See also

- Insurance

- Risk management

- Third party administrator

- Self-funded health care

- List of insurance topics

| Types of insurance |

| ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Insurance policy and law | |||||||||||||

| Insurance by country | |||||||||||||

| History | |||||||||||||

| Authority control databases: National |

|---|

Self-insurance is a situation in which a person or business that is liable for some risk does not take out any third-party insurance, but rather chooses to bear the risk itself.

In the United States the concept applies especially to self-funded health care and may involve, for example, an employer providing certain benefits – generally health benefits or disability benefits – to employees and funding claims from a specified pool of assets rather than through an insurance company, as the term is traditionally used. In self-funded health care, the employer ultimately retains the full risk of paying claims, in contrast to traditional insurance, where all risk is transferred to the insurer.

| Authority control databases: National |

|---|

Insurance is a means of protection from financial loss in which, in exchange for a fee, a party agrees to compensate another party in the event of a certain loss, damage, or injury. It is a form of risk management, primarily used to protect against the risk of a contingent or uncertain loss.

In the United States, a health maintenance organization (HMO) is a medical insurance group that provides health services for a fixed annual fee. It is an organization that provides or arranges managed care for health insurance, self-funded health care benefit plans, individuals, and other entities, acting as a liaison with health care providers on a prepaid basis. The Health Maintenance Organization Act of 1973 required employers with 25 or more employees to offer federally certified HMO options if the employer offers traditional healthcare options. Unlike traditional indemnity insurance, an HMO covers care rendered by those doctors and other professionals who have agreed by contract to treat patients in accordance with the HMO's guidelines and restrictions in exchange for a steady stream of customers. HMOs cover emergency care regardless of the health care provider's contracted status.

Actuarial science is the discipline that applies mathematical and statistical methods to assess risk in insurance, pension, finance, investment and other industries and professions. More generally, actuaries apply rigorous mathematics to model matters of uncertainty and life expectancy.

Health insurance or medical insurance is a type of insurance that covers the whole or a part of the risk of a person incurring medical expenses. As with other types of insurance, risk is shared among many individuals. By estimating the overall risk of health risk and health system expenses over the risk pool, an insurer can develop a routine finance structure, such as a monthly premium or payroll tax, to provide the money to pay for the health care benefits specified in the insurance agreement. The benefit is administered by a central organization, such as a government agency, private business, or not-for-profit entity.

The Employee Retirement Income Security Act of 1974 (ERISA) is a U.S. federal tax and labor law that establishes minimum standards for pension plans in private industry. It contains rules on the federal income tax effects of transactions associated with employee benefit plans. ERISA was enacted to protect the interests of employee benefit plan participants and their beneficiaries by:

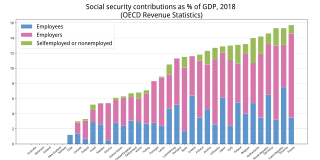

Social insurance is a form of social welfare that provides insurance against economic risks. The insurance may be provided publicly or through the subsidizing of private insurance. In contrast to other forms of social assistance, individuals' claims are partly dependent on their contributions, which can be considered insurance premiums to create a common fund out of which the individuals are then paid benefits in the future.

The term job lock is used to describe the inability of an employee to freely leave a job because doing so will result in the loss of employee benefits. In a broader sense, job lock may describe the situation where an employee is being paid higher than scale or has accumulated significant benefits, so that changing jobs is not a realistic option as it would result in significantly lower pay, less vacation time, etc.

Social welfare, assistance for the ill or otherwise disabled and the old, has long been provided in Japan by both the government and private companies. Beginning in the 1920s, the Japanese government enacted a series of welfare programs, based mainly on European models, to provide medical care and financial support. During the post-war period, a comprehensive system of social security was gradually established.

A Health Reimbursement Arrangement, also known as a Health Reimbursement Account (HRA), is a type of US employer-funded health benefit plan that reimburses employees for out-of-pocket medical expenses and, in limited cases, to pay for health insurance plan premiums.

National health insurance (NHI), sometimes called statutory health insurance (SHI), is a system of health insurance that insures a national population against the costs of health care. It may be administered by the public sector, the private sector, or a combination of both. Funding mechanisms vary with the particular program and country. National or statutory health insurance does not equate to government-run or government-financed health care, but is usually established by national legislation. In some countries, such as Australia's Medicare system, the UK's National Health Service and South Korea's National Health Insurance Service, contributions to the system are made via general taxation and therefore are not optional even though use of the health system it finances is. In practice, most people paying for NHI will join it. Where an NHI involves a choice of multiple insurance funds, the rates of contributions may vary and the person has to choose which insurance fund to belong to.

In the United States, a third-party administrator (TPA) is an organization that processes insurance claims or certain aspects of employee benefit plans for a separate entity. It is also a term used to define organizations within the insurance industry which administer other services such as underwriting and customer service. This can be viewed as outsourcing the administration of the claims processing, since the TPA is performing a task traditionally handled by the company providing the insurance or the company itself. Often, in the case of insurance claims, a TPA handles the claims processing for an employer that self-insures its employees. Thus, the employer is acting as an insurance company and underwrites the risk. The risk of loss remains with the employer, and not with the TPA. An insurance company may also use a TPA to manage its claims processing, provider networks, utilization review, or membership functions. While some third-party administrators may operate as units of insurance companies, they are often independent.

