As explained in the Talk page this article was created under a student programme with many edits being plan copy pasted texts. The article wasn't improved for a long time, and perhaps more fundamentally the scope of the article is very, very broad and too vague. Of course fiscal & monetary policy interact a lot, but it seems this concept is already covered by macroeconomics(proposed by Stanjourdan )

If you can address this concern by improving, copyediting, sourcing, renaming, or merging the page, please edit this page and do so. You may remove this message if you improve the article or otherwise object to deletion for any reason. Although not required, you are encouraged to explain why you object to the deletion, either in your edit summary or on the talk page. If this template is removed, do not replace it.

The article may be deleted if this message remains in place for seven days, i.e., after 15:44, 30 December 2020 (UTC). If you created the article, please don't be offended. Instead, consider improving the article so that it is acceptable according to the deletion policy. Find sources:"Interaction between monetary and fiscal policies"–news·newspapers·books·scholar·JSTORPRODExpired+%5B%5BWP%3APROD%7CPROD%5D%5D%2C+concern+was%3A+As+explained+in+the+Talk+page+this+article+was+created+under+a+student+programme+with+many+edits+being+plan+copy+pasted+texts.+The+article+wasn%27t+improved+for+a+long+time%2C+and+perhaps+more+fundamentally+the+scope+of+the+article+is+very%2C+very+broad+and+too+vague.+Of+course+fiscal+%26+monetary+policy+interact+a+lot%2C+but+it+seems+this+concept+is+already+covered+by+%5B%5Bmacroeconomics%5D%5DExpired [[WP:PROD|prod]], concern was: As explained in the Talk page this article was created under a student programme with many edits being plan copy pasted texts. The article wasn't improved for a long time, and perhaps more fundamentally the scope of the article is very, very broad and too vague. Of course fiscal & monetary policy interact a lot, but it seems this concept is already covered by macroeconomics

Nominator: Please consider notifying the author/project: {{subst:proposed deletion notify|Interaction between monetary and fiscal policies|concern=As explained in the Talk page this article was created under a student programme with many edits being plan copy pasted texts. The article wasn't improved for a long time, and perhaps more fundamentally the scope of the article is very, very broad and too vague. Of course fiscal & monetary policy interact a lot, but it seems this concept is already covered by [[macroeconomics]]}} ~~~~

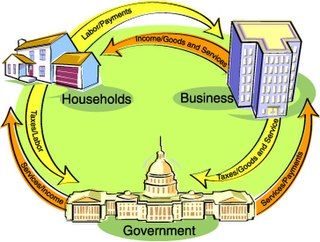

Fiscal policy and monetary policy are the two tools used by the state to achieve its macroeconomic objectives. While for many countries the main objective of fiscal policy is to increase the aggregate output of the economy, the main objective of the monetary policies is to control the interest and inflation rates. The IS/LM model is one of the models used to depict the effect of policy interactions on aggregate output and interest rates. The fiscal policies have a direct impact on the goods market and the monetary policies have a direct impact on the asset markets; since the two markets are connected to each other via the two macrovariables output and interest rates, the policies interact while influencing output and interest rates.

Traditionally, both the policy instruments were under the control of the national governments. Thus traditional analyses were made with respect to the two policy instruments to obtain the optimum policy mix of the two to achieve macroeconomic goals, lest the two policy tools be aimed at mutually inconsistent targets. But more recently, owing to the transfer of control with respect to monetary policy formulation to central banks, formation of monetary unions (like European Monetary Union formed via the Stability and Growth Pact), and attempts being made to form fiscal unions, there has been a significant structural change in the way in which fiscal and monetary policies interact.

There is a dilemma as to whether these two policies are complementary, or act as substitutes to each other for achieving macroeconomic goals. Policy makers are viewed as interacting as strategic substitutes when one policy maker's expansionary (contractionary) policies are countered by another policy maker's contractionary (expansionary) policies. For example: if the fiscal authority raises taxes or cuts spending, then the monetary authority reacts to it by lowering the policy rates and vice versa. If they behave as strategic complements, then an expansionary (contractionary) policy of one authority is met by expansionary (contractionary) policies of the other.

