A sales tax is a tax paid to a governing body for the sales of certain goods and services. Usually laws allow the seller to collect funds for the tax from the consumer at the point of purchase.

A fuel tax is an excise tax imposed on the sale of fuel. In most countries the fuel tax is imposed on fuels which are intended for transportation. Fuel tax receipts are often dedicated or hypothecated to transportation projects, in which case the fuel tax can be considered a user fee. In other countries, the fuel tax is a source of general revenue. Sometimes, a fuel tax is used as an ecotax, to promote ecological sustainability. Fuel taxes are often considered by government agencies such as the Internal Revenue Service as regressive taxes.

An ad valorem tax is a tax whose amount is based on the value of a transaction or of a property. It is typically imposed at the time of a transaction, as in the case of a sales tax or value-added tax (VAT). An ad valorem tax may also be imposed annually, as in the case of a real or personal property tax, or in connection with another significant event. In some countries, a stamp duty is imposed as an ad valorem tax.

Entertainment tax also sometimes referred to as "amusement tax" is any tax levied on any form of commercial entertainment, such as movie tickets, exhibitions, sport events and more. The specific rules such as the tax rate of entertainment tax and cases of tax exemption are subject to local authorities, as is their collection. The entertainment tax has in the most cases the form of indirect tax, which is levied on buyer. Nowadays, the most discussed subject of those taxes are their implementations to online services, especially the ones working on streaming basis such as Netflix, Spotify and others.

The tax system of the Russian Federation is a complex of relationships between fiscal authorities and taxpayers in the field of all existing taxes and fees. It implies continuous communication of all its members and related objects: payers; legislative framework; oversight authorities; types of mandatory payments. The Russian Tax Code is the primary tax law for the Russian Federation. The Code was created, adopted and implemented in three stages.

Taxation in Iran is levied and collected by the Iranian National Tax Administration under the Ministry of Finance and Economic Affairs of the Government of Iran. In 2008, about 55% of the government's budget came from oil and natural gas revenues, the rest from taxes and fees. An estimated 50% of Iran's GDP was exempt from taxes in FY 2004. There are virtually millions of people who do not pay taxes in Iran and hence operate outside the formal economy. The fiscal year begins on March 21 and ends on March 20 of the next year.

Taxes in India are levied by the Central Government and the State Governments by virtue of powers conferred to them from the Constitution of India. Some minor taxes are also levied by the local authorities such as the Municipality.

The Tanzania Revenue Authority (TRA) is the government agency of Tanzania, charged with the responsibility of managing the assessment, collection and accounting of all central government revenue in Tanzania.

An excise, or excise tax, is any duty on manufactured goods that is normally levied at the moment of manufacture for internal consumption rather than at sale. It is therefore a fee that must be paid in order to consume certain products. Excises are often associated with customs duties, which are levied on pre-existing goods when they cross a designated border in a specific direction; customs are levied on goods that become taxable items at the border, while excise is levied on goods that came into existence inland.

Taxes provide the most important revenue source for the Government of the People's Republic of China. Tax is a key component of macro-economic policy, and greatly affects China's economic and social development. With the changes made since the 1994 tax reform, China has sought to set up a streamlined tax system geared to a socialist market economy.

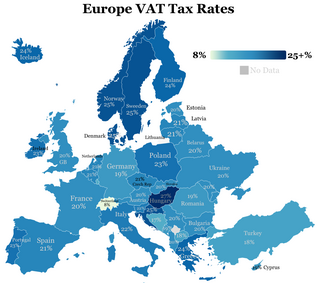

The European Union value-added tax is a value added tax on goods and services within the European Union (EU). The EU's institutions do not collect the tax, but EU member states are each required to adopt in national legislation a value added tax that complies with the EU VAT code. Different rates of VAT apply in different EU member states, ranging from 17% in Luxembourg to 27% in Hungary. The total VAT collected by member states is used as part of the calculation to determine what each state contributes to the EU's budget.

Service tax was a tax levied by the Government of India on services provided or agreed to be provided excluding services covered under the negative list and considering the Place of Provision of Service Rules 2012 and collected as per Point of Taxation Rules 2011 from the person liable to pay service tax.

Taxes in Germany are levied at various government levels: the federal government, the 16 states (Länder), and numerous municipalities (Städte/Gemeinden). The structured tax system has evolved significantly, since the reunification of Germany in 1990 and the integration within the European Union, which has influenced tax policies. Today, income tax and Value-Added Tax (VAT) are the primary sources of tax revenue. These taxes reflect Germany's commitment to a balanced approach between direct and indirect taxation, essential for funding extensive social welfare programs and public infrastructure. The modern German tax system accentuate on fairness and efficiency, adapting to global economic trends and domestic fiscal needs.

The policy of taxation in the Philippines is governed chiefly by the Constitution of the Philippines and three Republic Acts.

The Sixth Amendment of the Constitution of India, officially known as The Constitution Act, 1956, brought taxes on inter-State sales and purchases of goods other than newspapers within the exclusive legislative and executive power of the Union, and levied taxes on inter-State sales and purchase of goods other than newspapers. Although these taxes would be levied and collected in accordance with an Act of Parliament, they would not form part of the Consolidated Fund of India, but would accrue to the States themselves in accordance with such principles of distribution as may be formulated by Parliament by law.

In Slovakia, taxes are levied by the state and local governments. Tax revenue stood at 19.3% of the country's gross domestic product in 2021. The tax-to-GDP ratio in Slovakia deviates from OECD average of 34.0% by 0.8 percent and in 2022 was 34.8% which ranks Slovakia 19th in the tax-to-GDP ratio comparison among the OECD countries. The most important revenue sources for the state government are income tax, social security, value-added tax and corporate tax.

Taxes in Bulgaria are collected on both state and local levels. The most important taxes are collected on state level, these taxes include income tax, social security, corporate taxes and value added tax. On the local level, property taxes as well as various fees are collected. All income earned in Bulgaria is taxed on a flat rate of 10%. Employment income earned in Bulgaria is also subject to various social security insurance contributions. In total the employee pays 12.9% and the employer contributes what corresponds to 17.9%. Corporate income tax is also a flat 10%. Value-Added Tax applies at a flat rate of 20% on virtually all goods and services. A lower rate of 9% applies on only hotel services.

The Goods and Services Tax (GST) is a successor to VAT used in India on the supply of goods and service. Both VAT and GST have the same taxation slabs. It is a comprehensive, multistage, destination-based tax: comprehensive because it has subsumed almost all the indirect taxes except a few state taxes. Multi-staged as it is, the GST is imposed at every step in the production process, but is meant to be refunded to all parties in the various stages of production other than the final consumer and as a destination-based tax, it is collected from point of consumption and not point of origin like previous taxes.

A value-added tax (VAT or goods and services tax (GST), general consumption tax (GCT)), is a consumption tax that is levied on the value added at each stage of a product's production and distribution. VAT is similar to, and is often compared with, a sales tax. VAT is an indirect tax because the consumer who ultimately bears the burden of the tax is not the entity that pays it. Specific goods and services are typically exempted in various jurisdictions.

Ethiopia has a long history of taxing its population. As of 2002, reforms have changed the way the tax system works in the nation; these reforms have aimed to centralize tax authority. Currently the nation's federal government lobbies many different types of taxes on its population; these taxes include income taxes on four main schedules, property taxes, and value added taxes (VAT).