In finance, a derivative is a contract that derives its value from the performance of an underlying entity. This underlying entity can be an asset, index, or interest rate, and is often simply called the underlying. Derivatives can be used for a number of purposes, including insuring against price movements (hedging), increasing exposure to price movements for speculation, or getting access to otherwise hard-to-trade assets or markets.

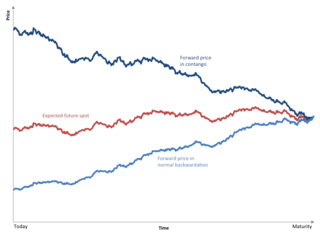

Contango is a situation in which the futures price of a commodity is higher than the expected spot price of the contract at maturity. In a contango situation, arbitrageurs or speculators are "willing to pay more [now] for a commodity [to be received] at some point in the future than the actual expected price of the commodity [at that future point]. This may be due to people's desire to pay a premium to have the commodity in the future rather than paying the costs of storage and carry costs of buying the commodity today." On the other side of the trade, hedgers are happy to sell futures contracts and accept the higher-than-expected returns. A contango market is also known as a normal market or carrying-cost market.

In finance, being short in an asset means investing in such a way that the investor will profit if the market value of the asset falls. This is the opposite of the more common long position, where the investor will profit if the market value of the asset rises. An investor that sells an asset short is, as to that asset, a short seller.

In finance, a put or put option is a derivative instrument in financial markets that gives the holder the right to sell an asset, at a specified price, by a specified date to the writer of the put. The purchase of a put option is interpreted as a negative sentiment about the future value of the underlying stock. The term "put" comes from the fact that the owner has the right to "put up for sale" the stock or index.

In finance, a warrant is a security that entitles the holder to buy or sell stock, typically the stock of the issuing company, at a fixed price called the exercise price.

In finance, a futures contract is a standardized legal contract to buy or sell something at a predetermined price for delivery at a specified time in the future, between parties not yet known to each other. The asset transacted is usually a commodity or financial instrument. The predetermined price of the contract is known as the forward price or delivery price. The specified time in the future when delivery and payment occur is known as the delivery date. Because it derives its value from the value of the underlying asset, a futures contract is a derivative.

In finance, an equity derivative is a class of derivatives whose value is at least partly derived from one or more underlying equity securities. Options and futures are by far the most common equity derivatives, however there are many other types of equity derivatives that are actively traded.

A hedge is an investment position intended to offset potential losses or gains that may be incurred by a companion investment. A hedge can be constructed from many types of financial instruments, including stocks, exchange-traded funds, insurance, forward contracts, swaps, options, gambles, many types of over-the-counter and derivative products, and futures contracts.

In finance, a contract for difference (CFD) is a financial agreement between two parties, commonly referred to as the "buyer" and the "seller." The contract stipulates that the buyer will pay the seller the difference between the current value of an asset and its value at the time the contract was initiated. If the asset's price increases from the opening to the closing of the contract, the seller compensates the buyer for the increase, which constitutes the buyer's profit. Conversely, if the asset's price decreases, the buyer compensates the seller, resulting in a profit for the seller.

In finance, a long position in a financial instrument means the holder of the position owns a positive amount of the instrument. The holder of the position has the expectation that the financial instrument will increase in value. This is known as a bullish position.

The owner of an option contract has the right to exercise it, and thus require that the financial transaction specified by the contract is to be carried out immediately between the two parties, whereupon the option contract is terminated. When exercising a call option, the owner of the option purchases the underlying shares at the strike price from the option seller, while for a put option, the owner of the option sells the underlying to the option seller, again at the strike price.

In finance, a collar is an option strategy that limits the range of possible positive or negative returns on an underlying to a specific range. A collar strategy is used as one of the ways to hedge against possible losses and it represents long put options financed with short call options. The collar combines the strategies of the protective put and the covered call.

Option strategies are the simultaneous, and often mixed, buying or selling of one or more options that differ in one or more of the options' variables. Call options, simply known as Calls, give the buyer a right to buy a particular stock at that option's strike price. Opposite to that are Put options, simply known as Puts, which give the buyer the right to sell a particular stock at the option's strike price. This is often done to gain exposure to a specific type of opportunity or risk while eliminating other risks as part of a trading strategy. A very straightforward strategy might simply be the buying or selling of a single option; however, option strategies often refer to a combination of simultaneous buying and or selling of options.

Pin risk occurs when the market price of the underlier of an option contract at the time of the contract's expiration is close to the option's strike price. In this situation, the underlier is said to have pinned. The risk to the writer (seller) of the option is that they cannot predict with certainty whether the option will be exercised or not. So the writer cannot hedge their position precisely and may end up with a loss or gain. There is a chance that the price of the underlier may move adversely, resulting in an unanticipated loss to the writer. In other words, an option position may result in a large, undesired risky position in the underlier immediately after expiration, regardless of the actions of the writer.

In finance, an option is a contract which conveys to its owner, the holder, the right, but not the obligation, to buy or sell a specific quantity of an underlying asset or instrument at a specified strike price on or before a specified date, depending on the style of the option.

In finance, a stock market index future is a cash-settled futures contract on the value of a particular stock market index. The turnover for the global market in exchange-traded equity index futures is notionally valued, for 2008, by the Bank for International Settlements at US$130 trillion.

A reverse convertible security is a type of convertible security where a bond or short-term note can be converted to cash, debt or equity at a set date by the issuer based on an underlying stock. In effect it is a type of option on the maturity date where the bond can be converted to shares or cash. For the investor they get the advantage of a steady stream of income due to the payment of a high coupon rate, but will either get back their principle or a predetermined number of shares in the underlying stock if they are lower. The coupon rate is typically higher because the investor participates in the risk that the underlying shares are lower at the maturity date.

In finance a covered warrant is a type of warrant that has been issued without an accompanying bond or equity. Like a normal warrant, it allows the holder to buy or sell a specific amount of equities, currency, or other financial instruments from the issuer at a specified price at a predetermined date.

Stocks consist of all the shares by which ownership of a corporation or company is divided. A single share of the stock means fractional ownership of the corporation in proportion to the total number of shares. This typically entitles the shareholder (stockholder) to that fraction of the company's earnings, proceeds from liquidation of assets, or voting power, often dividing these up in proportion to the number of like shares each stockholder owns. Not all stock is necessarily equal, as certain classes of stock may be issued, for example, without voting rights, with enhanced voting rights, or with a certain priority to receive profits or liquidation proceeds before or after other classes of shareholders.

Sharia and securities trading is the impact of conventional financial markets activity for those following the islamic religion and particularly sharia law. Sharia practices ban riba and involvement in haram. It also forbids gambling (maisir) and excessive risk. This, however has not stopped some in Islamic finance industry from using some of these instruments and activities, but their permissibility is a subject of "heated debate" within the religion.