The issue of interaction and the policies being complements or substitutes for each other arises only when the authorities are independent of each other. But when the goals of one authority are made subservient to those of the other, then one authority solely dominates the policy making and no interaction worthy of analysis would arise. Also, fiscal and monetary policies interact only to the extent of influencing the final objective. So long as the objectives of one policy are not influenced by the other, there is no direct interaction between them.

Active and passive monetary and fiscal policies

Professor Eric Leeper has defined terminology as follows:[1]

Passive fiscal policy is one in which the authority raises or reduces taxes to balance the budget intertemporally.

Active fiscal policy is one in which the tax and spending levels are determined independently of intertemporal budget consideration.

Active monetary policy is one that pursues its inflation target independent of fiscal policies.

Passive monetary policy is one that sets interest rates to accommodate fiscal policies.

In case of active fiscal policy and a passive monetary policy, when the economy faces an expansionary fiscal shock that raises the price level, money growth passively increases as well because the monetary authority is forced to accommodate these shocks. But in case both the authorities are active, then the expansionary pressures created by the fiscal authority are contained to some extent by the monetary policies.

Supply shock

During a negative supply shock, the fiscal and monetary authorities may follow conflicting policies if they do not coordinate, as the fiscal authorities would follow expansionary policies to bring the output back to its original state while the monetary authorities would follow contractionary policies so as to reduce the inflation created due to the cutback in output caused by the supply shock.

Demand shock

During a demand shock (a sudden significant rise or fall in aggregate demand due to external factors) without a corresponding change in output, inflation or deflation may result. Here monetary and fiscal policies may work in harmony. Both the authorities would follow expansionary policies in case of a negative demand shock in order to bring back the demand at its original state while they would follow contractionary policies during a positive demand shock in order to reduce the excess aggregate demand and bring inflation under control.

Fiscal shock and policy rate shock

In the case of a positive fiscal shock (increase in fiscal deficits), aggregate output may rise beyond potential (sustainable) output due to the fiscally induced rise in aggregate demand. Subsequently, this leads to dissavings and lowering of investments which would depress output in the long run. Monetary authorities react in a countercyclical way to this, tightening monetary policy in the short run but perhaps, in the long run, adopting quantitative easing to counter the longer-term fall in output.

In case of policy shocks consisting of a sudden positive (negative) change in banking policy rates such as the statutory liquidity ratio, cash reserve ratio or the repo rates, the fiscal authority initially reacts by following expansionary (contractionary) policy but subsequently reverses.

Presence of monetary union

When an economy is a part of a monetary union, its monetary authority is no longer able to conduct its monetary policies independently in response to the needs of the economy. Under such a situation the interaction between fiscal and monetary policies undergoes certain changes. Generally, the monetary union follows policies to keep the overall inflation at such levels so as to keep the overall gap between the actual aggregate consumption and desired consumption close to zero.

Fiscal policies are then used to minimize the country-specific welfare losses arising out of such policies. Also, fiscal policies are used to stabilize the terms of trade and maintain them at their natural levels. Given the common monetary policies and the price levels for all the nations under the union, the fiscal authority of the home country is led to follow contractionary policies in case of deterioration in terms of trade.

Effect of price rigidities

In the case of a supply shock, while the weighted average inflation is at optimum levels, the inflation levels of the nations hit by such a shock may be far from optimum. In such a scenario, given that the degrees of price rigidity in all the nations are equal, the fiscal policies would achieve the dual goal of attaining optimum public spending and maintaining the natural levels of terms of trade only when the shocks hitting the nations under the union are perfectly correlated; otherwise either of the objectives is achieved at the cost of other as monetary policies fail to influence the terms of trade.

But in case of varying degrees of price rigidities amongst the nations, the terms of trade are no longer insulated from monetary policies. This is so because the monetary policies would be directed towards keeping the inflation of the nations with a higher degree of price rigidities at optimum levels so as to reduce their terms of trade losses and the fiscal policies of the rest of the countries would assume a relatively effective role in stabilizing the national inflation as the price levels would respond to the change in public spendings. In short, lower the degree of price rigidities in an economy belonging to a monetary union, the greater would be the relative role of fiscal policies in economic stabilization.

