economic Policy, 23: 375–411.

McLure, Charles E. (1993) "The Brazilian Tax Assignment Problem: Ends, Means, and Constraints", in A Reforma Fiscal no Brasil (São Paulo: Fundaçäo Instituto de Pesquisas Econômicas).

McLure, Charles E. 2000. "Implementing Subnational VATs on Internal Trade: The Compensating VAT (CVAT)", International Tax and Public Finance, 7: 723–40.

Muller, Nichole. 2007. Indisches Recht mit Schwerpunkt auf gewerblichem Rechtsschutz im Rahmen eines Projektgeschäfts in Indien, IBL Review, VOL. 12, Institute of International Business and law, Germany. Law-and-business.de

Muller, Nichole. 2007. Indian law with emphasis on commercial legal insurance within the scope of a project business in India. IBL Review, VOL. 12, Institute of International Business and law, Germany.

OECD. 2008. Consumption Tax Trends 2008: VAT/GST and Excise Rates, Trends and Administration Issues. Paris: OECD.

Serra, J. and J. Afonso. 1999. "Fiscal Federalism Brazilian Style: Some Reflections", Paper presented to Forum of Federations, Mont Tremblant, Canada, October 1999.

Shome, Parthasarathi and Paul Bernd Spahn (1996) "Brazil: Fiscal Federalism and Value Added Tax Reform", Working Paper No. 11, National Institute of Public Finance and Policy, New Delhi

Silvani, Carlos and Paulo dos Santos (1996) "Administrative Aspects of Brazil's Consumption Tax Reform", International VAT Monitor, 7: 123–32.

Tait, Alan A. (1988) Value Added Tax: International Practice and Problems (Washington: International Monetary Fund).

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.