In economics, a shortage or excess demand is a situation in which the demand for a product or service exceeds its supply in a market. It is the opposite of an excess supply (surplus).

In economics, a shortage or excess demand is a situation in which the demand for a product or service exceeds its supply in a market. It is the opposite of an excess supply (surplus).

In a perfect market (one that matches a simple microeconomic model), an excess of demand will prompt sellers to increase prices until demand at that price matches the available supply, establishing market equilibrium. [1] [2] In economic terminology, a shortage occurs when for some reason (such as government intervention, or decisions by sellers not to raise prices) the price does not rise to reach equilibrium. In this circumstance, buyers want to purchase more at the market price than the quantity of the good or service that is available, and some non-price mechanism (such as "first come, first served" or a lottery) determines which buyers are served. So in a perfect market the only thing that can cause a shortage is price.

In common use, the term "shortage" may refer to a situation where most people are unable to find a desired good at an affordable price, especially where supply problems have increased the price. [3] "Market clearing" happens when all buyers and sellers willing to transact at the prevailing price are able to find partners. There are almost always willing buyers at a lower-than-market-clearing price; the narrower technical definition doesn't consider failure to serve this demand as a "shortage", even if it would be described that way in a social or political context (which the simple model of supply and demand does not attempt to encompass).

Shortages (in the technical sense) may be caused by the following causes:

Decisions which result in a below-market-clearing price help some people and hurt others. In this case, shortages may be accepted because they theoretically enable a certain portion of the population to purchase a product that they couldn't afford at the market-clearing price. The cost is to those who are willing to pay for a product and either can't, or experience greater difficulty in doing so.

In the case of government intervention in the market, there is always a trade-off with positive and negative effects. For example, a price ceiling may cause a shortage, but it will also enable a certain percentage of the population to purchase a product that they couldn't afford at market costs. [3] Economic shortages caused by higher transaction costs and opportunity costs (e.g., in the form of lost time) also mean that the distribution process is wasteful. Both of these factors contribute to a decrease in aggregate wealth.

Shortages may or will cause: [3]

Many regions around the world have experienced shortages in the past.

Garrett Hardin emphasised that a shortage of supply can just as well be viewed as a "longage" of demand. For instance, a shortage of food can just as well be called a longage of people (overpopulation). By looking at it from this view, he felt the problem could be better dealt with. [20]

In its narrowest definition, a labour shortage is an economic condition in which employers believe there are insufficient qualified candidates (employees) to fill the marketplace demands for employment at a wage that is mostly employer-determined. Such a condition is sometimes referred to by economists as "an insufficiency in the labour force." An ageing population and a contracting workforce and a birth dearth may curb U.S. economic expansion for several decades, for example. [21]

In a wider definition, a widespread domestic labour shortage is caused by excessively low salaries (relative to the domestic cost of living) and adverse working conditions (excessive workload and working hours) in low-wage industries (hospitality and leisure, education, health care, rail transportation, aviation, retail, manufacturing, food, elderly care), which collectively lead to occupational burnout and attrition of existing workers, insufficient incentives to attract the inflow supply of domestic workers, short-staffing at workplaces and further exacerbation (positive feedback) of staff shortages. [4]

Labour shortages occur broadly across multiple industries within a rapidly expanding economy, whilst labour shortages often occur within specific industries (which generally offer low salaries) even during economic periods of high unemployment. [22] In response to domestic labour shortages, business associations such as chambers of commerce would generally lobby to governments for an increase of the inward immigration of foreign workers from countries which are less developed and have lower salaries. [23] In addition, business associations have campaigned for greater state provision of child care, which would enable more women to re-enter the labour workforce. [24] However, as labour shortages in the relevant low-wage industries are often widespread globally throughout many countries in the world, immigration would only partially address the chronic labour shortages in the relevant low-wage industries in developed countries (whilst simultaneously discouraging local labour from entering the relevant industries) and in turn cause greater labour shortages in developing countries. [25]

