The European debt crisis, often also referred to as the eurozone crisis or the European sovereign debt crisis, was a multi-year debt crisis that took place in the European Union (EU) from 2009 until the mid to late 2010s. Several eurozone member states were unable to repay or refinance their government debt or to bail out over-indebted banks under their national supervision without the assistance of third parties like other eurozone countries, the European Central Bank (ECB), or the International Monetary Fund (IMF).

Greece faced a sovereign debt crisis in the aftermath of the financial crisis of 2007–2008. Widely known in the country as The Crisis, it reached the populace as a series of sudden reforms and austerity measures that led to impoverishment and loss of income and property, as well as a small-scale humanitarian crisis. In all, the Greek economy suffered the longest recession of any advanced mixed economy to date. As a result, the Greek political system has been upended, social exclusion increased, and hundreds of thousands of well-educated Greeks have left the country.

The European Financial Stability Facility (EFSF) is a special purpose vehicle financed by members of the eurozone to address the European sovereign-debt crisis. It was agreed by the Council of the European Union on 9 May 2010, with the objective of preserving financial stability in Europe by providing financial assistance to eurozone states in economic difficulty. The Facility's headquarters are in Luxembourg City, as are those of the European Stability Mechanism. Treasury management services and administrative support are provided to the Facility by the European Investment Bank through a service level contract. Since the establishment of the European Stability Mechanism, the activities of the EFSF are carried out by the ESM.

From late 2009, fears of a sovereign debt crisis in some European states developed, with the situation becoming particularly tense in early 2010. Greece was most acutely affected, but fellow Eurozone members Cyprus, Ireland, Italy, Portugal, and Spain were also significantly affected. In the EU, especially in countries where sovereign debt has increased sharply due to bank bailouts, a crisis of confidence has emerged with the widening of bond yield spreads and risk insurance on credit default swaps between these countries and other EU members, most importantly Germany.

The European Financial Stabilisation Mechanism (EFSM) is an emergency funding programme reliant upon funds raised on the financial markets and guaranteed by the European Commission using the budget of the European Union as collateral. It runs under the supervision of the Commission and aims at preserving financial stability in Europe by providing financial assistance to member states of the European Union in economic difficulty.

The European Stability Mechanism (ESM) is an intergovernmental organization located in Luxembourg City, which operates under public international law for all eurozone member states having ratified a special ESM intergovernmental treaty. It was established on 27 September 2012 as a permanent firewall for the eurozone, to safeguard and provide instant access to financial assistance programmes for member states of the eurozone in financial difficulty, with a maximum lending capacity of €500 billion. It has replaced two earlier temporary EU funding programmes: the European Financial Stability Facility (EFSF) and the European Financial Stabilisation Mechanism (EFSM).

Legislative elections were held in Greece on Sunday 25 January 2015 to elect all 300 members to the Hellenic Parliament in accordance with the constitution. The election was held earlier than scheduled due to the failure of the Greek parliament to elect a new president on 29 December 2014.

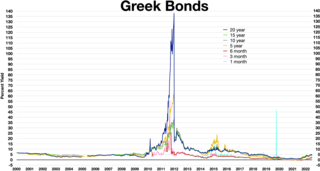

The Greek government-debt crisis is one of a number of current European sovereign-debt crises. In late 2009, fears of a sovereign debt crisis developed among investors concerning Greece's ability to meet its debt obligations because of strong increase in government debt levels. This led to a crisis of confidence, indicated by a widening of bond yield spreads and the cost of risk insurance on credit default swaps compared to the other countries in the Eurozone, most importantly Germany.

The 2012–2013 Cypriot financial crisis was an economic crisis in the Republic of Cyprus that involved the exposure of Cypriot banks to overleveraged local property companies, the Greek government-debt crisis, the downgrading of the Cypriot government's bond credit rating to junk status by international credit rating agencies, the consequential inability to refund its state expenses from the international markets and the reluctance of the government to restructure the troubled Cypriot financial sector.

The eurozone crisis is an ongoing financial crisis that has made it difficult or impossible for some countries in the euro area to repay or re-finance their government debt without the assistance of third parties.

The Second Economic Adjustment Programme for Greece, usually referred to as the second bailout package or the second memorandum, is a memorandum of understanding on financial assistance to the Hellenic Republic in order to cope with the Greek government-debt crisis.

The Third Economic Adjustment Programme for Greece, usually referred to as the third bailout package or the third memorandum, is a memorandum of understanding on financial assistance to the Hellenic Republic in order to cope with the Greek government-debt crisis.

This article details the fourteen austerity packages passed by the Government of Greece between 2010 and 2017. These austerity measures were a result of the Greek government-debt crisis and other economic factors. All of the legislation listed remains in force.

The Economic Adjustment Programme for Ireland, usually referred to as the Bailout programme, is a Memorandum of understanding on financial assistance to the Republic of Ireland in order to cope with the Post-2008 Irish financial crisis.

The Economic Adjustment Programme for Cyprus, usually referred to as the Bailout programme, is a memorandum of understanding on financial assistance to the Republic of Cyprus in order to cope with the 2012–13 Cypriot financial crisis.

The Economic Adjustment Programme for Portugal, usually referred to as the Bailout programme, is a Memorandum of understanding on financial assistance to the Portuguese Republic in order to cope with the 2010–14 Portuguese financial crisis.

The troika is a term used to refer to the single decision group created by three entities, the European Commission (EC), the European Central Bank (ECB) and the International Monetary Fund (IMF). It was formed in the aftermath of the European debt crisis as an ad hoc authority with a mandate to manage the bailouts of Cyprus, Greece, Ireland and Portugal, in the aftermath of their prospective insolvency caused by the world financial crisis of 2007–2008.

A repayment plan is a structured repaying of funds that have been loaned to an individual, business or government over either a standard or extended period of time, typically alongside a payment of interest. Repayment plans are prominent within the financial industry of a national economy where liquid funds are in high demand to assist in investment opportunities, governmental expenditure or personal finance. The term first saw prominence with its use by the International Monetary Fund to describe its form of financial loan repayment from individual nations. Typically, the term "repayment plan" refers to the system of Federal Student Aid in the United States of America, which assists in covering tertiary education expenses of domestic students.

In 2009–2010, due to substantial public and private sector debt, and "the intimate sovereign-bank linkages" the eurozone crisis impacted periphery countries. This resulted in significant financial sector instability in Europe; banks' solvency risks grew, which had direct implications for their funding liquidity. The European central bank (ECB), as the monetary union's central bank, responded to the sovereign debt crisis with a series of conventional and unconventional measures, including a decrease in the key policy interest rate, and three-year long-term refinancing operation (LTRO) liquidity injections in December 2011 and February 2012, and the announcement of the outright monetary transactions (OMT) program in the summer of 2012. The ECB acted as a de facto lender-of-last-resort (LOLR) to the euro area banking system, providing banks with cash flow in exchange for collateral, as well as a buyer of last resort (BOLR), purchasing eurozone sovereign bonds. However, the ECB's policies have been criticised for their economic repercussions as well as its political agenda.