A debit card is a payment card that can be used in place of cash to make purchases. It is similar to a credit card, but unlike a credit card, the money for the purchase must be in the cardholder's bank account at the time of a purchase and is immediately transferred directly from that account to the merchant's account to pay for the purchase.

Electronic funds transfer at point of sale is an electronic payment system involving electronic funds transfers based on the use of payment cards, such as debit or credit cards, at payment terminals located at points of sale. EFTPOS technology was developed during the 1980s. In Australia and New Zealand, it is also the brand name of a specific system used for such payments; these systems are mainly country-specific and do not interconnect. In Singapore, it is known as NETS.

A telephone card, calling card or phonecard for short, is a credit card-size plastic or paper card, used to pay for telephone services. It is not necessary to have the physical card except with a stored-value system; knowledge of the access telephone number to dial and the PIN is sufficient. Standard cards which can be purchased and used without any sort of account facility give a fixed amount of credit and are discarded when used up; rechargeable cards can be topped up, or collect payment in arrears. The system for payment and the way in which the card is used to place a telephone call vary from card to card.

A smart card, chip card, or integrated circuit card is a physical electronic authorization device, used to control access to a resource. It is typically a plastic credit card-sized card with an embedded integrated circuit (IC) chip. Many smart cards include a pattern of metal contacts to electrically connect to the internal chip. Others are contactless, and some are both. Smart cards can provide personal identification, authentication, data storage, and application processing. Applications include identification, financial, mobile phones (SIM), public transit, computer security, schools, and healthcare. Smart cards may provide strong security authentication for single sign-on (SSO) within organizations. Numerous nations have deployed smart cards throughout their populations.

The point of sale (POS) or point of purchase (POP) is the time and place where a retail transaction is completed. At the point of sale, the merchant calculates the amount owed by the customer, indicates that amount, may prepare an invoice for the customer, and indicates the options for the customer to make payment. It is also the point at which a customer makes a payment to the merchant in exchange for goods or after provision of a service. After receiving payment, the merchant may issue a receipt for the transaction, which is usually printed but can also be dispensed with or sent electronically.

A charge card is a type of credit card that enables the cardholder to make purchases which are paid for by the card issuer. The cardholder is obligated to repay the debt to the card issuer in full by the due date, usually on a monthly basis, or be subject to late fees and restrictions on further card use. Whilst regular credit cards have spending limits, charge cards typically do not. Most charge cards are held by businesses or corporations and are issued to customers with good or excellent credit score.

A turnstile is a form of gate which allows one person to pass at a time. A turnstile can be configured to enforce one-way human traffic. In addition, a turnstile can restrict passage only to people who insert a coin, ticket, pass, or other method of payment. Modern turnstiles incorporate biometrics, including retina scanning, fingerprints, and other individual human characteristics which can be scanned. Thus a turnstile can be used in the case of paid access, for example to access public transport, a pay toilet, or to restrict access to authorized people, for example in the lobby of an office building.

The Oyster card is a payment method for public transport in London in the United Kingdom. A standard Oyster card is a blue credit-card-sized stored-value contactless smart card. It is promoted by Transport for London (TfL) and can be used on travel modes across London including London Buses, London Underground, the Docklands Light Railway (DLR), London Overground, Tramlink, some river boat services, and most National Rail services within the London fare zones. Since its introduction in June 2003, more than 86 million cards have been used.

SmarTrip is a contactless stored-value smart card payment system managed by the Washington Metropolitan Area Transit Authority (WMATA). The Maryland Transit Administration (MTA) uses a compatible payment system called CharmCard. A reciprocity agreement between the MTA and WMATA allows either card to be used for travel on any of the participating transit systems in the Baltimore-Washington metropolitan area. Unlike traditional paper farecards or bus passes, SmarTrip/CharmCard is designed to be permanent and reloadable; the term "SmarTrip" may refer to both payment systems unless otherwise noted.

A bouncer is a type of security guard, employed at venues such as bars, nightclubs, cabaret clubs, stripclubs, casinos, hotels, billiard halls, restaurants, sporting events, schools, or concerts. A bouncer's duties are to provide security, to check legal age and drinking age, to refuse entry for intoxicated persons, and to deal with aggressive behavior or non-compliance with statutory or establishment rules. They are civilians and they are often hired directly by the venue, rather than by a security firm. Bouncers are often required where crowd size, clientele or alcohol consumption may make arguments or fights a possibility, or where the threat or presence of criminal gang activity or violence is high. At some clubs, bouncers are also responsible for "face control", choosing who is allowed to patronize the establishment. In the United States, civil liability and court costs related to the use of force by bouncers are "the highest preventable loss found within the [bar] industry", as many United States bouncers are often taken to court and other countries have similar problems of excessive force. In many countries, federal or state governments have taken steps to professionalise the industry by requiring bouncers to have training, licensing, and a criminal records background check.

