Macroeconomics is a branch of economics that deals with the performance, structure, behavior, and decision-making of an economy as a whole. This includes national, regional, and global economies. Macroeconomists study topics such as output/GDP and national income, unemployment, price indices and inflation, consumption, saving, investment, energy, international trade, and international finance.

In economics, deflation is a decrease in the general price level of goods and services. Deflation occurs when the inflation rate falls below 0%. Inflation reduces the value of currency over time, but deflation increases it. This allows more goods and services to be bought than before with the same amount of currency. Deflation is distinct from disinflation, a slowdown in the inflation rate; i.e., when inflation declines to a lower rate but is still positive.

Monetary policy is the policy adopted by the monetary authority of a nation to affect monetary and other financial conditions to accomplish broader objectives like high employment and price stability. Further purposes of a monetary policy may be to contribute to economic stability or to maintain predictable exchange rates with other currencies. Today most central banks in developed countries conduct their monetary policy within an inflation targeting framework, whereas the monetary policies of most developing countries' central banks target some kind of a fixed exchange rate system. A third monetary policy strategy, targeting the money supply, was widely followed during the 1980s, but has diminished in popularity since then, though it is still the official strategy in a number of emerging economies.

Zero interest-rate policy (ZIRP) is a macroeconomic concept describing conditions with a very low nominal interest rate, such as those in contemporary Japan and in the United States from December 2008 through December 2015 and again from March 2020 until March 2022 amid the COVID-19 pandemic. ZIRP is considered to be an unconventional monetary policy instrument and can be associated with slow economic growth, deflation and deleverage.

The causes of the Great Depression in the early 20th century in the United States have been extensively discussed by economists and remain a matter of active debate. They are part of the larger debate about economic crises and recessions. The specific economic events that took place during the Great Depression are well established.

Janet Louise Yellen is an American economist serving as the 78th United States secretary of the treasury since January 26, 2021. She previously served as the 15th chair of the Federal Reserve from 2014 to 2018. She is the first woman to hold either post, and has also led the White House Council of Economic Advisers. Yellen is the Eugene E. and Catherine M. Trefethen Professor of Business Administration and Economics at the University of California, Berkeley.

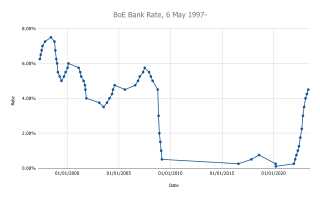

The Monetary Policy Committee (MPC) is a committee of the Bank of England, which meets for three and a half days, eight times a year, to decide the official interest rate in the United Kingdom.

Ben Shalom Bernanke is an American economist who served as the 14th chairman of the Federal Reserve from 2006 to 2014. After leaving the Federal Reserve, he was appointed a distinguished fellow at the Brookings Institution. During his tenure as chairman, Bernanke oversaw the Federal Reserve's response to the 2007–2008 financial crisis, for which he was named the 2009 Time Person of the Year. Before becoming Federal Reserve chairman, Bernanke was a tenured professor at Princeton University and chaired the Department of Economics there from 1996 to September 2002, when he went on public service leave. Bernanke was awarded the 2022 Nobel Memorial Prize in Economic Sciences, jointly with Douglas Diamond and Philip H. Dybvig, "for research on banks and financial crises", more specifically for his analysis of the Great Depression.

In macroeconomics, inflation targeting is a monetary policy where a central bank follows an explicit target for the inflation rate for the medium-term and announces this inflation target to the public. The assumption is that the best that monetary policy can do to support long-term growth of the economy is to maintain price stability, and price stability is achieved by controlling inflation. The central bank uses interest rates as its main short-term monetary instrument.

The Bank of Canada is a Crown corporation and Canada's central bank. Chartered in 1934 under the Bank of Canada Act, it is responsible for formulating Canada's monetary policy, and for the promotion of a safe and sound financial system within Canada. The Bank of Canada is the sole issuing authority of Canadian banknotes, provides banking services and money management for the government, and loans money to Canadian financial institutions. The contract to produce the banknotes has been held by the Canadian Bank Note Company since 1935.

