A debit card, also known as a check card or bank card is a payment card that can be used in place of cash to make purchases. The term plastic card includes the above and as an identity document. These are similar to a credit card, but unlike a credit card, the money for the purchase must be in the cardholder's bank account at the time of a purchase and is immediately transferred directly from that account to the merchant's account to pay for the purchase.

An automated teller machine (ATM) is an electronic telecommunications device that enables customers of financial institutions to perform financial transactions, such as cash withdrawals, deposits, funds transfers, balance inquiries or account information inquiries, at any time and without the need for direct interaction with bank staff.

The Society for Worldwide Interbank Financial Telecommunication (SWIFT), legally S.W.I.F.T. SC, is a Belgian cooperative society providing services related to the execution of financial transactions and payments between certain banks worldwide. Its principal function is to serve as the main messaging network through which international payments are initiated. It also sells software and services to financial institutions, mostly for use on its proprietary "SWIFTNet", and assigns ISO 9362 Business Identifier Codes (BICs), popularly known as "SWIFT codes".

A smart card, chip card, or integrated circuit card is a physical electronic authentication device, used to control access to a resource. It is typically a plastic credit card-sized card with an embedded integrated circuit (IC) chip. Many smart cards include a pattern of metal contacts to electrically connect to the internal chip. Others are contactless, and some are both. Smart cards can provide personal identification, authentication, data storage, and application processing. Applications include identification, financial, public transit, computer security, schools, and healthcare. Smart cards may provide strong security authentication for single sign-on (SSO) within organizations. Numerous nations have deployed smart cards throughout their populations.

A mobile payment, also referred to as mobile money, mobile money transfer and mobile wallet, is any of various payment processing services operated under financial regulations and performed from or via a mobile device, as the cardinal class of digital wallet. Instead of paying with cash, cheque, or credit cards, a consumer can use a payment app on a mobile device to pay for a wide range of services and digital or hard goods. Although the concept of using non-coin-based currency systems has a long history, it is only in the 21st century that the technology to support such systems has become widely available.

Hazard analysis and critical control points, or HACCP, is a systematic preventive approach to food safety from biological, chemical, and physical hazards in production processes that can cause the finished product to be unsafe and designs measures to reduce these risks to a safe level. In this manner, HACCP attempts to avoid hazards rather than attempting to inspect finished products for the effects of those hazards. The HACCP system can be used at all stages of a food chain, from food production and preparation processes including packaging, distribution, etc. The Food and Drug Administration (FDA) and the United States Department of Agriculture (USDA) require mandatory HACCP programs for juice and meat as an effective approach to food safety and protecting public health. Meat HACCP systems are regulated by the USDA, while seafood and juice are regulated by the FDA. All other food companies in the United States that are required to register with the FDA under the Public Health Security and Bioterrorism Preparedness and Response Act of 2002, as well as firms outside the US that export food to the US, are transitioning to mandatory hazard analysis and risk-based preventive controls (HARPC) plans.

A personal identification number (PIN), or sometimes redundantly a PIN number or PIN code, is a numeric passcode used in the process of authenticating a user accessing a system.

A micropayment is a financial transaction involving a very small sum of money and usually one that occurs online. A number of micropayment systems were proposed and developed in the mid-to-late 1990s, all of which were ultimately unsuccessful. A second generation of micropayment systems emerged in the 2010s.

EMV is a payment method based on a technical standard for smart payment cards and for payment terminals and automated teller machines which can accept them. EMV stands for "Europay, Mastercard, and Visa", the three companies that created the standard.

The Reserve Bank of Australia (RBA) is Australia's central bank and banknote issuing authority. It has had this role since 14 January 1960, when the Reserve Bank Act 1959 removed the central banking functions from the Commonwealth Bank.