The EZ-Link card is a rechargeable contactless smart card and electronic money system that is primarily used as a payment method for public transport such as bus and rail lines in Singapore. A standard EZ-Link card is a credit-card-sized stored-value contact-less smart-card that comes in a variety of colours, as well as limited edition designs. It is sold by TransitLink Pte Ltd, a subsidiary of the Land Transport Authority (LTA), and can be used on travel modes across Singapore, including the Mass Rapid Transit (MRT), the Light Rail Transit (LRT), public buses which are operated by SBS Transit, SMRT Buses, Tower Transit Singapore and Go-Ahead Singapore, as well as the Sentosa Express.

An e-commerce payment system facilitates the acceptance of electronic payment for offline transfer, also known as a subcomponent of electronic data interchange (EDI), e-commerce payment systems have become increasingly popular due to the widespread use of the internet-based shopping and banking.

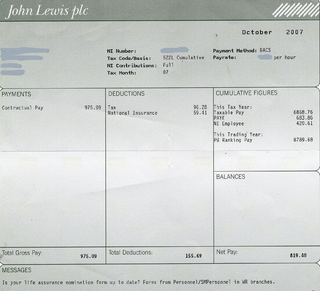

A paycheck, also spelled pay check or pay cheque, is traditionally a paper document issued by an employer to pay an employee for services rendered. In recent times, the physical paycheck has been increasingly replaced by electronic direct deposits to the employee's designated bank account or loaded onto a payroll card. Employees may still receive a pay slip to detail the calculations of the final payment amount.

A cover charge is an entrance fee sometimes charged at bars, nightclubs, or restaurants. The American Heritage Dictionary defines it as a "fixed amount added to the bill at a nightclub or restaurant for entertainment or service." In restaurants, cover charges generally do not include the cost of food that is specifically ordered, but in some establishments, they do include the cost of bread, butter, olives and other accompaniments which are provided as a matter of course.

A contactless smart card is a contactless credential whose dimensions are credit-card size. Its embedded integrated circuits can store data and communicate with a terminal via NFC. Commonplace uses include transit tickets, bank cards and passports.

A digital wallet, also known as e-wallet, is an electronic device, online service, or software program that allows one party to make electronic transactions with another party bartering digital currency units for goods and services. This can include purchasing items on-line with a computer or using a smartphone to purchase something at a store. Money can be deposited in the digital wallet prior to any transactions or, in other cases, an individual's bank account can be linked to the digital wallet. Users might also have their driver's license, health card, loyalty card(s) and other ID documents stored within the wallet. The credentials can be passed to a merchant's terminal wirelessly via near field communication (NFC). Increasingly, digital wallets are being made not just for basic financial transactions but to also authenticate the holder's credentials. For example, a digital wallet could verify the age of the buyer to the store while purchasing alcohol. The system has already gained popularity in Japan, where digital wallets are known as "wallet mobiles". A cryptocurrency wallet is a digital wallet where private keys are stored for cryptocurrencies like bitcoin.

The Breeze Card is a stored value smart card that passengers use as part of an automated fare collection system which the Metropolitan Atlanta Rapid Transit Authority (MARTA) introduced to the general public in early October 2006. The card automatically debits the cost of the passenger’s ride when placed on or near the Breeze Target at the fare gate. Transit riders are able to add value or time-based passes to the card at Breeze Vending Machines (BVM) located at all MARTA stations. The major phases of MARTA's Breeze transformation took place before July 1, 2007 when customers were still able to purchase TransCards from ridestores or their employers. They were also able to obtain paper transfers from bus drivers to access the train. As of July 1, 2007 the TransCard and the paper transfers were discontinued and patrons now use a Breeze Card or ticket to access the system, and all transfers are loaded on the card. Breeze Vending Machines (BVM) distribute regional transit provider passes The Breeze Card employs passive RFID technology currently in use in many transit systems around the world.

A credit card is a payment card issued to users (cardholders) to enable the cardholder to pay a merchant for goods and services based on the cardholder's accrued debt. The card issuer creates a revolving account and grants a line of credit to the cardholder, from which the cardholder can borrow money for payment to a merchant or as a cash advance. There are two credit card groups: consumer credit cards and business credit cards. Most cards are plastic, but some are metal cards, and a few gemstone-encrusted metal cards.

A surcharge, also known as checkout fee, is an extra fee charged by a merchant when receiving a payment by cheque, credit card, charge card or debit card which at least covers the cost to the merchant of accepting that means of payment, such as the merchant service fee imposed by a credit card company. Retailers generally incur higher costs when consumers choose to pay by credit card due to higher merchant service fees compared to traditional payment methods such as cash.

Apple Pay is a mobile payment and digital wallet service by Apple Inc. that allows users to make payments in person, in iOS apps, and on the web using Safari. It is supported on the iPhone, Apple Watch, iPad, and Mac. It is not available on any client device that is not made and sold by Apple. It digitizes and can replace a credit or debit card chip and PIN transaction at a contactless-capable point-of-sale terminal. It does not require Apple Pay-specific contactless payment terminals; it can work with any merchant that accepts contactless payments. It adds two-factor authentication via Touch ID, Face ID, PIN, or passcode. Devices wirelessly communicate with point of sale systems using near field communication (NFC), with an embedded secure element (eSE) to securely store payment data and perform cryptographic functions, and Apple's Touch ID and Face ID for biometric authentication.