External links

| International | |

|---|---|

| National | |

| Other | |

John E. Floyd | |

|---|---|

| Born | May 6, 1937 |

| Nationality | Canadian |

| Alma mater | University of Saskatchewan University of Chicago |

| Scientific career | |

| Fields | Economics |

| Institutions | University of Toronto, University of Washington |

John E. Floyd (born May 6, 1937, in Moose Jaw, Saskatchewan) is a Canadian economist and member of the University of Toronto faculty. [1]

Floyd received his B.Comm. from the University of Saskatchewan in 1958, and continued to obtain an honours economics degree in 1959. He later obtained M.A. and Ph.D. from the University of Chicago in 1962 and 1964 respectively.

Before coming to the University of Toronto in 1970, Floyd spent 9 years at the University of Washington. He joined the Washington faculty as an assistant professor in 1962, and was promoted to associate professor in 1966 and full professor in 1970.

Since 1970, Floyd has been a professor in the Department of Economics at the University of Toronto.

| International | |

|---|---|

| National | |

| Other | |

A gold standard is a monetary system in which the standard economic unit of account is based on a fixed quantity of gold. The gold standard was the basis for the international monetary system from the 1870s to the early 1920s, and from the late 1920s to 1932 as well as from 1944 until 1971 when the United States unilaterally terminated convertibility of the US dollar to gold, effectively ending the Bretton Woods system. Many states nonetheless hold substantial gold reserves.

In economics, inflation is a general increase in the prices of goods and services in an economy. This is usually measured using the consumer price index (CPI). When the general price level rises, each unit of currency buys fewer goods and services; consequently, inflation corresponds to a reduction in the purchasing power of money. The opposite of CPI inflation is deflation, a decrease in the general price level of goods and services. The common measure of inflation is the inflation rate, the annualized percentage change in a general price index. As prices faced by households do not all increase at the same rate, the consumer price index (CPI) is often used for this purpose.

Robert Alexander Mundell was a Canadian economist. He was a professor of economics at Columbia University and the Chinese University of Hong Kong.

Monetary policy is the policy adopted by the monetary authority of a nation to affect monetary and other financial conditions to accomplish broader objectives like high employment and price stability. Further purposes of a monetary policy may be to contribute to economic stability or to maintain predictable exchange rates with other currencies. Today most central banks in developed countries conduct their monetary policy within an inflation targeting framework, whereas the monetary policies of most developing countries' central banks target some kind of a fixed exchange rate system. A third monetary policy strategy, targeting the money supply, was widely followed during the 1980s, but has diminished in popularity since that, though it is still the official strategy in a number of emerging economies.

In international economics, the balance of payments of a country is the difference between all money flowing into the country in a particular period of time and the outflow of money to the rest of the world. In other words, it is economic transactions between countries during a period of time. These financial transactions are made by individuals, firms and government bodies to compare receipts and payments arising out of trade of goods and services.

The Bretton Woods system of monetary management established the rules for commercial relations among the United States, Canada, Western European countries, and Australia among 44 other countries after the 1944 Bretton Woods Agreement. The Bretton Woods system was the first example of a fully negotiated monetary order intended to govern monetary relations among independent states. The Bretton Woods system required countries to guarantee convertibility of their currencies into U.S. dollars to within 1% of fixed parity rates, with the dollar convertible to gold bullion for foreign governments and central banks at US$35 per troy ounce of fine gold. It also envisioned greater cooperation among countries in order to prevent future competitive devaluations, and thus established the International Monetary Fund (IMF) to monitor exchange rates and lend reserve currencies to nations with balance of payments deficits.

The causes of the Great Depression in the early 20th century in the United States have been extensively discussed by economists and remain a matter of active debate. They are part of the larger debate about economic crises and recessions. The specific economic events that took place during the Great Depression are well established.

The impossible trinity is a concept in international economics and international political economy which states that it is impossible to have all three of the following at the same time:

In macroeconomics and economic policy, a floating exchange rate is a type of exchange rate regime in which a currency's value is allowed to fluctuate in response to foreign exchange market events. A currency that uses a floating exchange rate is known as a floating currency, in contrast to a fixed currency, the value of which is instead specified in terms of material goods, another currency, or a set of currencies.