Self-funded health care, also known as Administrative Services Only (ASO), is a self insurance arrangement in the United States whereby an employer provides health or disability benefits to employees using the company's own funds. This is different from fully insured plans where the employer contracts an insurance company to cover the employees and dependents.

Aetna Health Inc. v. Davila, 542 U.S. 200 (2004), was a United States Supreme Court case in which the Court limited the scope of the Texas Healthcare Liability Act (THCLA). The effective result of this decision was that the THCLA, which held Case Management and Utilization Review decisions by Managed Care entities like CIGNA and Aetna to a legal duty of care according to the laws of The State of Texas could not be enforced in the case of Health Benefit plans provided through private employers, because the Texas statute allowed compensatory or punitive damages to redress losses or deter future transgressions, which were not available under ERISA § 1132. The ruling still allows the State of Texas to enforce the THCLA in the case of Government-sponsored (Medicare, Medicaid, Federal, State, Municipal Employee, etc., Church-sponsored, or Individual Health Plan Policies, which are saved from preemption by ERISA. The history that allows these Private and Self-Pay Insurance to be saved dates to the "Interstate Commerce" power that was given the federal Government by the Supreme Court. ERISA, enacted in 1974, relied on the "Interstate Commerce" rule to allow federal jurisdiction over private employers, based on the need of private employers to follow a single set of paperwork and rules for pensions and other employee benefit plans where employers had employees in multiple states. Except for private employer plans, insurance can be regulated by the individual states, and Managed Care entities making medical decisions can be held accountable for those decisions if negligence is involved, as allowed by the Texas Healthcare Liability Act.

In the United States, health insurance helps pay for medical expenses through privately purchased insurance, social insurance, or a social welfare program funded by the government. Synonyms for this usage include "health coverage", "health care coverage", and "health benefits". In a more technical sense, the term "health insurance" is used to describe any form of insurance providing protection against the costs of medical services. This usage includes both private insurance programs and social insurance programs such as Medicare, which pools resources and spreads the financial risk associated with major medical expenses across the entire population to protect everyone, as well as social welfare programs like Medicaid and the Children's Health Insurance Program, which both provide assistance to people who cannot afford health coverage.

Social security is divided by the French government into five branches: illness; old age/retirement; family; work accident; and occupational disease. From an institutional point of view, French social security is made up of diverse organismes. The system is divided into three main Regimes: the General Regime, the Farm Regime, and the Self-employed Regime. In addition there are numerous special regimes dating from prior to the creation of the state system in the mid-to-late 1940s.

Welfare in France includes all systems whose purpose is to protect people against the financial consequences of social risks.

The Virginia Workers' Compensation Commission (VWC) is an agency of the U.S. state of Virginia that oversees the resolution of workers' compensation claims brought in that state, in accordance with the Virginia Workers' Compensation Act. The Commission has exclusive jurisdiction to adjudicate such claims. Its decisions may be appealed to the Virginia Court of Appeals. The Commission is led by a Senior Leadership team consisting of three Commissioners, an Executive Director and a Chief Deputy Commissioner. The Commissioners are appointed by the Virginia General Assembly and serve staggered six-year terms. Honorable Robert A. Rapaport, Honorable Wesley G. Marshall and Honorable R. Ferrell Newman currently serve as Commissioners. The Commissioners elect a Chairman for a term of three years. Commissioner Rapaport currently serves as Chairman. Ms. Evelyn McGill is the Commission’s Executive Director and Honorable James J. Szablewicz is the Commission’s Chief Deputy Commissioner. The Commission is headquartered in Richmond, Virginia, and has offices and hearing locations at various places around the state.

The Empowering Patients First Act is legislation sponsored by Rep. Tom Price, first introduced as H.R. 3400 in the 111th Congress. The bill was initially intended to be a Republican alternative to the America's Affordable Health Choices Act of 2009, but has since been positioned as a potential replacement to the Patient Protection and Affordable Care Act (PPACA). The bill was introduced in the 112th Congress as H.R. 3000, and in the 113th Congress as H.R. 2300. As of October 2014, the bill has 58 cosponsors. An identical version of the bill has been introduced in the Senate by Senator John McCain as S. 1851.

Uninsured employer in the United States is a term to identify an employer of workers under circumstances where there is no form of insurance in place to provide certain benefits to those workers. More specifically, it is a term used in workers’ compensation law to identify an employer who does not have some form of worker's compensation insurance or self-insurance coverage in effect at the time of, or during the time of, a claimed injury.

PEHP Health & Benefits, known as Public Employees Health Program or simply PEHP, is a division of Utah Retirement Systems and administers Utah's public employees medical, dental, life, and long-term disability benefits. PEHP is governed through Title 49 of the Utah Code.