Quantitative easing (QE) is a monetary policy action where a central bank purchases predetermined amounts of government bonds or other financial assets in order to stimulate economic activity. Quantitative easing is a novel form of monetary policy that came into wide application after the 2007–2008 financial crisis. It is used to mitigate an economic recession when inflation is very low or negative, making standard monetary policy ineffective. Quantitative tightening (QT) does the opposite, where for monetary policy reasons, a central bank sells off some portion of its holdings of government bonds or other financial assets.

The Greenspan put was a monetary policy response to financial crises that Alan Greenspan, former chair of the Federal Reserve, exercised beginning with the crash of 1987. Successful in addressing various crises, it became controversial as it led to periods of extreme speculation led by Wall Street investment banks overusing the put's repurchase agreements and creating successive asset price bubbles. The banks so overused Greenspan's tools that their compromised solvency in the 2007–2008 financial crisis required Fed chair Ben Bernanke to use direct quantitative easing. The term Yellen put was used to refer to Fed chair Janet Yellen's policy of perpetual monetary looseness.

James Brian Bullard is the former chief executive officer and 12th president of the Federal Reserve Bank of St. Louis, a position he held from 2008 until August 14, 2023. In July 2023, he was named dean of the Mitchell E. Daniels Jr. School of Business at Purdue University.

The Lost Decades are a lengthy period of economic stagnation in Japan precipitated by the asset price bubble's collapse beginning in 1990. The singular term Lost Decade originally referred to the 1990s, but the 2000s and the 2010s have been included by commentators as the phenomenon continued.

Narayana Rao Kocherlakota is an American economist and the Lionel W. McKenzie Professor of Economics at the University of Rochester. Previously, he served as the 12th president of the Federal Reserve Bank of Minneapolis until December 31, 2015. Appointed in 2009, he joined the Federal Open Markets Committee in 2011. In 2012, he was named one of the top 100 Global Thinkers by Foreign Policy magazine.

Negative interest on excess reserves is an instrument of unconventional monetary policy applied by central banks to encourage lending by making it costly for commercial banks to hold their excess reserves at central banks so they will lend more readily to the private sector. Such a policy is usually a response to very slow economic growth, deflation, and deleveraging.

Marvin Seth Goodfriend was an American economist. He held the Allan H. Meltzer Professorship in economics at Carnegie Mellon University; he was previously the director of research at the Federal Reserve Bank of Richmond. Following his 2017 nomination to the Federal Reserve Board of Governors, the White House decided to forgo renominating Goodfriend at the beginning of the new term.

Quantitative tightening (QT) is a contractionary monetary policy tool applied by central banks to decrease the amount of liquidity or money supply in the economy. A central bank implements quantitative tightening by reducing the financial assets it holds on its balance sheet by selling them into the financial markets, which decreases asset prices and raises interest rates. QT is the reverse of quantitative easing, where the central bank prints money and uses it to buy assets in order to raise asset prices and stimulate the economy. QT is rarely used by central banks, and has only been employed after prolonged periods of Greenspan put-type stimulus, where the creation of too much central banking liquidity has led to a risk of uncontrolled inflation.

A distributional effect is the effect of the redistribution of the final gains and costs derived from the direct gains and cost allocations of a project. A project has a direct-profit redistribution effect and a direct-cost redistribution effect. But whether it is profit or cost, the redistribution effect can be expressed as a benefit to a group of people or department or region, and the loss to another party. In theory, the indirect profit and indirect costs can also be derived from the redistribution effect, and valued.

The expression "everything bubble" refers to the correlated impact of monetary easing by the Federal Reserve on asset prices in most asset classes, namely equities, housing, bonds, many commodities, and even exotic assets such as cryptocurrencies and SPACs. The policy itself and the techniques of direct and indirect methods of quantitative easing used to execute it are sometimes referred to as the Fed put. Modern monetary theory advocates the use of such tools, even in non-crisis periods, to create economic growth through asset price inflation. The term "everything bubble" first came in use during the chair of Janet Yellen, but it is most associated with the subsequent chair of Jerome Powell, and the 2020–2021 period of the coronavirus pandemic.