Type of short term debt instrument in the United States

This article is about an obsolete class of short-term debt obligations issued by the United States during the 19th century. For other uses, see Treasury Note (disambiguation).

An unissued $10 Small Treasury Note, authorized by the Act of February 24, 1815. This particular note is a remainder which was given a serial number but was never countersigned.

A Treasury Note is a type of short term debt instrument issued by the United States prior to the creation of the Federal Reserve System in 1913. Without the alternatives offered by a federal paper money or a central bank, the U.S. government relied on these instruments for funding during periods of financial stress such as the War of 1812, the Panic of 1837, and the American Civil War. While the Treasury Notes, as issued, were neither legal tender nor representative money, some issues were used as money in lieu of an official federal paper money. However the motivation behind their issuance was always funding federal expenditures rather than the provision of a circulating medium. These notes typically were hand-signed, of large denomination (at least $50), of large dimension (bigger than private banknotes), bore interest, were payable to the order of the owner (whose name was written on the front of the note), and matured in no more than three years – though some issues lacked one or more of these properties. Often they were receivable at face value by the government in payment of taxes and for purchases of publicly owned land,[1] and thus "might to some extent be regarded as paper money."[2] On many issues the interest rate was chosen to make interest calculations particularly easy, paying either 1, 1+1⁄2, or 2 cents per day on a $100 note.

Characteristically, the issues were not extensive and, as it has been observed, "the polite fiction was always maintained that Treasury Notes did not serve as money when, in fact, to a limited extent they did."[3] The value of these notes varied, being worth more or less than par as market conditions fluctuated, and they rapidly disappeared from the financial system after the crisis associated with their issuance had ended.

The ante-bellum Treasury Notes did not have legal tender status, but financial innovation during the Civil War caused the term Treasury Note to become associated with legal tender instruments such as the United States Notes introduced in 1862 and the Compound Interest Treasury Notes introduced in 1863. The appearance of these new obligations, together with the changes brought about by the National Banking Act, effectively eliminated most of the uses of the old Treasury Notes as money and the term Certificate of Indebtedness was introduced to apply to new notes which possessed the debt-like aspects of the pre-war Notes. Today the Treasury's short term debt needs are fulfilled by Treasury bills.

Origin

The early finances of the central government of the United States were precarious. To help finance the American Revolution the Continental Congress had issued Continental Dollars between 1775 and 1779. The paper Continental Dollars nominally entitled the bearer to an equivalent amount of silver Spanish Milled Dollars but were repeatedly devalued and were never redeemed in silver despite the American victory.[4] With the fate of the Continentals in mind, the Founding Fathers embedded in the Constitution no provision for a paper currency, and they forbade the states to make anything but gold or silver a legal tender. As part of the Compromise of 1790, the Continental Dollars were redeemed at a loss of over 99% vs. their face value, but the United States did choose to perform on revolutionary war bond obligations in full by pledging the publicly owned land and the credit of the new federal government against the bonds. As a result, America's early creditors had reason to be wary of a paper currency, but reason to respect its debt.

The Founding Fathers were divided over whether the United States needed a central bank similar to the Bank of England to issue currency and facilitate the government's use of credit. An early American attempt at central banking along these lines was the Bank of North America which played a meaningful role in helping the Congress of the Confederation to arrange its finances during the 1780s, but its rechartering in 1786 prevented it from continuing to act as a central bank. Subsequently, the 1st United States Congress chartered the First Bank of the United States in 1791 to facilitate its financial operations, but in 1811 its charter was not renewed due to opposition from the Madison administration.

Thus, when the declaration of the War of 1812 impaired the government's ability to raise money via the sale of long-term bonds, the United States had no paper currency nor a central bank with which to obtain emergency short-term financing, and it used its borrowing authority to issue short-term debt in the form of Treasury Notes receivable for public dues or bond purchases. Having thus set the precedent, the Treasury would go on to irregularly issue such notes up through the Civil War.

War of 1812

An unissued and untrimmed remainder from a sheet of the first issue of Treasury Notes, authorized by the Act of June 30, 1812. The issued notes of this type were trimmed to size, signed in three places, dated, and endorsed as payable to the order of the purchaser or his/her assignee.