Fiscal monetary interaction in the European Monetary Union

The European Central Bank was created in December 1998 and from 1999 onwards the euro became the official currency of the member nations of the European Monetary Union, and a single monetary policy was adopted under the European Central Bank. To ensure that the member nations meet the conditions for an optimum currency area, potential member nations were asked to commit to the following convergence criteria as spelled out in the Maastricht Treaty:

Central Bank independence

A stability-oriented monetary policy with the primary objective of maintaining price stability

Obligations of the member states to treat the economic policies, in particular, fiscal policies as a matter of common concern.[2]

In addition to the above requirements, members were to maintain exchange rates within a specific band and bring inflation, long-term interest rates, and budget deficits to levels specified in the Treaty. Meeting these criteria forced the member nations to restrict the adoption of stabilizing fiscal policies and concentrate on inflation rates to bring them down to the levels spelled out in the Treaty. This led to changes in the structure of monetary-fiscal interactions in the member nations.

"The Interaction of Fiscal and Monetary Policies: Some Evidences using Structural Econometric Models" by Anton Muscatelli et al.

"Stabilising Output and Inflation in EMU: Policy Conflicts and Cooperation under the Stability Pact" by Buti Marco and Roeger W.

Macroeconomics by N. Gregory Mankiw 7th Edition, Worth Publishers, Harvard University

"Monetary and Fiscal Policy Interactions in a Microfounded Model of a Monetary Union" by Roel M.W.J.Beetsma and Henrik Jensen (2002): European Central Bank Working Paper No. 166

"Monetary and Fiscal Policy Interaction: The Current Consensus Assignment in the light of Recent Developments" by Tatiana Kirsanova et al.

Keynesian economics are various macroeconomic theories about how economic output is strongly influenced by aggregate demand. In the Keynesian view, aggregate demand does not necessarily equal the productive capacity of the economy. Instead, it is influenced by a host of factors. According to Keynes, the productive capacity of the economy sometimes behaves erratically, affecting production, employment, and inflation.

Macroeconomics is a branch of economics dealing with the performance, structure, behavior, and decision-making of an economy as a whole. For example, using interest rates, taxes and government spending to regulate an economy’s growth and stability. This includes regional, national, and global economies.

In economics, stagflation or recession-inflation is a situation in which the inflation rate is high, the economic growth rate slows, and unemployment remains steadily high. It presents a dilemma for economic policy, since actions intended to lower inflation may exacerbate unemployment.

In economics, inflation is a general rise in the price level in an economy over a period of time. When the general price level rises, each unit of currency buys fewer goods and services; consequently, inflation reflects a reduction in the purchasing power per unit of money – a loss of real value in the medium of exchange and unit of account within the economy. The opposite of inflation is deflation, a sustained decrease in the general price level of goods and services. The common measure of inflation is the inflation rate, the annualized percentage change in a general price index, usually the consumer price index, over time.

New Keynesian economics is a school of macroeconomics that strives to provide microeconomic foundations for Keynesian economics. It developed partly as a response to criticisms of Keynesian macroeconomics by adherents of new classical macroeconomics.

In economics and political science, fiscal policy is the use of government revenue collection and expenditure (spending) to influence a country's economy. The use of government revenues and expenditures to influence macroeconomic variables developed as a result of the Great Depression, when the previous laissez-faire approach to economic management became unpopular. Fiscal policy is based on the theories of the British economist John Maynard Keynes, whose Keynesian economics theorized that government changes in the levels of taxation and government spending influences aggregate demand and the level of economic activity. Fiscal and monetary policy are the key strategies used by a country's government and central bank to advance its economic objectives. The combination of these policies enables these authorities to target inflation and to increase employment. Additionally, it is designed to try to keep GDP growth at 2%–3% and the unemployment rate near the natural unemployment rate of 4%–5%. This implies that fiscal policy is used to stabilize the economy over the course of the business cycle.

Monetary policy the policy adopted by the monetary authority of a nation to control either the interest rate payable for very short-term borrowing or the money supply, often as an attempt to reduce inflation or the interest rate to ensure price stability and general trust of the value and stability of the nation's currency.

