Related Research Articles

The Federal Deposit Insurance Corporation (FDIC) is a United States government corporation supplying deposit insurance to depositors in American commercial banks and savings banks. The FDIC was created by the Banking Act of 1933, enacted during the Great Depression to restore trust in the American banking system. More than one-third of banks failed in the years before the FDIC's creation, and bank runs were common. The insurance limit was initially US$2,500 per ownership category, and this has been increased several times over the years. Since the enactment of the Dodd–Frank Wall Street Reform and Consumer Protection Act in 2010, the FDIC insures deposits in member banks up to $250,000 per ownership category. FDIC insurance is backed by the full faith and credit of the government of the United States, and according to the FDIC, "since its start in 1933 no depositor has ever lost a penny of FDIC-insured funds".

A commercial bank is a financial institution which accepts deposits from the public and gives loans for the purposes of consumption and investment to make profit.

An offshore bank is a bank that is operated and regulated under international banking license, which usually prohibits the bank from establishing any business activities in the jurisdiction of establishment. Due to less regulation and transparency, accounts with offshore banks were often used to hide undeclared income. Since the 1980s, jurisdictions that provide financial services to nonresidents on a big scale can be referred to as offshore financial centres. OFCs often also levy little or no corporation tax and/or personal income and high direct taxes such as duty, making the cost of living high.

Bank fraud is the use of potentially illegal means to obtain money, assets, or other property owned or held by a financial institution, or to obtain money from depositors by fraudulently posing as a bank or other financial institution. In many instances, bank fraud is a criminal offence. While the specific elements of particular banking fraud laws vary depending on jurisdictions, the term bank fraud applies to actions that employ a scheme or artifice, as opposed to bank robbery or theft. For this reason, bank fraud is sometimes considered a white-collar crime.

A savings and loan association (S&L), or thrift institution, is a financial institution that specializes in accepting savings deposits and making mortgage and other loans. The terms "S&L" and "thrift" are mainly used in the United States; similar institutions in the United Kingdom, Ireland and some Commonwealth countries include building societies and trustee savings banks. They are often mutually held, meaning that the depositors and borrowers are members with voting rights, and have the ability to direct the financial and managerial goals of the organization like the members of a credit union or the policyholders of a mutual insurance company. While it is possible for an S&L to be a joint-stock company, and even publicly traded, in such instances it is no longer truly a mutual association, and depositors and borrowers no longer have membership rights and managerial control. By law, thrifts can have no more than 20 percent of their lending in commercial loans—their focus on mortgage and consumer loans makes them particularly vulnerable to housing downturns such as the deep one the U.S. experienced in 2007.

A money market fund is an open-ended mutual fund that invests in short-term debt securities such as US Treasury bills and commercial paper. Money market funds are managed with the goal of maintaining a highly stable asset value through liquid investments, while paying income to investors in the form of dividends. Although they are not insured against loss, actual losses have been quite rare in practice.

The Bank of Korea is the central bank of the Republic of Korea and issuer of Korean Republic won. It was established on 12 June 1950 in Seoul, South Korea.

The Australian financial system consists of the arrangements covering the borrowing and lending of funds and the transfer of ownership of financial claims in Australia, comprising:

The Canada Deposit Insurance Corporation is a Canadian federal Crown Corporation created by Parliament in 1967 to provide deposit insurance to depositors in Canadian commercial banks and savings institutions. CDIC insures Canadians' deposits held at Canadian banks up to C$100,000 in case of a bank failure. CDIC automatically insures many types of savings against the failure of a financial institution. However, the bank must be a CDIC member and not all savings are insured. CDIC is also Canada's resolution authority for banks, federally regulated credit unions, trust and loan companies as well as associations governed by the Cooperative Credit Associations Act that take deposits.

Deposit insurance or deposit protection is a measure implemented in many countries to protect bank depositors, in full or in part, from losses caused by a bank's inability to pay its debts when due. Deposit insurance systems are one component of a financial system safety net that promotes financial stability.

Bank account debits tax was an Australian bank transaction tax levied on customer withdrawals from bank accounts with a cheque facility.

Taxes in New Zealand are collected at a national level by the Inland Revenue Department (IRD) on behalf of the Government of New Zealand. National taxes are levied on personal and business income, and on the supply of goods and services. Capital gains tax applies in limited situations, such as the sale of some rental properties within 10 years of purchase. Some "gains" such as profits on the sale of patent rights are deemed to be income – income tax does apply to property transactions in certain circumstances, particularly speculation. There are currently no land taxes, but local property taxes (rates) are managed and collected by local authorities. Some goods and services carry a specific tax, referred to as an excise or a duty, such as alcohol excise or gaming duty. These are collected by a range of government agencies such as the New Zealand Customs Service. There is no social security (payroll) tax.

The budget of the European Union is used to finance EU funding programmes and other expenditure at the European level.

Income taxes are the most significant form of taxation in Australia, and collected by the federal government through the Australian Taxation Office. Australian GST revenue is collected by the Federal government, and then paid to the states under a distribution formula determined by the Commonwealth Grants Commission.

Taxation in the British Virgin Islands is relatively simple by comparative standards; photocopies of all of the tax laws of the British Virgin Islands (BVI) would together amount to about 200 pages of paper.

A bank is a financial institution that accepts deposits from the public and creates a demand deposit while simultaneously making loans. Lending activities can be directly performed by the bank or indirectly through capital markets.

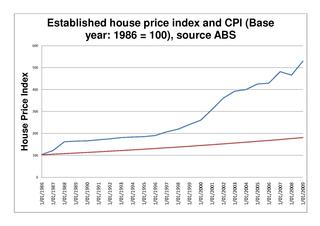

The Australian property bubble is the economic theory that the Australian property market has become or is becoming significantly overpriced and due for a significant downturn. Since the early 2010s, various commentators, including one Treasury official, have claimed the Australian property market is in a significant bubble.

A bank tax, or a bank levy, is a tax on banks which was discussed in the context of the financial crisis of 2007–08. The bank tax is levied on the capital at risk of financial institutions, excluding federally insured deposits, with the aim of discouraging banks from taking unnecessary risks. The bank tax is levied on a limited number of sophisticated taxpayers and is not especially difficult to understand. It can be used as a counterbalance to the various ways in which banks are currently subsidized by the tax system, such as the ability to subtract bad loan reserves, delay tax on interest received abroad, and buy other banks and use their losses to offset future income. In other words, the bank tax is a small reimbursement of taxpayer funds used to bail out major banks after the 2008 financial crisis, and it is carefully structured to target only certain institutions that are considered "too big to fail."

A fixed deposit (FD) is a tenured deposit account provided by banks or non-bank financial institutions which provides investors a higher rate of interest than a regular savings account, until the given maturity date. It may or may not require the creation of a separate account. The term fixed deposit is most commonly used in India and the United States. It is known as a term deposit or time deposit in Canada, Australia, New Zealand, and as a bond in the United Kingdom.

The Ministry of Finance, abbreviated MOF, is a ministry of the Government of Malaysia that is charged with the responsibility for government expenditure and revenue raising. The ministry's role is to develop economic policy and prepare the Malaysian federal budget. The Ministry of Finance also oversees financial legislation and regulation. Each year in October, the Minister of Finance presents the Malaysian federal budget to the Parliament.

References

- ↑ Australian Bankers' Association. "Press release on FID abolition". Archived from the original on 22 December 2004.

- ↑ "NT legislation". September 2013.[ dead link ]

- Bank Account Transaction Taxes: 'FID' and 'BAD' , David Kehl, Parliament of Australia Parliamentary Library Research Note 7 2001–02