Several issues of Treasury Notes were made during the War of 1812 from 1812 to 1815. Most of these notes paid 5+2⁄5% interest (or 1+1⁄2 cents per day on a $100 note), matured in one year, and were receivable in payment for public dues. While $37 million were issued, no more than $17 million were outstanding at any one time.[5]

Five acts authorized these Notes. The first, on June 20, 1812, authorized 1-year Treasury Notes at 5+2⁄5% interest to fill out the unsubscribed portion of an $11 million loan in support of the war with Britain which had just been declared on the 18th. Only about $6 million of the loan was placed in the form of 6% interest bonds, and thus $5 million of Notes were issued. The Notes were made receivable for all public dues owed the federal government and payable to the order of the owner by endorsement. A further $5 million of similar Notes were authorized on February 25, 1813 to supplement additional loans which had not been fully subscribed. Only Notes of $100 denomination and greater were issued under these first two acts, and they sold at prices close to par.

The next two acts, those of March 4, 1814 and Dec 26, 1814, called for Note issues both to independently raise revenue as well as to substitute for unsubscribed loans. A total of $18,318,400 were emitted under these acts which included Notes of $20 and $50 denominations in addition to the larger Notes.

During 1814 federal finances deteriorated as the war dragged on, and banks outside New England suspended specie payment on August 31, 1814. The value of the Treasury Notes fell below that of specie. New England states were unsympathetic to the war and when the government attempted to withdraw deposits from a Boston bank to make interest payments on October 1, 1814, the bank took the position that it could tender Treasury Notes to the government which were then rejected by the holders of the government bonds who expected payment in specie. These developments led to changes in the final Treasury Note act of the era signed on February 24, 1815. These last notes were divided into large ($100 and over) and small (under $100) denominations, and did not expire at any predetermined time. The large notes paid interest as before, at 5+2⁄5% per annum, but could also be used to purchase 6 percent interest bonds at par (i.e. were fundable into the bonds) as a way of supporting their value.

Small Treasury Notes

Among the several issues of Treasury Notes of special note are the "Small Treasury Notes" authorized by the Act of February 24, 1815 which were intended to circulate as currency in the aftermath of the 1814 suspension of specie payment. The Act had been drafted during the financial disarray late in the War of 1812 and called for Notes of denomination less than $100 which would bear no interest. The issued denominations were as low as $3, their size was typical of banknotes and, unlike the previously issued Notes, they were payable to bearer rather than to order. However, they were not a Legal Tender for private transactions. Like the larger Notes issued under the February 24, 1815 Act, this issue was also supported by the government's promise to receive them at face value for purchasing bonds at par, but in the case of the Small Notes the bonds were to yield 7% interest. Before the notes could be issued, however, the war had ended – an occasion which led to the 7% bonds being worth more than par, and the Small Treasury Notes, of which $3,392,994 were originally issued, were rapidly exchanged for the bonds.[6] In witness to the limited circulation achieved by these notes, only two issued uncancelled examples of the Small Treasury Notes are known today.[7]

An issued, but cancelled, $100 Treasury Note from 1838, issued under the Act of October 12, 1837

The financial difficulties during the War of 1812 contributed to the Madison administration reversing its views on central banking and authorizing the chartering of the Second Bank of the United States for 20 years, 1816–1836. However, when the Jacksonian Democrats rose to power they strongly opposed the bank and began to dismantle its role in federal policy in the mid-1830s. Thus, when the Panic of 1837 struck the federal government was again without the flexibility of a central bank for its short term finances and one result was several issues of Treasury Notes when federal revenues declined during the panic.

The Act of Oct. 12, 1837 authorized $10 million of notes in denominations of at least $50. During the economic recovery in 1838/39, outstanding notes were gradually retired but the recovery failed to take hold and the panic turned into a depression which lasted through the early 1840s and several acts from 1838 to 1843 authorized further issues of Treasury Notes. Of note during this period were agitation by the Whig Party for a central bank and a flirtation with the Treasury Notes as currency. Particularly controversial was an issue by Secretary Spencer of about $850,000 of Treasury Notes endorsed with a promise for immediate repurchase, principal and interest, by the sub-treasury in New York at par in specie. Some members of the Congress complained that such Notes were dangerously close to currency. Also controversial was the practice by the Secretaries to issue some Notes with only nominal interest, a mere 1/1000 of one percent per annum, to "deposit" in private banks and then draw upon the resulting funds via checks.[8]

Mexican–American War

A contemporary imitation of a United States Treasury Note from the Mexican–American War; no such note was actually issued

