An initial public offering (IPO) or stock launch is a public offering in which shares of a company are sold to institutional investors and usually also to retail (individual) investors. An IPO is typically underwritten by one or more investment banks, who also arrange for the shares to be listed on one or more stock exchanges. Through this process, colloquially known as floating, or going public, a privately held company is transformed into a public company. Initial public offerings can be used to raise new equity capital for companies, to monetize the investments of private shareholders such as company founders or private equity investors, and to enable easy trading of existing holdings or future capital raising by becoming publicly traded.

The Securities Act of 1933, also known as the 1933 Act, the Securities Act, the Truth in Securities Act, the Federal Securities Act, and the '33 Act, was enacted by the United States Congress on May 27, 1933, during the Great Depression and after the stock market crash of 1929. It is an integral part of United States securities regulation. It is legislated pursuant to the Interstate Commerce Clause of the Constitution.

Trustee is a legal term which, in its broadest sense, is a synonym for anyone in a position of trust and so can refer to any individual who holds property, authority, or a position of trust or responsibility for the benefit of another. A trustee can also be a person who is allowed to do certain tasks but not able to gain income. Although in the strictest sense of the term a trustee is the holder of property on behalf of a beneficiary, the more expansive sense encompasses persons who serve, for example, on the board of trustees of an institution that operates for a charity, for the benefit of the general public, or a person in the local government.

A joint venture (JV) is a business entity created by two or more parties, generally characterized by shared ownership, shared returns and risks, and shared governance. Companies typically pursue joint ventures for one of four reasons: to access a new market, particularly emerging market; to gain scale efficiencies by combining assets and operations; to share risk for major investments or projects; or to access skills and capabilities.

A fiduciary is a person who holds a legal or ethical relationship of trust with one or more other parties. Typically, a fiduciary prudently takes care of money or other assets for another person. One party, for example, a corporate trust company or the trust department of a bank, acts in a fiduciary capacity to another party, who, for example, has entrusted funds to the fiduciary for safekeeping or investment. Likewise, financial advisers, financial planners, and asset managers, including managers of pension plans, endowments, and other tax-exempt assets, are considered fiduciaries under applicable statutes and laws. In a fiduciary relationship, one person, in a position of vulnerability, justifiably vests confidence, good faith, reliance, and trust in another whose aid, advice, or protection is sought in some matter. In such a relation, good conscience requires the fiduciary to act at all times for the sole benefit and interest of the one who trusts.

A fiduciary is someone who has undertaken to act for and on behalf of another in a particular matter in circumstances which give rise to a relationship of trust and confidence.

SEC Rule 10b-5, codified at 17 CFR 240.10b-5, is one of the most important rules targeting securities fraud in the United States. It was promulgated by the U.S. Securities and Exchange Commission (SEC), pursuant to its authority granted under § 10(b) of the Securities Exchange Act of 1934. The rule prohibits any act or omission resulting in fraud or deceit in connection with the purchase or sale of any security. The issue of insider trading is given further definition in SEC Rule 10b5-1.

Securities regulation in the United States is the field of U.S. law that covers transactions and other dealings with securities. The term is usually understood to include both federal and state-level regulation by governmental regulatory agencies, but sometimes may also encompass listing requirements of exchanges like the New York Stock Exchange and rules of self-regulatory organizations like the Financial Industry Regulatory Authority (FINRA).

A red herring prospectus, as a first or preliminary prospectus, is a document submitted by a company (issuer) as part of a public offering of securities. Most frequently associated with an initial public offering (IPO), this document, like the previously submitted Form S-1 registration statement, must be filed with the Securities and Exchange Commission (SEC).

