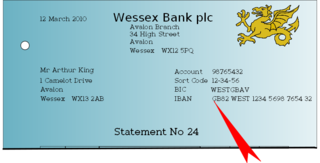

The International Bank Account Number (IBAN) is an internationally agreed system of identifying bank accounts across national borders to facilitate the communication and processing of cross border transactions with a reduced risk of transcription errors. An IBAN uniquely identifies the account of a customer at a financial institution. It was originally adopted by the European Committee for Banking Standards (ECBS) and later as an international standard under ISO 13616:1997. The current standard is ISO 13616:2020, which indicates SWIFT as the formal registrar. Initially developed to facilitate payments within the European Union, it has been implemented by most European countries and numerous countries in other parts of the world, mainly in the Middle East and the Caribbean. As of May 2020, 77 countries were using the IBAN numbering system.

The Society for Worldwide Interbank Financial Telecommunication (SWIFT), legally S.W.I.F.T. SCRL, is a Belgian cooperative society that serves as an intermediary and executor of financial transactions between banks worldwide. It also sells software and services to financial institutions, mostly for use on its proprietary "SWIFTNet", and ISO 9362 Business Identifier Codes (BICs), popularly known as "SWIFT codes". Swift Transfer is also called International Money Transfer.

ISO 9362 defines a standard format of Business Identifier Codes approved by the International Organization for Standardization (ISO). It is a unique identification code for both financial and non-financial institutions. The acronym SWIFT stands for the Society for Worldwide Interbank Financial Telecommunication. The ISO has designated SWIFT as the BIC registration authority. When assigned to a non-financial institution, the code may also be known as a Business Entity Identifier or BEI. These codes are used when transferring money between banks, particularly for international wire transfers, and also for the exchange of other messages between banks. The codes can sometimes be found on account statements.

Delivery versus payment or DvP is a common form of settlement for securities. The process involves the simultaneous delivery of all documents necessary to give effect to a transfer of securities in exchange for the receipt of the stipulated payment amount. Alternatively, it may involve transfers of two securities in such a way as to ensure that delivery of one security occurs if and only if the corresponding delivery of the other security occurs.

ISO 15022 is an ISO standard for messaging used in transactions between financial institutions. Participants in the financial industry need a common representation of the financial transactions they perform and this standard defines general message schema, which in turn are used by organizations to define messages in a complete and unambiguous way. This results in efficiency, lower costs, and the avoidance of errors. Prior to standardization in this area, there were overlapping standards, or ad hoc approaches where there was a functional gap and no standard.

The Australian financial system consists of the arrangements covering the borrowing and lending of funds and the transfer of ownership of financial claims in Australia, comprising:

ISO 20022 is an ISO standard for electronic data interchange between financial institutions. It describes a metadata repository containing descriptions of messages and business processes, and a maintenance process for the repository content. The standard covers financial information transferred between financial institutions that includes payment transactions, securities trading and settlement information, credit and debit card transactions and other financial information.

In banking and finance, clearing denotes all activities from the time a commitment is made for a transaction until it is settled. This process turns the promise of payment into the actual movement of money from one account to another. Clearing houses were formed to facilitate such transactions among banks.

A payment system is any system used to settle financial transactions through the transfer of monetary value. This includes the institutions, instruments, people, rules, procedures, standards, and technologies that make its exchange possible. A common type of payment system, called an operational network, links bank accounts and provides for monetary exchange using bank deposits. Some payment systems also include credit mechanisms, which are essentially a different aspect of payment.

Electronic funds transfer (EFT) is the electronic transfer of money from one bank account to another, either within a single financial institution or across multiple institutions, via computer-based systems, without the direct intervention of bank staff.

The Clearing House Interbank Payments System (CHIPS) is a United States private clearing house for large-value transactions. By 2015, it was settling well over US$1.5 trillion a day in around 250,000 interbank payments in cross border and domestic transactions. Together with the Fedwire Funds Service, CHIPS forms the primary U.S. network for large-value domestic and international USD payments where it has a market share of around 96%. CHIPS transfers are governed by Article 4A of Uniform Commercial Code.