The Nixon shock was a series of economic measures undertaken by United States President Richard Nixon in 1971, in response to increasing inflation, the most significant of which were wage and price freezes, surcharges on imports, and the unilateral cancellation of the direct international convertibility of the United States dollar to gold.

Barry Julian Eichengreen is an American economist and economic historian who holds the title of George C. Pardee and Helen N. Pardee Professor of Economics and Political Science at the University of California, Berkeley, where he has taught since 1987. Eichengreen currently serves as a research associate at the National Bureau of Economic Research and as a Research Fellow at the Centre for Economic Policy Research.

Monetary hegemony is an economic and political concept in which a single state has decisive influence over the functions of the international monetary system. A monetary hegemon would need:

David Ernest William Laidler is an English/Canadian economist who has been one of the foremost scholars of monetarism. He published major economics journal articles on the topic in the late 1960s and early 1970s. His book, The Demand for Money, was published in four editions from 1969 through 1993, initially setting forth the stability of the relationship between income and the demand for money and later taking into consideration the effects of legal, technological, and institutional changes on the demand for money. The book has been translated into French, Spanish, Italian, Japanese, and Chinese.

A Monetary History of the United States, 1867–1960 is a book written in 1963 by Nobel Prize–winning economist Milton Friedman and Anna J. Schwartz. It uses historical time series and economic analysis to argue the then-novel proposition that changes in the money supply profoundly influenced the U.S. economy, especially the behavior of economic fluctuations. The implication they draw is that changes in the money supply had unintended adverse effects, and that sound monetary policy is necessary for economic stability. Orthodox economic historians see it as one of the most influential economics books of the century. The chapter dealing with the causes of the Great Depression was published as a stand-alone book titled The Great Contraction, 1929–1933.

Malcolm D. Knight is a Canadian economist, policymaker and banker. He is currently Visiting Professor of Finance at the London School of Economics and Political Science and a Distinguished Fellow at the Center for International Governance Innovation. From 2008 to 2012, Knight was Vice Chairman of Deutsche Bank Group where he was responsible for developing and coordinating the bank's global approach to issues in financial regulation, supervision, and financial stability. He served as general manager of the Bank for International Settlements from 2003 to 2008 and as Senior Deputy Governor of the Bank of Canada (1999-2003), after holding senior positions at the International Monetary Fund (1975-1999).

The following outline is provided as an overview of and topical guide to economics:

The term exorbitant privilege refers to the benefits the United States has due to its own currency being the international reserve currency. For example, the US would not face a balance of payments crisis, because their imports are purchased in their own currency. Exorbitant privilege as a concept cannot refer to currencies that have a regional reserve currency role, only to global reserve currencies.

A fixed exchange rate, often called a pegged exchange rate, is a type of exchange rate regime in which a currency's value is fixed or pegged by a monetary authority against the value of another currency, a basket of other currencies, or another measure of value, such as gold.

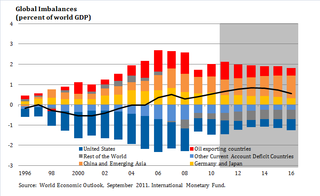

Global imbalances refers to the situation where some countries have more assets than the other countries. In theory, when the current account is in balance, it has a zero value: inflows and outflows of capital will be cancelled by each other. Hence, if the current account is persistently showing deficits for certain period, it is said to show an inequilibrium. Since, by definition, all current accounts and net foreign assets of the countries in the world must become zero, then other countries become indebted with the other nations. During recent years, global imbalances have become a concern in the rest of the world. The United States has run long term deficits, as well as many other advanced economies, while in Asia and emerging economies the opposite has occurred.

Michael David Bordo is a Canadian and American economist, currently Board of Governors Professor of Economics and Distinguished Professor of Economics at Rutgers University. He is a research associate at the National Bureau of Economic Research as well as a Distinguished Visiting Fellow at the Hoover Institution at Stanford University. He is the third most influential economic historian worldwide according to the RePEc/IDEAS rankings. He was a student of Milton Friedman and has co-authored numerous books and articles with Anna Schwartz.