A flat tax is a tax with a single rate on the taxable amount, after accounting for any deductions or exemptions from the tax base. It is not necessarily a fully proportional tax. Implementations are often progressive due to exemptions, or regressive in case of a maximum taxable amount. There are various tax systems that are labeled "flat tax" even though they are significantly different. The defining characteristic is the existence of only one tax rate other than zero, as opposed to multiple non-zero rates that vary depending on the amount subject to taxation.

National Insurance (NI) is a fundamental component of the welfare state in the United Kingdom. It acts as a form of social security, since payment of NI contributions establishes entitlement to certain state benefits for workers and their families.

Payroll taxes are taxes imposed on employers or employees, and are usually calculated as a percentage of the salaries that employers pay their employees. By law, some payroll taxes are the responsibility of the employee and others fall on the employer, but almost all economists agree that the true economic incidence of a payroll tax is unaffected by this distinction, and falls largely or entirely on workers in the form of lower wages. Because payroll taxes fall exclusively on wages and not on returns to financial or physical investments, payroll taxes may contribute to underinvestment in human capital, such as higher education.

Taxation in Ireland in 2017 came from Personal Income taxes, and Consumption taxes, being VAT and Excise and Customs duties. Corporation taxes represents most of the balance, but Ireland's Corporate Tax System (CT) is a central part of Ireland's economic model. Ireland summarises its taxation policy using the OECD's Hierarchy of Taxes pyramid, which emphasises high corporate tax rates as the most harmful types of taxes where economic growth is the objective. The balance of Ireland's taxes are Property taxes and Capital taxes.

In France, taxation is determined by the yearly budget vote by the French Parliament, which determines which kinds of taxes can be levied and which rates can be applied.

Due to the absence of the tax code in Argentina, the tax regulation takes place in accordance with separate laws, which, in turn, are supplemented by provisions of normative acts adopted by the executive authorities. The powers of the executive authority include levying a tax on profits, property and added value throughout the national territory. In Argentina, the tax policy is implemented by the Federal Administration of Public Revenue, which is subordinate to the Ministry of Economy. The Federal Administration of Public Revenues (AFIP) is an independent service, which includes: the General Tax Administration, the General Customs Office and the General Directorate for Social Security. AFIP establishes the relevant legal norms for the calculation, payment and administration of taxes:

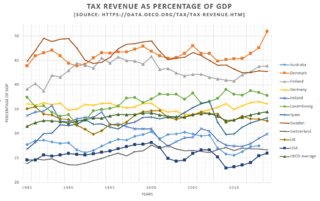

In Austria, taxes are levied by the state and the tax revenue in Austria was 42.7% of GDP in 2016 according to the World Bank The most important revenue source for the government is the income tax, corporate tax, social security contributions, value added tax and tax on goods and services. Another important taxes are municipal tax, real-estate tax, vehicle insurance tax, property tax, tobacco tax. There exists no property tax. The gift tax and inheritance tax were cancelled in 2008. Furthermore, self-employed persons can use a tax allowance of €3,900 per year. The tax period is set for a calendar year. However, there is a possibility of having an exception but a permission of the tax authority must be received. The Financial Secrecy Index ranks Austria as the 35th safest tax haven in the world.

Taxation in Finland is mainly carried out through the Finnish Tax Administration, an agency of the Ministry of Finance. Finnish Customs and the Finnish Transport and Communications Agency Traficom, also collect taxes. Taxes collected are distributed to the Government, municipalities, church, and the Social Insurance Institution, Kela.

Taxation in Norway is levied by the central government, the county municipality and the municipality. In 2012 the total tax revenue was 42.2% of the gross domestic product (GDP). Many direct and indirect taxes exist. The most important taxes – in terms of revenue – are VAT, income tax in the petroleum sector, employers' social security contributions and tax on "ordinary income" for persons. Most direct taxes are collected by the Norwegian Tax Administration and most indirect taxes are collected by the Norwegian Customs and Excise Authorities.

Taxation may involve payments to a minimum of two different levels of government: central government through SARS or to local government. Prior to 2001 the South African tax system was "source-based", where in income is taxed in the country where it originates. Since January 2001, the tax system was changed to "residence-based" wherein taxpayers residing in South Africa are taxed on their income irrespective of its source. Non residents are only subject to domestic taxes.

Taxation in Estonia consists of state and local taxes. A relatively high proportion of government revenue comes from consumption taxes whilst revenue from capital taxes is one of the lowest in the European Union.

Czech Republic's current tax system was put into administration on 1 January 1993. Since then, an updated VAT act was introduced on 1 May 2004 when Czech Republic joined the EU and the act had to correspond to EU law. In 2008, the administration also introduced Energy Taxation. Changes to tax laws are quite frequent and common in the Czech Republic due to a dynamic economy. The highest levels of revenue are generated from income tax, social security contributions, value-added tax and corporate tax. In 2015, total revenue stood at CZK 670.216 billion which was 36.3% of GDP. The tax quota of the Czech Republic is lower than the EU average. Compared to the averages of the OECD countries, revenues generated from taxes on social security contributions, corporate income and gains and value added taxes account for higher proportions of total taxation revenue. Personal income tax lies on the other end of the spectrum where the revenue is proportionally much lower than the OECD average. Taxes on property also account for lower levels of revenue.

Taxes in Poland are levied by both the central and local governments. Tax revenue in Poland is 33.9% of the country's GDP in 2017. The most important revenue sources include the income tax, Social Security, corporate tax and the value added tax, which are all applied on the national level.

Taxes in Lithuania are levied by the central and the local governments. Most important revenue sources include the value added tax, personal income tax, excise tax and corporate income tax, which are all applied on the central level. In addition, social security contributions are collected in a social security fund, outside the national budget. Taxes in Lithuania are administered by the State Tax Inspectorate, the Customs Department and the State Social Insurance Fund Board. In 2019, the total government revenue in Lithuania was 30.3% of GDP.

In Latvia, taxes are levied by both national and local governments. Tax revenue stood at 28.1% of the GDP in 2013. The most important revenue sources include income tax, social security, corporate tax and value added tax, which are all applied on the national level. Income taxes are levied at a flat rate of 23% on all income. A long range of tax allowances is given including a standard allowance of €900 per year and €1980 per year for every dependent.

Taxation in Bosnia and Herzegovina includes both federal and local taxes. Tax revenue in Bosnia and Herzegovina stood at 28.6% of GDP in 2013. Most important revenue sources include the income tax, Social Security contributions, corporate tax, and the value added tax, which are all applied on the federal level.

Taxation in Belgium consists of taxes that are collected on both state and local level. The most important taxes are collected on federal level, these taxes include an income tax, social security, corporate taxes and value added tax. At the local level, property taxes as well as communal taxes are collected. Tax revenue stood at 48% of GDP in 2012.

Taxes in Cyprus are levied by both the central and local governments. Tax revenue stood at 39.2% of GDP in 2012. The most important revenue sources are the income tax, social security, value-added tax and corporate tax, and are all collected by the central government.

Taxation in Malta is levied by the State and it is administered by the Commissioner for Revenue. The total tax revenues in 2014 amounted to €2.747 Billion, which represents 34.6% of the Maltese GDP. The main sources of tax revenue were value-added tax, income tax, and social security contributions.

Tax revenue in Luxembourg was 38.65% of GDP in 2017, which is just above the average OECD in 2017.