Treasury Notes were again issued to help finance the Mexican–American War in 1846 and 1847. Including reissues, $33.8 of one year notes were issued with interest rates varying from 1⁄1000 of 1% to 6%.[5]

Panic of 1857

In 1857 federal revenues suffered from the lowered rates of the Tariff of 1857 and decreased economic activity due to the Panic of 1857. At the same time outlays increased with the expensive Utah War. The government resorted to several issues of Treasury Notes from 1857 to 1860.[9]

Early Civil War notes

Treasury Note as authorized by the Morrill Tariff Act of 1861

The Morrill Tariff Act of March 2, 1861, signed into law by President Buchanan, authorized the Secretary of the Treasury to issue six percent interest Treasury Notes if he was unable to issue previously authorized bonds at par.[10] Sixty-day and two-year notes were issued, payable to order, receivable in payment of all debts due to the United States, and exchangeable for bonds at par. They were first issued by President Lincoln's administration just after the Battle of Fort Sumter and until the financing authorized by Act of July 17 became available.[9]

Only one example is known to have survived in issued and uncancelled form.

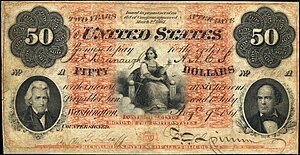

Three year Treasury Notes bearing interest at a rate of 7.30% (seven-thirty) were first authorized by the Act of July 17, 1861 to help finance the Civil War.[11] These notes were payable to order, but the Treasury would issue them in blank form if requested. Secretary of the Treasury Chase suggested this rate of interest in hopes that the ease of interest calculation (a $50 note would accrue interest at one cent per day) would allow the notes to circulate as money, but apparently this did not prove to be the case.[12] Further issues of Seven-Thirties were made in 1864 and 1865. The issue of 1861, which preceded the First Legal Tender Act, paid interest in gold, but the government reserved the right to pay the interest of the 1864 and 1865 issues in either United States Notes at 7.3% or in gold at 6%. The option to pay in gold, however, was never exercised.

The notes could be exchanged, at par, for 20-year United States bonds bearing interest at 6% in gold. When the 1861 issue was maturing in 1864 these bonds were trading at a premium to face value, so most holders of the seven-thirties exercised their right to make the exchange. Almost all of the 1864 and 1865 notes were similarly exchanged.

The Seven-Thirties were issued in denominations of $50, $100, $500, $1,000, and $5,000. The notes are similar in design to the Legal Tender notes of the Civil War era. Today these notes are collectors' items like U.S. paper money, though no more than two or three dozen surviving examples are known.[2]

The Demand Notes were also authorized by the Act of July 17, 1861[11] and were a transitional issue connecting Treasury Notes to modern paper money. The denominations of the Demand Notes ($5, $10 and $20) complemented those of the Seven-Thirties ($50 to $5,000) – much in the way that the Small Treasury Notes of 1815 complemented the Large Notes. The Demand Notes had been intended to function as money, and were payable to bearer, but were authorized within the legal framework of Treasury Notes since the U.S. was not generally assumed to have the authority to issue banknotes at that time. Eventually the Demand Notes were granted legal tender status[13] and were replaced in function by United States Notes.

When the United States Notes were issued they were not receivable in payment of taxes. The 2-year Morrill Tariff act notes and the Demand Notes were outstanding at the time and both were "Receivable in Payment of All Public Dues" and were sold at a premium to United States Notes for the payment of customs taxes. Litigation to secure a similar privilege for the Seven-Thirties was unsuccessful.

Certificates of Indebtedness (Civil War)

The Act of March 1, 1862 authorized the Secretary of the Treasury to issue to public creditors certificates of denominations not less than $1,000, signed by the Treasurer, bearing interest at a rate of 6%, and payable in one year or earlier at the option of the government.[14] While these instruments were Treasury Notes in the pre-Civil war usage of the term, they were called Certificates of Indebtedness to distinguish them from Demand Notes, United States Notes and Seven-Thirties.[15] While these certificates traded below par in the secondary market[16] they could be used by merchants as collateral for obtaining bank loans.[9]

Certificates of Indebtedness (Panic of 1907)

A proof of a $50 Certificate of Indebtedness of the type issued during the Panic of 1907

Authorized in 1898, Certificates of Indebtedness were issued during the Panic of 1907 to serve as backing for an increased circulation of banknotes. The Aldrich–Vreeland Act soon followed and notes of this nature ceased to be issued.