The Atlantic slave trade (which originated in the early 17th century but ended by the early 19th century) was said to have originated from perceived shortages of agricultural labour in the Americas (particularly in the Southern United States). It was thought that bringing African labor was the only means of malaria resistance available at the time. [26] Ironically, malaria seems to itself have been introduced to the "New World" via the slave trade. [27]

Labour economics, or labor economics, seeks to understand the functioning and dynamics of the markets for wage labour. Labour is a commodity that is supplied by labourers, usually in exchange for a wage paid by demanding firms. Because these labourers exist as parts of a social, institutional, or political system, labour economics must also account for social, cultural and political variables.

In economics, stagflation or recession-inflation is a situation in which the inflation rate is high or increasing, the economic growth rate slows, and unemployment remains steadily high. It presents a dilemma for economic policy, since actions intended to lower inflation may exacerbate unemployment.

In microeconomics, supply and demand is an economic model of price determination in a market. It postulates that, holding all else equal, in a competitive market, the unit price for a particular good or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded will equal the quantity supplied, resulting in an economic equilibrium for price and quantity transacted. The concept of supply and demand forms the theoretical basis of modern economics.

In economics, economic equilibrium is a situation in which economic forces such as supply and demand are balanced and in the absence of external influences the values of economic variables will not change. For example, in the standard text perfect competition, equilibrium occurs at the point at which quantity demanded and quantity supplied are equal.

Rationing is the controlled distribution of scarce resources, goods, services, or an artificial restriction of demand. Rationing controls the size of the ration, which is one's allowed portion of the resources being distributed on a particular day or at a particular time. There are many forms of rationing, although rationing by price is most prevalent.

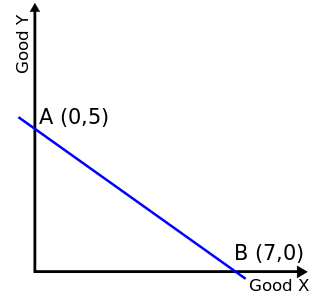

In economics, a budget constraint represents all the combinations of goods and services that a consumer may purchase given current prices within his or her given income. Consumer theory uses the concepts of a budget constraint and a preference map as tools to examine the parameters of consumer choices. Both concepts have a ready graphical representation in the two-good case. The consumer can only purchase as much as their income will allow, hence they are constrained by their budget. The equation of a budget constraint is where is the price of good X, and is the price of good Y, and m is income.

In classical economics, Say's law, or the law of markets, is the claim that the production of a product creates demand for another product by providing something of value which can be exchanged for that other product. So, production is the source of demand. In his principal work, A Treatise on Political Economy, Jean-Baptiste Say wrote: "A product is no sooner created, than it, from that instant, affords a market for other products to the full extent of its own value." And also, "As each of us can only purchase the productions of others with his/her own productions – as the value we can buy is equal to the value we can produce, the more men can produce, the more they will purchase."

In economics, effective demand (ED) in a market is the demand for a product or service which occurs when purchasers are constrained in a different market. It contrasts with notional demand, which is the demand that occurs when purchasers are not constrained in any other market. In the aggregated market for goods in general, demand, notional or effective, is referred to as aggregate demand. The concept of effective supply parallels the concept of effective demand. The concept of effective demand or supply becomes relevant when markets do not continuously maintain equilibrium prices.

Incomes policies in economics are economy-wide wage and price controls, most commonly instituted as a response to inflation, and usually seeking to establish wages and prices below free market level.

In economics, market clearing is the process by which, in an economic market, the supply of whatever is traded is equated to the demand so that there is no excess supply or demand, ensuring that there is neither a surplus nor a shortage. The new classical economics assumes that in any given market, assuming that all buyers and sellers have access to information and that there is no "friction" impeding price changes, prices constantly adjust up or down to ensure market clearing.