Nominal rigidity, also known as price-stickiness or wage-stickiness, is a situation in which a nominal price is resistant to change. Complete nominal rigidity occurs when a price is fixed in nominal terms for a relevant period of time. For example, the price of a particular good might be fixed at $10 per unit for a year. Partial nominal rigidity occurs when a price may vary in nominal terms, but not as much as it would if perfectly flexible. For example, in a regulated market there might be limits to how much a price can change in a given year.

Neo-Keynesian economics is a school of macroeconomic thought that was developed in the post-war period from the writings of John Maynard Keynes. A group of economists, attempted to interpret and formalize Keynes' writings and to synthesize it with the neoclassical models of economics. Their work has become known as the neoclassical synthesis and created the models that formed the core ideas of neo-Keynesian economics. These ideas dominated mainstream economics in the post-war period and formed the mainstream of macroeconomic thought in the 1950s, 1960s and 1970s.

Fiscalism is a term sometimes used to refer the economic theory that the government should rely on fiscal policy as the main instrument of macroeconomic policy. Fiscalism in this sense is contrasted with monetarism, which is associated with reliance on monetary policy. Fiscalists reject monetarism in a non-convertible floating rate system as inefficient if not also ineffective

An inflationary gap, in economics, is the amount by which the actual gross domestic product exceeds potential full-employment GDP. It is one type of output gap, the other being a recessionary gap.

In monetary economics, the demand for money is the desired holding of financial assets in the form of money: that is, cash or bank deposits rather than investments. It can refer to the demand for money narrowly defined as M1, or for money in the broader sense of M2 or M3.

Dynamic stochastic general equilibrium modeling is a method in macroeconomics that attempts to explain economic phenomena, such as economic growth and business cycles, and the effects of economic policy, through econometric models based on applied general equilibrium theory and microeconomic principles.

The AD–AS or aggregate demand–aggregate supply model is a macroeconomic model that explains price level and output through the relationship of aggregate demand and aggregate supply.

Macroeconomic theory has its origins in the study of business cycles and monetary theory. In general, early theorists believed monetary factors could not affect real factors such as real output. John Maynard Keynes attacked some of these "classical" theories and produced a general theory that described the whole economy in terms of aggregates rather than individual, microeconomic parts. Attempting to explain unemployment and recessions, he noticed the tendency for people and businesses to hoard cash and avoid investment during a recession. He argued that this invalidated the assumptions of classical economists who thought that markets always clear, leaving no surplus of goods and no willing labor left idle.

In economics, divine coincidence refers to the property of New Keynesian models that there is no trade-off between the stabilization of inflation and the stabilization of the welfare-relevant output gap for central banks. This property is attributed to a feature of the model, namely the absence of real imperfections such as real wage rigidities. Conversely, if New Keynesian models are extended to account for these real imperfections, divine coincidence disappears and central banks again face a trade-off between inflation and output gap stabilization. The definition of divine coincidence is usually attributed to the seminal article by Olivier Blanchard and Jordi Galí in 2007.

Simon Wren-Lewis is a British economist. He is a professor of economic policy at the Blavatnik School of Government at Oxford University and a Fellow of Merton College.

The Taylor contract or staggered contract was first formulated by John B. Taylor in his two articles, in 1979 "Staggered wage setting in a macro model'. and in 1980 "Aggregate Dynamics and Staggered Contracts". In its simplest form, one can think of two equal sized unions who set wages in an industry. Each period, one of the unions sets the nominal wage for two periods. This means that in any one period, only one of the unions can reset its wage and react to events that have just happened. When the union sets its wage, it sets it for a known and fixed period of time. Whilst it will know what is happening in the first period when it sets the new wage, it will have to form expectations about the factors in the second period that determine the optimal wage to set. Although the model was first used to model wage setting, in new Keynesian models that followed it was also used to model price-setting by firms.

Emi Nakamura is an American economist and the Chancellor's Professor of Economics at University of California, Berkeley.

Jón Steinsson is Chancellor's Professor of Economics at University of California, Berkeley, a research associate and co-director of the Monetary Economics program of the National Bureau of Economic Research, and associate editor of both American Economic Review: Insights, and the Quarterly Journal of Economics. He received his PhD in economics from Harvard and his AB from Princeton.

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.