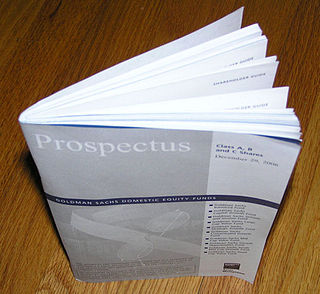

A prospectus, in finance, is a disclosure document that describes a financial security for potential buyers. It commonly provides investors with material information about mutual funds, stocks, bonds and other investments, such as a description of the company's business, financial statements, biographies of officers and directors, detailed information about their compensation, any litigation that is taking place, a list of material properties and any other material information. In the context of an individual securities offering, such as an initial public offering, a prospectus is distributed by underwriters or other financial firms to potential investors. Today, prospectuses are most widely distributed through websites such as EDGAR and its equivalents in other countries.

The United Kingdom company law regulates corporations formed under the Companies Act 2006. Also governed by the Insolvency Act 1986, the UK Corporate Governance Code, European Union Directives and court cases, the company is the primary legal vehicle to organise and run business. Tracing their modern history to the late Industrial Revolution, public companies now employ more people and generate more of wealth in the United Kingdom economy than any other form of organisation. The United Kingdom was the first country to draft modern corporation statutes, where through a simple registration procedure any investors could incorporate, limit liability to their commercial creditors in the event of business insolvency, and where management was delegated to a centralised board of directors. An influential model within Europe, the Commonwealth and as an international standard setter, UK law has always given people broad freedom to design the internal company rules, so long as the mandatory minimum rights of investors under its legislation are complied with.

Erlanger v New Sombrero Phosphate Co (1878) 3 App Cas 1218 is a landmark English contract law, restitution and UK company law case. It concerned rescission for misrepresentation and how the impossibility of counter restitution may be a bar to rescission. It is also an important illustration of how promoters of a company stand in a fiduciary relationship to subscribers.

The corporate opportunity doctrine is the legal principle providing that directors, officers, and controlling shareholders of a corporation must not take for themselves any business opportunity that could benefit the corporation. The corporate opportunity doctrine is one application of the fiduciary duty of loyalty.

The Royal Mail Case or R v Kylsant & Otrs was a noted English criminal case in 1931. The director of the Royal Mail Steam Packet Company, Lord Kylsant, had falsified a trading prospectus with the aid of the company accountant to make it look as if the company was profitable and to entice potential investors. Following an independent audit instigated by HM Treasury, Kylsant and Harold John Morland, the company auditor, were arrested and charged with falsifying both the trading prospectus and company records and accounts. Although they were acquitted of falsifying records and accounts, Kylsant was found guilty of falsifying the trading prospectus and sentenced to twelve months in prison. The company was then liquidated, and reconstituted as The Royal Mail Lines Ltd with the backing of the British government.

Jones v. Harris Associates L.P., 559 U.S. 335 (2010), is a case decided by the United States Supreme Court in which investors claimed that the fees they paid to an investment advisor were too steep, violating the Investment Company Act of 1940.

Guinness plc v Saunders [1989] UKHL 2 is a UK company law case, regarding the power of the company to pay directors. It required that whatever rules exist for payment in the company's articles, they must be strictly observed.

Regulation S-K is a prescribed regulation under the US Securities Act of 1933 that lays out reporting requirements for various SEC filings used by public companies. Companies are also often called issuers, filers or registrants.

Corporate law in Vietnam was originally based on the French commercial law system. However, since Vietnam's independence in 1945, it has largely been influenced by the ruling Communist Party. Currently, the main sources of corporate law are the Law on Enterprises, the Law on Securities and the Law on Investment.

Canadian corporate law concerns the operation of corporations in Canada, which can be established under either federal or provincial authority.

Re Rica Gold Washing Co (1879) 11 Ch D 36 is a UK insolvency law case concerning the liquidation when a company is unable to repay its debts. It held that a shareholder, to having standing to bring a winding up petition must have a sufficient tangible interest in what is left over after winding up.

South African company law is that body of rules which regulates corporations formed under the Companies Act. A company is a business organisation which earns income by the production or sale of goods or services. This entry also covers rules by which partnerships and trusts are governed in South Africa, together with cooperatives and sole proprietorships.