Related Research Articles

The United States has separate federal, state, and local governments with taxes imposed at each of these levels. Taxes are levied on income, payroll, property, sales, capital gains, dividends, imports, estates and gifts, as well as various fees. In 2020, taxes collected by federal, state, and local governments amounted to 25.5% of GDP, below the OECD average of 33.5% of GDP.

A flat tax is a tax with a single rate on the taxable amount, after accounting for any deductions or exemptions from the tax base. It is not necessarily a fully proportional tax. Implementations are often progressive due to exemptions, or regressive in case of a maximum taxable amount. There are various tax systems that are labeled "flat tax" even though they are significantly different. The defining characteristic is the existence of only one tax rate other than zero, as opposed to multiple non-zero rates that vary depending on the amount subject to taxation.

An income tax is a tax imposed on individuals or entities (taxpayers) in respect of the income or profits earned by them. Income tax generally is computed as the product of a tax rate times the taxable income. Taxation rates may vary by type or characteristics of the taxpayer and the type of income.

The Tax Reform Act of 1986 (TRA) was passed by the 99th United States Congress and signed into law by President Ronald Reagan on October 22, 1986.

A tax deduction or benefit is an amount deducted from taxable income, usually based on expenses such as those incurred to produce additional income. Tax deductions are a form of tax incentives, along with exemptions and tax credits. The difference between deductions, exemptions, and credits is that deductions and exemptions both reduce taxable income, while credits reduce tax.

In addition to federal income tax collected by the United States, most individual U.S. states collect a state income tax. Some local governments also impose an income tax, often based on state income tax calculations. Forty-one states, the District of Columbia, and many localities in the United States impose an income tax on individuals. Eight states impose no state income tax, and a ninth, New Hampshire, imposes an individual income tax on dividends and interest income but not other forms of income. Forty-seven states and many localities impose a tax on the income of corporations.

The Tax Reform Act of 1969 was a United States federal tax law signed by President Richard Nixon in 1969. Its largest impact was creating the Alternative Minimum Tax, which was intended to tax high-income earners who had previously avoided incurring tax liability due to various exemptions and deductions.

The Internal Revenue Code of 1986 (IRC), is the domestic portion of federal statutory tax law in the United States. It is codified in statute as Title 26 of the United States Code. The IRC is organized topically into subtitles and sections, covering federal income tax in the United States, payroll taxes, estate taxes, gift taxes, and excise taxes; as well as procedure and administration. The Code's implementing federal agency is the Internal Revenue Service.

An S corporation, for United States federal income tax, is a closely held corporation that makes a valid election to be taxed under Subchapter S of Chapter 1 of the Internal Revenue Code. In general, S corporations do not pay any income taxes. Instead, the corporation's income and losses are divided among and passed through to its shareholders. The shareholders must then report the income or loss on their own individual income tax returns.

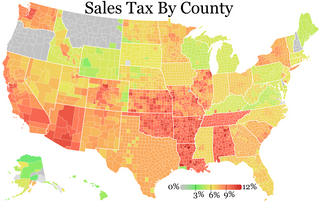

Sales taxes in the United States are taxes placed on the sale or lease of goods and services in the United States. Sales tax is governed at the state level and no national general sales tax exists. 45 states, the District of Columbia, the territories of Puerto Rico, and Guam impose general sales taxes that apply to the sale or lease of most goods and some services, and states also may levy selective sales taxes on the sale or lease of particular goods or services. States may grant local governments the authority to impose additional general or selective sales taxes.

The United States federal government and most state governments impose an income tax. They are determined by applying a tax rate, which may increase as income increases, to taxable income, which is the total income less allowable deductions. Income is broadly defined. Individuals and corporations are directly taxable, and estates and trusts may be taxable on undistributed income. Partnerships are not taxed, but their partners are taxed on their shares of partnership income. Residents and citizens are taxed on worldwide income, while nonresidents are taxed only on income within the jurisdiction. Several types of credits reduce tax, and some types of credits may exceed tax before credits. Most business expenses are deductible. Individuals may deduct certain personal expenses, including home mortgage interest, state taxes, contributions to charity, and some other items. Some deductions are subject to limits, and an Alternative Minimum Tax (AMT) applies at the federal and some state levels.

Under Article 108 of the Basic Law of Hong Kong, the taxation system in Hong Kong is independent of, and different from, the taxation system in mainland China. In addition, under Article 106 of the Hong Kong Basic Law, Hong Kong has independent public finance, and no tax revenue is handed over to the Central Government in China. The taxation system in Hong Kong is generally considered to be one of the simplest, most transparent and straightforward systems in the world. Taxes are collected through the Inland Revenue Department (IRD).