Related Research Articles

The Specie Payment Resumption Act of January 14, 1875 was a law in the United States that restored the nation to the gold standard through the redemption of previously unbacked United States Notes and reversed inflationary government policies promoted directly after the American Civil War. The decision further contracted the nation's money supply and was seen by critics as an exacerbating factor of the so-called Long Depression, which struck in 1873.

Federal Reserve Notes are the currently issued banknotes of the United States dollar. The United States Bureau of Engraving and Printing produces the notes under the authority of the Federal Reserve Act of 1913 and issues them to the Federal Reserve Banks at the discretion of the Board of Governors of the Federal Reserve System. The Reserve Banks then circulate the notes to their member banks, at which point they become liabilities of the Reserve Banks and obligations of the United States.

A United States Note, also known as a Legal Tender Note, is a type of paper money that was issued from 1862 to 1971 in the United States. Having been current for 109 years, they were issued for longer than any other form of U.S. paper money other than the currently issued Federal Reserve Note. They were known popularly as "greenbacks", a name inherited from the earlier greenbacks, the Demand Notes, that they replaced in 1862. Often termed Legal Tender Notes, they were named United States Notes by the First Legal Tender Act, which authorized them as a form of fiat currency. During the early 1860s the so-called second obligation on the reverse of the notes stated:

This Note is a Legal Tender for all debts public and private except Duties on Imports and Interest on the Public Debt; and is receivable in payment of all loans made to the United States.

Legal tender is a form of money that courts of law are required to recognize as satisfactory payment for any monetary debt. Each jurisdiction determines what is legal tender, but essentially it is anything which when offered ("tendered") in payment of a debt extinguishes the debt. There is no obligation on the creditor to accept the tendered payment, but the act of tendering the payment in legal tender discharges the debt.

The United States ten-dollar bill (US$10) is a denomination of U.S. currency. The obverse of the bill features the portrait of Alexander Hamilton, who served as the first U.S. Secretary of the Treasury, two renditions of the torch of the Statue of Liberty, and the words "We the People" from the original engrossed preamble of the United States Constitution. The reverse features the U.S. Treasury Building. All $10 bills issued today are Federal Reserve Notes.

The United States one-hundred-dollar bill (US$100) is a denomination of United States currency. The first United States Note with this value was issued in 1862 and the Federal Reserve Note version was first produced in 1914. Inventor and U.S. Founding Father Benjamin Franklin has been featured on the obverse of the bill since 1914, which now also contains stylized images of the Declaration of Independence, a quill pen, the Syng inkwell, and the Liberty Bell. The reverse depicts Independence Hall in Philadelphia, which it has featured since 1928.

Large denominations of United States currency greater than $100 were circulated by the United States Treasury until 1969. Since then, U.S. dollar banknotes have been issued in seven denominations: $1, $2, $5, $10, $20, $50, and $100.

Silver certificates are a type of representative money issued between 1878 and 1964 in the United States as part of its circulation of paper currency. They were produced in response to silver agitation by citizens who were angered by the Fourth Coinage Act, which had effectively placed the United States on a gold standard. The certificates were initially redeemable for their face value of silver dollar coins and later in raw silver bullion. Since 1968 they have been redeemable only in Federal Reserve Notes and are thus obsolete, but still valid legal tender at their face value and thus are still an accepted form of currency.

Gold certificates were issued by the United States Treasury as a form of representative money from 1865 to 1933. While the United States observed a gold standard, the certificates offered a more convenient way to pay in gold than the use of coins. General public ownership of gold certificates was outlawed in 1933 and since then they have been available only to the Federal Reserve Banks, with book-entry certificates replacing the paper form.

National Bank Notes were United States currency banknotes issued by National Banks chartered by the United States Government. The notes were usually backed by United States bonds the bank deposited with the United States Treasury. In addition, banks were required to maintain a redemption fund amounting to five percent of any outstanding note balance, in gold or "lawful money." The notes were not legal tender in general, but were satisfactory for nearly all payments to and by the federal government.

The history of the United States dollar began with moves by the Founding Fathers of the United States of America to establish a national currency based on the Spanish silver dollar, which had been in use in the North American colonies of the Kingdom of Great Britain for over 100 years prior to the United States Declaration of Independence. The new Congress's Coinage Act of 1792 established the United States dollar as the country's standard unit of money, creating the United States Mint tasked with producing and circulating coinage. Initially defined under a bimetallic standard in terms of a fixed quantity of silver or gold, it formally adopted the gold standard in 1900, and finally eliminated all links to gold in 1971.