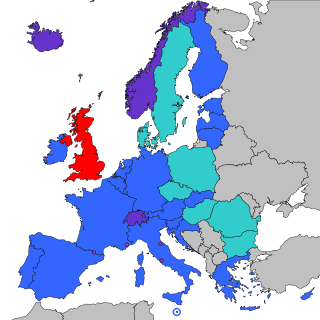

The Single Euro Payments Area (SEPA) is a payment-integration initiative of the European Union for simplification of bank transfers denominated in euro. As of 2020, there were 36 members in SEPA, consisting of the 27 member states of the European Union, the four member states of the European Free Trade Association, and the United Kingdom. Some countries participate in the technical schemes: Andorra, Monaco, San Marino, and Vatican City.

SWIFT message types are the format or schema used to send messages to financial institutions on the SWIFT network. The original message types were developed by SWIFT and a subset was retrospectively made into an ISO standard, ISO 15022. In many instances, SWIFT message types between custodians follow the ISO standard. This was later supplemented by a XML based version under ISO 20022.

The Clearing House Automated Transfer System, or CHATS, is a real-time gross settlement (RTGS) system for the transfer of funds in Hong Kong. It is operated by Hong Kong Interbank Clearing Limited, a private company jointly owned by the Hong Kong Monetary Authority (HKMA) and the Hong Kong Association of Banks. Transactions in four currency denominations may be settled using CHATS: Hong Kong dollar, renminbi, euro, and US dollar. In 2005, the value of Hong Kong dollar CHATS transactions averaged HK$467 billion per day, which amounted to a third of Hong Kong's annual Gross Domestic Product (GDP); the total value of transactions that year was 84 times the GDP of Hong Kong.

The Electronic Banking Internet Communication Standard (EBICS) is a German transmission protocol developed by the German Banking Industry Committee for sending payment information between banks over the Internet. It grew out of the earlier BCS-FTAM protocol that was developed in 1995, with the aim of being able to use internet connections and TCP/IP. It is mandated for use by German banks and has also been adopted by France and Switzerland.

MT103 is a Society for Worldwide Interbank Financial Telecommunication (SWIFT) payment message type/format used by financial institutions for customer cash transfers specifically for cross border/international wire transfer.

The Swiss Interbank Clearing (SIC) system is a mechanism for the clearing of domestic and international payments.

Since the late-2000s, the People's Republic of China (PRC) has sought to internationalize its official currency, the Renminbi (RMB). RMB internationalization accelerated in 2009 when China established the dim sum bond market and expanded Cross-Border Trade RMB Settlement Pilot Project, which helps establish pools of offshore RMB liquidity. The RMB was the 8th-most-traded currency in the world in 2013 and the 7th-most-traded in early 2014. By the end of 2014, RMB ranked 5th as the most traded currency, according to SWIFT's report, at 2.2% of SWIFT payment behind JPY (2.7%), GBP (7.9%), EUR (28.3%) and USD (44.6%). In February 2015, RMB became the second most used currency for trade and services, and reached the ninth position in forex trading. The RMB Qualified Foreign Institutional Investor (RQFII) quotas were also extended to five other countries — the UK, Singapore, France, Korea, Germany, and Canada, each with the quotas of ¥80 billion except Canada and Singapore (¥50bn). Previously, only Hong Kong was allowed, with a ¥270 billion quota.

The International Payments Framework (IPF) was an initiative launched in 2010 to create a global framework for payment processing by the International Payments Framework Association, a trade association headquartered in Atlanta, in the United States. The IPF standard is currently used by some organisations to process payments between the United States and Europe.

SPFS is a Russian equivalent of the SWIFT financial transfer system, developed by the Central Bank of Russia. The system has been in development since 2014, after the United States government threatened to disconnect Russia from the SWIFT system.