History

After the Andorran Constitution came into force, the qualified law delimiting the powers of the Comuns, of November 4, 1993, configures and delimits the powers of the commons within the framework of their self-government. [1]

During the period 1994–1996, an important activity of tax development was observed with the creation of five new taxes:

- Vehicle ownership rate (1994).

- Trademark Office Fees (1995).

- Tax on the registration of holders of economic activities (1995).

- Court fees (1995).

- Tax on the game of bingo (1996).

In 2000, the legislature approved the Law on the Tax on the provision of services (ISI), in accordance with the political model of generalizing indirect taxation to all sectors of the economy. It is a framework law that establishes the bases for indirect taxation on services and that, through specific laws, within two years, must be developed in all sectors.

In May 2002, the indirect tax on the provision of banking and financial services (currently repealed), and the indirect tax on the provision of Insurance services were approved. The same year, the rate was approved by reason of the notarized public faith service (currently repealed) and the tax on real estate property transfers within the framework of fiscal co-responsibility between the commons and the Government.

In 2003, Law 10/2003, of June 27, on communal finances unifies the essential elements of communal taxes and homogenizes the bases of the various tax figures that these local administrations develop through the respective ordinances. On November 3 of the same year, the three specific tax laws were passed that generalize indirect taxation to all sectors of the economy:

These three new taxes, which entered into force on January 1, 2006, were replaced by the indirect general tax (IGI), which entered into force on January 1, 2013.

Government direct taxation begins in 2006 with the entry into force of the capital gains tax on property transfers. It is a direct tax that is taxed on the increase in the value of real estate that is evidenced by the inter vivos, onerous or lucrative transfers of real estate, as well as by the constitutions or transfers of real rights over them.

On December 29, 2010, three major taxes were approved in the field of direct taxation. They are:

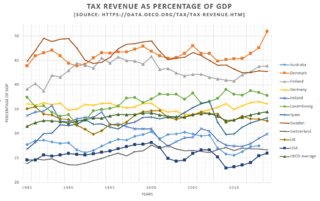

In 2013, Andorra announced plans to impose an income tax in response to pressure from the European Union. [3] The tax was introduced in 2015, at a flat rate of 10%. [4] Also the General Indirect Tax (IGI) was applied. Its introduction allowed replacing the vast majority of existing indirect tax figures that taxed the consumption produced in the territory. In this way, the indirect taxation framework becomes more neutral and efficient for companies and fairer for citizens.

In 2014, the Department of Taxes and Borders was created, with the aim of establishing an administrative authority in charge of managing the tax system and the customs system, equipped with human resources and legal mechanisms that allow for management and collection effective income of a tax nature.

Finally, on January 1, 2014, the Personal Income Tax (IRPF) came into force, which completes the configuration of the Andorran fiscal framework and introduces a tax system comparable to that existing in other neighboring countries, the European Union and the OECD. The new tax covers all the income that the taxpayer may obtain, regardless of its type and source, also incorporating business income that until then was taxed on income tax from economic activities.

- Law 5/2014, of April 24, on the Income Tax of natural persons

- Law 42/2014, of December 11, amending Law 5/2014, of April 24, on Personal Income Tax

Banking secrecy and Tax Haven status

In 2016, Andorra took steps to renounce banking secrecy to end its status as a tax haven. [5]