A Demand Note is a type of United States paper money that was issued from August 1861 to April 1862 during the American Civil War in denominations of 5, 10, and 20 US$. Demand Notes were the first issue of paper money by the United States that achieved wide circulation. The U.S. government placed Demand Notes into circulation by using them to pay expenses incurred during the Civil War including the salaries of its workers and military personnel.

The Refunding Certificate was a type of interest-bearing banknote that the United States Treasury issued in 1879. They issued it only in the $10 denomination, depicting Benjamin Franklin. Their issuance reflects the end of a coin-hoarding period that began during the American Civil War, and represented a return to public confidence in paper money.

Fractional currency, also referred to as shinplasters, was introduced by the United States federal government following the outbreak of the Civil War. These low-denomination banknotes of the United States dollar were in use between August 21, 1862, and February 15, 1876, and issued in denominations of 3, 5, 10, 15, 25, and 50 cents across five issuing periods. The complete type set below is part of the National Numismatic Collection, housed at the National Museum of American History, part of the Smithsonian Institution.

The Legal Tender Cases were two 1871 United States Supreme Court cases that affirmed the constitutionality of paper money. The two cases were Knox v. Lee and Parker v. Davis.

Greenbacks were emergency paper currency issued by the United States during the American Civil War that were printed in green on the back. They were in two forms: Demand Notes, issued in 1861–1862, and United States Notes, issued in 1862–1865. A form of fiat money, the notes were legal tender for most purposes and carried varying promises of eventual payment in coin but were not backed by existing gold or silver reserves.

The United States dollar is the official currency of the United States and several other countries. The Coinage Act of 1792 introduced the U.S. dollar at par with the Spanish silver dollar, divided it into 100 cents, and authorized the minting of coins denominated in dollars and cents. U.S. banknotes are issued in the form of Federal Reserve Notes, popularly called greenbacks due to their predominantly green color.

Morgan v. United States, 113 U.S. 476 (1885), was a case involving several judgments of the United States Court of Claims in four cases against the United States for the payment of United States bonds known as "five-twenty bonds."

Bills of credit are documents similar to banknotes issued by a government that represent a government's indebtedness to the holder. They are typically designed to circulate as currency or currency substitutes. Bills of credit are mentioned in Article One, Section 10, Clause One of the United States Constitution, where their issuance by state governments is prohibited.

From 1775 to 1779, the Continental Congress issued Continental currency banknotes. Then there was a period when the United States just used gold and silver, rather than paper currency. In 1812, the US began issuing Treasury Notes, although the motivation behind their issuance was funding federal expenditures rather than the provision of a circulating medium. In 1861, the US began issuing Demand Notes, which were the first paper money issued by the United States whose main purpose was to circulate. And since 1914, the US has issued Federal Reserve Notes.

References

↑ Cuhaj, George S.; Brandimore, William (2008). Standard Catalog of United States Paper Money, 27th edition, Iola, Wisconsin: Krause Publications. ISBN0-89689-707-9.

1 2 Hessler, Gene and Chambliss, Carlson (2006). The Comprehensive Catalog of U.S. Paper Money, 7th edition, Port Clinton, Ohio: BNR Press ISBN0-931960-66-5.

↑ Coins of 1861 Controlled by the South, R.W. Julian, "Numismatic News", December 03, 2008.

↑ The Continental Dollar: What Happened to it after 1779?, Farley Grubb, NBER Working Paper No. W13770, February 2008.

1 2 Studenski, Paul; Krooss, Hermand Edward (1952). Financial History of the United States, New York, NY: McGraw-Hill. ISBN1-58798-175-0.

↑ United States Notes, John Joseph Lalor, "Cyclopaedia of Political Science, Political Economy, and of the Political History of the United States", Rand McNally & Co, Chicago, 1881.

↑ Friedberg, Arthur L. and Ira S. The Official RED BOOK A Guide Book of United States Paper Money, Whitman Publishing, Atlanta, Georgia, 2008 ISBN0-7948-2362-9.

↑ Timberlake, Richard H. (1993) "Monetary Policy in the United States", Chicago, IL: University of Chicago Press. ISBN0-226-80384-8.

1 2 3 Mitchell, Wesley Clair, "A History of the Greenbacks With Special Reference To the Economic Consequences of Their Issue 1862-65", University of Chicago, Chicago, 1903.

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.