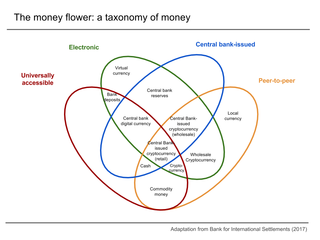

Digital currency is any currency, money, or money-like asset that is primarily managed, stored or exchanged on digital computer systems, especially over the internet. Types of digital currencies include cryptocurrency, virtual currency and central bank digital currency. Digital currency may be recorded on a distributed database on the internet, a centralized electronic computer database owned by a company or bank, within digital files or even on a stored-value card.

Chipknip was a stored-value payment card system used in the Netherlands. Based on the Belgian Proton system, it was started by Interpay on October 26, 1995, as a pilot project in the city of Arnhem and a year later rolled out countrywide. Chipknip was taken over by Currence due to a restructuring on May 17, 2005, who managed it with their licensees until its discontinuation on January 1, 2015. The Chipknip was primarily used for small retail transactions, as the card could contain a maximum value of 500 euros. The money needed to be transferred from a card holders main bank account using a loading station which were generally located next to ATMs.

Contactless payment systems are credit cards and debit cards, key fobs, smart cards, or other devices, including smartphones and other mobile devices, that use radio-frequency identification (RFID) or near-field communication for making secure payments. The embedded integrated circuit chip and antenna enable consumers to wave their card, fob, or handheld device over a reader at the Point-of-sale terminal. Contactless payments are made in close physical proximity, unlike other types of mobile payments which use broad-area cellular or WiFi networks and do not involve close physical proximity.

Paysafecard is a prepaid online payment method based on vouchers with a 16-digit PIN code, independent of bank account, credit card, or other personal information. Customers can purchase vouchers at local sales outlets and pay online by entering the code at the checkout of the respective website. Paysafecard codes are not designated to be passed by mail or telephone.

iDEAL is e-commerce payment system used for online banking in the Netherlands. It is an online payment method that enables consumers to pay online through their own bank. In addition to online merchants, other organisations that are not part of the e-commerce market also offer iDEAL.

The Bureau of Indian Standards (BIS) is the National Standards Body of India under Department of Consumer affairs, Ministry of Consumer Affairs, Food & Public Distribution, Government of India. It is established by the Bureau of Indian Standards Act, 2016 which came into effect on 12 October 2017. The Minister in charge of the Ministry or Department having administrative control of the BIS is the ex-officio President of the BIS. BIS has 500 plus scientific officers working as Certification Officers, Member secretaries of technical committees and lab OIC's.

Fair trade coffee is coffee that is certified as having been produced to fair trade standards by fair trade organizations, which create trading partnerships that are based on dialogue, transparency and respect, with the goal of achieving greater equity in international trade. These partnerships contribute to sustainable development by offering better trading conditions to coffee bean farmers. Fair trade organizations support producers and sustainable environmental farming practices and prohibit child labor or forced labor.

Utimaco Atalla, founded as Atalla Technovation and formerly known as Atalla Corporation or HP Atalla, is a security vendor, active in the market segments of data security and cryptography. Atalla provides government-grade end-to-end products in network security, and hardware security modules (HSMs) used in automated teller machines (ATMs) and Internet security. The company was founded by Egyptian engineer Mohamed M. Atalla in 1972. Atalla HSMs are the payment card industry's de facto standard, protecting 250 million card transactions daily as of 2013, and securing the majority of the world's ATM transactions as of 2014.

iVeri is a payments technology company that facilitates transaction acceptance for banks and businesses. The company is based in Johannesburg, South Africa. Established in 1998, it is South Africa's largest technology provider for both physical and mobile commerce.

PIN was a debit card brand in the Netherlands from 1990 until 2012, owned by Currence. PIN was a magnetic stripe card, which never migrated to the EMV chip. It was therefore discontinued in 2012, after the switch-over from magnetic stripe authentication to EMV chip authentication in the Netherlands was completed. PIN was replaced by Maestro and V Pay debit cards, but as most PIN cards were already co-branded with Maestro long before 2012, consumers noticed little of the change.