Within the budgetary process, deficit spending is the amount by which spending exceeds revenue over a particular period of time, also called simply deficit, or budget deficit, the opposite of budget surplus. The term may be applied to the budget of a government, private company, or individual. A central point of controversy in economics, government deficit spending was first identified as a necessary economic tool by John Maynard Keynes in the wake of the Great Depression.

The government budget balance, also referred to as the general government balance, public budget balance, or public fiscal balance, is the difference between government revenues and spending. For a government that uses accrual accounting the budget balance is calculated using only spending on current operations, with expenditure on new capital assets excluded. A positive balance is called a government budget surplus, and a negative balance is a government budget deficit. A government budget presents the government's proposed revenues and spending for a financial year.

The Barnett formula is a mechanism used by the Treasury in the United Kingdom to automatically adjust the amounts of public expenditure allocated to Northern Ireland, Scotland and Wales to reflect changes in spending levels allocated to public services in England, Scotland and Wales, as appropriate. The formula applies to a large proportion, but not the whole, of the devolved governments' budgets − in 2013–14 it applied to about 85% of the Scottish Parliament's total budget.

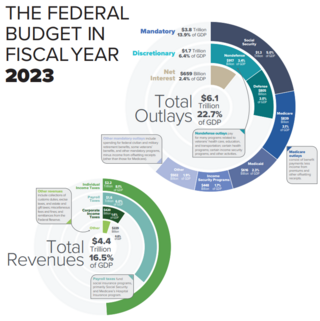

The United States budget comprises the spending and revenues of the U.S. federal government. The budget is the financial representation of the priorities of the government, reflecting historical debates and competing economic philosophies. The government primarily spends on healthcare, retirement, and defense programs. The non-partisan Congressional Budget Office provides extensive analysis of the budget and its economic effects. CBO estimated in February 2024 that Federal debt held by the public is projected to rise from 99 percent of GDP in 2024 to 116 percent in 2034 and would continue to grow if current laws generally remained unchanged. Over that period, the growth of interest costs and mandatory spending outpaces the growth of revenues and the economy, driving up debt. Those factors persist beyond 2034, pushing federal debt higher still, to 172 percent of GDP in 2054.

A government budget or a budget is a projection of the government's revenues and expenditure for a particular period of time often referred to as a financial or fiscal year, which may or may not correspond with the calendar year. Government revenues mostly include taxes while expenditures consist of government spending. A government budget is prepared by the Central government or other political entity. In most parliamentary systems, the budget is presented to the legislature and often requires approval of the legislature. Through this budget, the government implements economic policy and realizes its program priorities. Once the budget is approved, the use of funds from individual chapters is in the hands of government ministries and other institutions. Revenues of the state budget consist mainly of taxes, customs duties, fees and other revenues. State budget expenditures cover the activities of the state, which are either given by law or the constitution. The budget in itself does not appropriate funds for government programs, hence need for additional legislative measures. The word budget comes from the Old French bougette.

The Finance Commissions are commissions periodically constituted by the President of India under Article 280 of the Indian Constitution to define the financial relations between the central government of India and the individual state governments. The First Commission was established in 1951 under The Finance Commission Act, 1951. Fifteen Finance Commissions have been constituted since the promulgation of Indian Constitution in 1950. Individual commissions operate under the terms of reference which are different for every commission, and they define the terms of qualification, appointment and disqualification, the term, eligibility and powers of the Finance Commission. As per the constitution, the commission is appointed every five years and consists of a chairman and four other members.

The Indian government has, since war, subsidised many industries and products, from fuel to gas.

The Gadgil formula is named after Dhananjay Ramchandra Gadgil, a social scientist and the first critic of Indian planning. It was evolved in 1969 for determining the allocation of central assistance for state plans in India. Gadgil formula was adopted for distribution of plan assistance during Fourth and Fifth Five Year Plans.

The Fiscal Responsibility and Budget Management Act, 2003 (FRBMA) is an Act of the Parliament of India to institutionalize financial discipline, reduce India's fiscal deficit, improve macroeconomic management and the overall management of the public funds by moving towards a balanced budget and strengthen fiscal prudence. The main purpose was to eliminate revenue deficit of the country and bring down the fiscal deficit to a manageable 3% of the GDP by March 2008. However, due to the 2007 international financial crisis, the deadlines for the implementation of the targets in the act was initially postponed and subsequently suspended in 2009. In 2011, given the process of ongoing recovery, Economic Advisory Council publicly advised the Government of India to reconsider reinstating the provisions of the FRBMA. N. K. Singh is currently the Chairman of the review committee for Fiscal Responsibility and Budget Management Act, 2003, under the Ministry of Finance (India), Government of India.

The Eleventh Finance Commission of India was appointed by the President on 3 July 1998 for the period 2000-2005.

The Twelfth Finance Commission of India was appointed on 1 November 2002 to make recommendations on the distribution of net proceeds of sharable taxes between union and states. The commission was headed by veteran economist of India, C. Rangarajan. The commission submitted its report on 30 November 2004 and covered the period from 2005-10.

Government Expenditure and Revenue Scotland (GERS) is an annual estimate of the level of public revenue raised in Scotland and the level of public spending for the residents of Scotland under current constitutional arrangements. It was first published in 1992, and yearly since 1995, with the exceptions of 2007 where there was no report due to a methodology review, and 2016 where there were two annual reports due to an acceleration of publishing timescale.

Deficit reduction in the United States refers to taxation, spending, and economic policy debates and proposals designed to reduce the federal government budget deficit. Government agencies including the Government Accountability Office (GAO), Congressional Budget Office (CBO), the Office of Management and Budget (OMB), and the U.S. Treasury Department have reported that the federal government is facing a series of important long-run financing challenges, mainly driven by an aging population, rising healthcare costs per person, and rising interest payments on the national debt.

The Second Finance Commission of India was constituted by president Rajendra Prasad on 1 June 1956.

The Ninth Finance Commission of India was set up in June 1987 under the chairmanship of Mr. N.K.P Salve.

The Fifteenth Finance Commission is an Indian Finance Commission constituted in November 2017 and is to give recommendations for devolution of taxes and other fiscal matters for five fiscal years, commencing 2020-04-01. The commission's chairman is Nand Kishore Singh, a senior member of the Bharatiya Janata Party (BJP) since March 2014, with its full-time members being Ajay Narayan Jha, Ashok Lahiri and Anoop Singh. In addition, the commission also has a part-time member in Ramesh Chand.

Taxation in Wales typically comprises payments to one or more of the three different levels of government: the UK government, the Welsh Government, and local government.

From 1999 to 2022 Wales has had a negative fiscal balance, due to public spending in Wales exceeding tax revenue. For the 2018–19 fiscal year, the fiscal deficit was about 19.4 percent of Wales's estimated GDP, compared to 2 percent for the United Kingdom as a whole. All UK nations and regions except for East, South East England and London have a deficit. Wales' fiscal deficit per capita of £4,300 is the second highest of the economic regions, after the Northern Ireland fiscal deficit, which is nearly £5,000 per capita.

Old Pension Scheme (OPS) in India was abolished as a part of pension reforms by Union Government. Repealed from 1 January 2004, it had a defined-benefit (DB) pension of half the Last Pay Drawn (LPD) at the time of retirement along with components like Dearness Allowances (DA) etc. OPS was an unfunded pension scheme financed on a pay-as-you-go (PAYG) basis in which current revenues of the government funded the pension benefit for its retired employees. Old Pension Scheme was replaced by a restructured defined-contribution (DC) pension scheme called the National Pension System.