Finance is the study and discipline of money, currency and capital assets. It is related to and distinct from economics, which is the study of the production, distribution, and consumption of goods and services. Based on the scope of financial activities in financial systems, the discipline can be divided into personal, corporate, and public finance.

The International Finance Corporation (IFC) is an international financial institution that offers investment, advisory, and asset-management services to encourage private-sector development in less developed countries. The IFC is a member of the World Bank Group and is headquartered in Washington, D.C. in the United States.

A capital market is a financial market in which long-term debt or equity-backed securities are bought and sold, in contrast to a money market where short-term debt is bought and sold. Capital markets channel the wealth of savers to those who can put it to long-term productive use, such as companies or governments making long-term investments. Financial regulators like Securities and Exchange Board of India (SEBI), Bank of England (BoE) and the U.S. Securities and Exchange Commission (SEC) oversee capital markets to protect investors against fraud, among other duties.

The European Investment Bank (EIB) is the European Union's investment bank and is owned by the 27 member states. It is the largest multilateral financial institution in the world. The EIB finances and invests both through equity and debt solutions companies and projects that achieve the policy aims of the European Union through loans, equity and guarantees.

The money market is a component of the economy that provides short-term funds. The money market deals in short-term loans, generally for a period of a year or less.

Financial services are economic services tied to finance provided by financial institutions. Financial services encompass a broad range of service sector activities, especially as concerns financial management and consumer finance.

A money market fund is an open-end mutual fund that invests in short-term debt securities such as US Treasury bills and commercial paper. Money market funds are managed with the goal of maintaining a highly stable asset value through liquid investments, while paying income to investors in the form of dividends. Although they are not insured against loss, actual losses have been quite rare in practice.

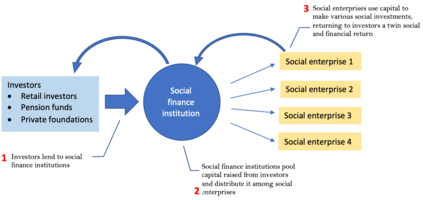

An institutional investor is an entity that pools money to purchase securities, real property, and other investment assets or originate loans. Institutional investors include commercial banks, central banks, credit unions, government-linked companies, insurers, pension funds, sovereign wealth funds, charities, hedge funds, real estate investment trusts, investment advisors, endowments, and mutual funds. Operating companies which invest excess capital in these types of assets may also be included in the term. Activist institutional investors may also influence corporate governance by exercising voting rights in their investments. In 2019, the world's top 500 asset managers collectively managed $104.4 trillion in Assets under Management (AuM).

The Caisse de dépôt et placement du Québec is an institutional investor that manages several public and parapublic pension plans and insurance programs in Quebec. It was established in 1965 by an act of the National Assembly, under the government of Jean Lesage, as part of the Quiet Revolution, a period of social and political change in Quebec. It is the second-largest pension fund in Canada, after the Canada Pension Plan Investment Board. It was created to manage the funds of the newly created Quebec Pension Plan, a public pension plan that aimed to provide financial security for Quebecers in retirement. The CDPQ’s mandate was to invest the funds prudently and profitably, while also contributing to Quebec’s economic development. As of December 31, 2023, CDPQ managed assets of C$434 billion, invested in Canada and elsewhere. CDPQ is headquartered in Quebec City at the Price building and has its main business office in Montreal at Édifice Jacques-Parizeau.

The following outline is provided as an overview of and topical guide to finance:

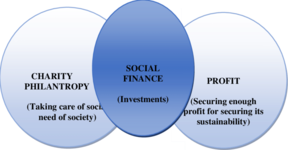

Socially responsible investing (SRI) is any investment strategy which seeks to consider both financial return and social/environmental good. The areas of concern recognized by the SRI practitioners are sometimes summarized under the heading of environmental, social and governance (ESG) issues: environment, social, and corporate governance. Impact investing is subset of SRI that is generally more proactive and focused on the conscious creation of social impact through investment. Eco-investing is SRI with a focus on environmentalism.

Conservation finance is the practice of raising and managing capital to support land, water, and resource conservation. Conservation financing options vary by source from public, private, and nonprofit funders; by type from loans, to grants, to tax incentives, to market mechanisms; and by scale ranging from federal to state, national to local.

Impact investing refers to investments "made into companies, organizations, and funds with the intention to generate a measurable, beneficial social or environmental impact alongside a financial return". At its core, impact investing is about an alignment of an investor's beliefs and values with the allocation of capital to address social and/or environmental issues.

Big Society Capital Limited (BSC) is a social impact investor in the United Kingdom. Its mission is to grow the amount of money invested in tackling social issues and inequalities in the UK. It invests its own capital as well as enabling others to invest for impact too. The capital finances front-line social purpose organizations tackling everything from homelessness to mental health and fuel poverty, enabling them to grow and increase their impact.

Climate finance is an umbrella term for loans, investments, and other forms of financial capital allocation in the area of climate change mitigation, adaptation and/or resiliency.

The Nigerian Capital Development Fund (NCDF) is an independent social investment financial intermediary institution. This hybrid organization was set up mainly to address the challenges of poverty in low income rural communities in Nigeria. The institution mobilizes capital from the public and private sectors to invest in projects, businesses and social enterprises with the intention to generate good financial returns and measurable positive social-environmental impact, as well as act as a champion to help increase awareness and confidence on the advantages of impact investing.

Malaysia's independence in 1957 was a catalyst for growth. As the nation took charge of managing its own affairs, it continued to develop the goals and means necessary for a financial structure conducive to the economic growth observed today. Critical to the transition of Malaysia from a low-income country to one of high-income status has been the expansion of its economy. From a commodity and agricultural-based economy, the Southeast Asian nation is transitioning to a leading exporter of more complex goods. As the nation opens up to trade and investment, the World Bank and the International Bank for Reconstruction and Development (IBRD) and International Development Association (IDA) continue to assist with its development.

The Capital Markets Union (CMU) is an economic policy initiative launched by the former president of the European Commission, Jean-Claude Juncker in the initial exposition of his policy agenda on 15 July 2014. The main target was to create a single market for capital in the whole territory of the EU by the end of 2019. The reasoning behind the idea was to address the issue that corporate finance relies on debt (i.e. bank loans) and the fact that capital markets in Europe were not sufficiently integrated so as to protect the EU and especially the Eurozone from future crisis. The Five Presidents Report of June 2015 proposed the CMU in order to complement the Banking union of the European Union and eventually finish the Economic and Monetary Union (EMU) project. The CMU is supposed to attract 2000 billion dollars more on the European capital markets, on the long-term.

Sustainable finance is the set of practices, standards, norms, regulations and products that pursue financial returns alongside environmental and/or social objectives. It is sometimes used interchangeably with Environmental, Social & Governance (ESG) investing. However, many distinguish between ESG integration for better risk-adjusted returns and a broader field of sustainable finance that also includes impact investing, social finance and ethical investing.

Sovereign funds of China are mechanisms through which the Chinese state acts as a market participant with the goals of supporting key domestic economic sectors, advancing strategic interests internationally, and diversifying its foreign exchange reserves.