Price controls are restrictions set in place and enforced by governments, on the prices that can be charged for goods and services in a market. The intent behind implementing such controls can stem from the desire to maintain affordability of goods even during shortages, and to slow inflation, or, alternatively, to ensure a minimum income for providers of certain goods or to try to achieve a living wage. There are two primary forms of price control: a price ceiling, the maximum price that can be charged; and a price floor, the minimum price that can be charged. A well-known example of a price ceiling is rent control, which limits the increases that a landlord is permitted by government to charge for rent. A widely used price floor is minimum wage. Historically, price controls have often been imposed as part of a larger incomes policy package also employing wage controls and other regulatory elements.

A price floor is a government- or group-imposed price control or limit on how low a price can be charged for a product, good, commodity, or service. It is one type of price support; other types include supply regulation and guarantee government purchase price. A price floor must be higher than the equilibrium price in order to be effective. The equilibrium price, commonly called the "market price", is the price where economic forces such as supply and demand are balanced and in the absence of external influences the (equilibrium) values of economic variables will not change, often described as the point at which quantity demanded and quantity supplied are equal. Governments use price floors to keep certain prices from going too low.

"Shortage economy" is a term coined by Hungarian economist János Kornai, who used this term to criticize the old centrally-planned economies of the communist states of the Eastern Bloc.

János Kornai was a Hungarian economist noted for his analysis and criticism of the command economies of Eastern European communist states. He also covered macroeconomic aspects in countries undergoing post-Soviet transition. He was emeritus professor at both Harvard University and Corvinus University of Budapest. Kornai was known to have coined the term shortage economy to reflect perpetual shortages of goods in the centrally-planned command economies of the Eastern Bloc.

In economics, an excess supply, economic surplus market surplus or briefly supply is a situation in which the quantity of a good or service supplied is more than the quantity demanded, and the price is above the equilibrium level determined by supply and demand. That is, the quantity of the product that producers wish to sell exceeds the quantity that potential buyers are willing to buy at the prevailing price. It is the opposite of an economic shortage.

In economics, a factor market is a market where factors of production are bought and sold. Factor markets allocate factors of production, including land, labour and capital, and distribute income to the owners of productive resources, such as wages, rents, etc.

Jacques H. Drèze was a Belgian economist noted for his contributions to economic theory, econometrics, and economic policy as well as for his leadership in the economics profession. Drèze was the first President of the European Economic Association in 1986 and was the President of the Econometric Society in 1970.

Disequilibrium macroeconomics is a tradition of research centered on the role of disequilibrium in economics. This approach is also known as non-Walrasian theory, equilibrium with rationing, the non-market clearing approach, and non-tâtonnement theory. Early work in the area was done by Don Patinkin, Robert W. Clower, and Axel Leijonhufvud. Their work was formalized into general disequilibrium models, which were very influential in the 1970s. American economists had mostly abandoned these models by the late 1970s, but French economists continued work in the tradition and developed fixprice models.

When elected in 2013, Nicolás Maduro continued the majority of existing economic policies of his predecessor Hugo Chávez. When entering the presidency, President Maduro's Venezuela faced a high inflation rate and large shortages of goods that was left over from the previous policies of President Chávez. These economic difficulties that Venezuela was facing were one of the main reasons of the current protests in Venezuela. President Maduro has blamed capitalism for speculation that is driving high rates of inflation and creating widespread shortages of staples, and often said he was fighting an "economic war", calling newly enacted economic measures "economic offensives" against political opponents he and loyalists state are behind an international economic conspiracy. However, President Maduro has been criticized for only concentrating on public opinion instead of tending to the practical issues economists have warned the Venezuelan government about or creating any ideas to improve the economic situation in Venezuela such as the "economic war".

This glossary of economics is a list of definitions of terms and concepts used in economics, its sub-disciplines, and related fields.

The Great Depression of the 1930s hit Mexican immigrants especially hard. Along with the job crisis and food shortages that affected all U.S. workers, Mexicans and Mexican Americans had to face an additional threat: deportation.

| Major topics | |

|---|---|

| Society and population | |

| Publications | |

| Lists | |

Events and organizations |

|

| Related topics | |