A gross receipts tax or gross excise tax is a tax on the total gross revenues of a company, regardless of their source. A gross receipts tax is often compared to a sales tax; the difference is that a gross receipts tax is levied upon the seller of goods or services, while a sales tax is nominally levied upon the buyer. This is compared to other taxes listed as separate line items on billings, are not directly included in the listed price of the item, and are not a factor in markup or profit on company sales. A gross receipts tax has a pyramid effect that increases the actual taxable percentage as it passes through the product or service lifecycle.

Corporate tax is imposed in the United States at the federal, most state, and some local levels on the income of entities treated for tax purposes as corporations. Since January 1, 2018, the nominal federal corporate tax rate in the United States of America is a flat 21% following the passage of the Tax Cuts and Jobs Act of 2017. State and local taxes and rules vary by jurisdiction, though many are based on federal concepts and definitions. Taxable income may differ from book income both as to timing of income and tax deductions and as to what is taxable. The corporate Alternative Minimum Tax was also eliminated by the 2017 reform, but some states have alternative taxes. Like individuals, corporations must file tax returns every year. They must make quarterly estimated tax payments. Groups of corporations controlled by the same owners may file a consolidated return.

Under the United States taxation system, an enterprise may deduct business expenses from its taxable income, subject to certain conditions. On occasion the Internal Revenue Service (IRS) has challenged such deductions, regarding the activities in question as illegitimate, and in certain circumstances the Internal Revenue Code provides for such challenge. Rulings by the U.S. Supreme Court have in general upheld the deductions, where there is not a specific governmental policy in support of disallowing them.

Qualified Production Activities Income is a class of income which is entitled to favored tax treatment under Section 199 of the United States Internal Revenue Code.

Taxes in Indiana are almost entirely authorized at the state level, although the revenue is used to fund both local and state level government. The state of Indiana's income comes from four primary tax areas. Most state level income is from a sales tax of 7% and a flat state income tax of 3.05%. The state also collects an additional income tax for the 92 counties. Local governments are funded by a property tax that is the sum of rates set by local boards, but the total rate must be approved by the Indiana General Assembly before it can be imposed. Residential property tax rates are capped at maximum of 1% of property value. Excise tax is the fourth form of taxation and is charged on motor vehicles, alcohol, tobacco, gasoline, and certain other forms of movable property; most of the proceeds are used to fund state and local roads and health programs. The Indiana Department of Revenue collects all taxes and pays them out to the appropriate agencies and municipalities. The Indiana Tax Court deals with all tax disputes issues, but decisions can be appealed to the Indiana Supreme Court.

The alternative minimum tax (AMT) is a tax imposed by the United States federal government in addition to the regular income tax for certain individuals, estates, and trusts. As of tax year 2018, the AMT raises about $5.2 billion, or 0.4% of all federal income tax revenue, affecting 0.1% of taxpayers, mostly in the upper income ranges.

The policy of taxation in the Philippines is governed chiefly by the Constitution of the Philippines and three Republic Acts.

Taxation in New Mexico comprises the taxation programs of the U.S state of New Mexico. All taxes are administered on state- and city-levels by the New Mexico Taxation and Revenue Department, a state agency. The principal taxes levied include state income tax, a state gross receipts tax, gross receipts taxes in local jurisdictions, state and local property taxes, and several taxes related to production and processing of oil, gas, and other natural resources.

References

- 1 2 3 "Business & Occupation Tax: RCW 82.04" (PDF). Washington Department of Revenue. 2007. Archived from the original (PDF) on 2009-05-12. Retrieved 2009-04-19.

- ↑ Occupational Tax Districts, Kentucky Secretary of State

- ↑ Tax classifications for common businesses

- ↑ Definitions of tax classifications for the B & O tax

- ↑ RCW 82.04.4284: Deduction - Bad debts

- ↑ WAC 458-20-196: Bad debts

- ↑ "Business Costs – Taxes". Business Assistance. West Virginia Development Office. Retrieved 2009-04-19.

- 1 2 "Publication TSD-100: West Virginia Business Taxes" (PDF). West Virginia State Tax Department. November 2008. Archived from the original (PDF) on 2007-02-08. Retrieved 2009-04-19.

- ↑ "B&O Tax Calculator". The City of Parkersburg, West Virginia. Archived from the original on May 22, 2008. Retrieved 2009-04-19.