Related Research Articles

In finance, a derivative is a contract that derives its value from the performance of an underlying entity. This underlying entity can be an asset, index, or interest rate, and is often simply called the "underlying". Derivatives can be used for a number of purposes, including insuring against price movements (hedging), increasing exposure to price movements for speculation, or getting access to otherwise hard-to-trade assets or markets. Some of the more common derivatives include forwards, futures, options, swaps, and variations of these such as synthetic collateralized debt obligations and credit default swaps. Most derivatives are traded over-the-counter (off-exchange) or on an exchange such as the Chicago Mercantile Exchange, while most insurance contracts have developed into a separate industry. In the United States, after the financial crisis of 2007–2009, there has been increased pressure to move derivatives to trade on exchanges.

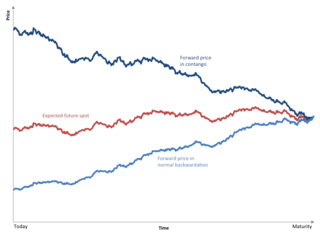

Contango is a situation where the futures price of a commodity is higher than the expected spot price of the contract at maturity. In a contango situation, arbitrageurs or speculators are "willing to pay more [now] for a commodity [to be received] at some point in the future than the actual expected price of the commodity [at that future point]. This may be due to people's desire to pay a premium to have the commodity in the future rather than paying the costs of storage and carry costs of buying the commodity today." On the other side of the trade, hedgers are happy to sell futures contracts and accept the higher-than-expected returns. A contango market is also known as a normal market, or carrying-cost market.

In finance, an interest rate swap (IRS) is an interest rate derivative (IRD). It involves exchange of interest rates between two parties. In particular it is a "linear" IRD and one of the most liquid, benchmark products. It has associations with forward rate agreements (FRAs), and with zero coupon swaps (ZCSs).

In finance, a futures contract is a standardized legal contract to buy or sell something at a predetermined price for delivery at a specified time in the future, between parties not yet known to each other. The asset transacted is usually a commodity or financial instrument. The predetermined price of the contract is known as the forward price. The specified time in the future when delivery and payment occur is known as the delivery date. Because it derives its value from the value of the underlying asset, a futures contract is a derivative.

In finance, a forward contract or simply a forward is a non-standardized contract between two parties to buy or sell an asset at a specified future time at a price agreed on at the time of conclusion of the contract, making it a type of derivative instrument. The party agreeing to buy the underlying asset in the future assumes a long position, and the party agreeing to sell the asset in the future assumes a short position. The price agreed upon is called the delivery price, which is equal to the forward price at the time the contract is entered into.

A hedge is an investment position intended to offset potential losses or gains that may be incurred by a companion investment. A hedge can be constructed from many types of financial instruments, including stocks, exchange-traded funds, insurance, forward contracts, swaps, options, gambles, many types of over-the-counter and derivative products, and futures contracts.

A swaption is an option granting its owner the right but not the obligation to enter into an underlying swap. Although options can be traded on a variety of swaps, the term "swaption" typically refers to options on interest rate swaps.

In finance, a swap is an agreement between two counterparties to exchange financial instruments or cashflows or payments for a certain time. The instruments can be almost anything but most swaps involve cash based on a notional principal amount.

An equity swap is a financial derivative contract where a set of future cash flows are agreed to be exchanged between two counterparties at set dates in the future. The two cash flows are usually referred to as "legs" of the swap; one of these "legs" is usually pegged to a floating rate such as LIBOR. This leg is also commonly referred to as the "floating leg". The other leg of the swap is based on the performance of either a share of stock or a stock market index. This leg is commonly referred to as the "equity leg". Most equity swaps involve a floating leg vs. an equity leg, although some exist with two equity legs.

Rational pricing is the assumption in financial economics that asset prices - and hence asset pricing models - will reflect the arbitrage-free price of the asset as any deviation from this price will be "arbitraged away". This assumption is useful in pricing fixed income securities, particularly bonds, and is fundamental to the pricing of derivative instruments.

Floating rate notes (FRNs) are bonds that have a variable coupon, equal to a money market reference rate, like LIBOR or federal funds rate, plus a quoted spread. The spread is a rate that remains constant. Almost all FRNs have quarterly coupons, i.e. they pay out interest every three months. At the beginning of each coupon period, the coupon is calculated by taking the fixing of the reference rate for that day and adding the spread. A typical coupon would look like 3 months USD LIBOR +0.20%.

Fixed-income arbitrage is a group of market-neutral-investment strategies that are designed to take advantage of differences in interest rates between varying fixed-income securities or contracts. Arbitrage in terms of investment strategy, involves buying securities on one market for immediate resale on another market in order to profit from a price discrepancy.

A quanto is a type of derivative in which the underlying is denominated in one currency, but the instrument itself is settled in another currency at some rate. Such products are attractive for speculators and investors who wish to have exposure to a foreign asset, but without the corresponding exchange rate risk.

A structured product, also known as a market-linked investment, is a pre-packaged structured finance investment strategy based on a single security, a basket of securities, options, indices, commodities, debt issuance or foreign currencies, and to a lesser extent, derivatives. Structured products are not homogeneous — there are numerous varieties of derivatives and underlying assets — but they can be classified under the aside categories. Typically, a desk will employ a specialized "structurer" to design and manage its structured-product offering.

In finance, a currency swap is an interest rate derivative (IRD). In particular it is a linear IRD, and one of the most liquid benchmark products spanning multiple currencies simultaneously. It has pricing associations with interest rate swaps (IRSs), foreign exchange (FX) rates, and FX swaps (FXSs).

An energy derivative is a derivative contract based on an underlying energy asset, such as natural gas, crude oil, or electricity. Energy derivatives are exotic derivatives and include exchange-traded contracts such as futures and options, and over-the-counter derivatives such as forwards, swaps and options. Major players in the energy derivative markets include major trading houses, oil companies, utilities, and financial institutions.

In finance, a spread trade is the simultaneous purchase of one security and sale of a related security, called legs, as a unit. Spread trades are usually executed with options or futures contracts as the legs, but other securities are sometimes used. They are executed to yield an overall net position whose value, called the spread, depends on the difference between the prices of the legs. Common spreads are priced and traded as a unit on futures exchanges rather than as individual legs, thus ensuring simultaneous execution and eliminating the execution risk of one leg executing but the other failing.

An asset swap refers to an exchange of tangible for intangible assets, in accountancy, or, in finance, to the exchange of the flow of payments from a given security for a different set of cash flows.

In finance, a zero coupon swap (ZCS) is an interest rate derivative (IRD). In particular it is a linear IRD, that in its specification is very similar to the much more widely traded interest rate swap (IRS).

The Islamic banking and finance movement that developed in the late 20th century as part of the revival of Islamic identity sought to create an alternative to conventional banking that complied with sharia (Islamic) law. Following sharia it banned from its practices riba (usury) – which it defined as any interest paid on all loans of money – and involvement in haram (forbidden) goods or services such as pork or alcohol. It also forbids gambling (maisir) and excessive risk.

References

- ↑ "Understanding Derivatives: Markets and Infrastructure". Federal Reserve Bank of Chicago, Financial Markets Group.

- ↑ Staff, Investopedia (2003-11-23). "Interest Rate Swap". Investopedia. Retrieved 2018-10-20.

- ↑ "Understanding Interest Rate Swaps | PIMCO". Pacific Investment Management Company LLC. Retrieved 2018-10-20.

| | This economic term article is a stub. You can help Wikipedia by expanding it. |