Related Research Articles

In finance, being short in an asset means investing in such a way that the investor will profit if the value of the asset falls. This is the opposite of a more conventional "long" position, where the investor will profit if the value of the asset rises.

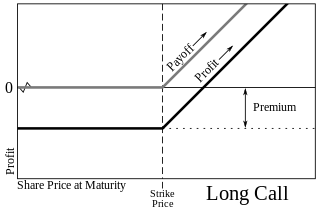

In finance, a call option, often simply labeled a "call", is a contract between the buyer and the seller of the call option to exchange a security at a set price. The buyer of the call option has the right, but not the obligation, to buy an agreed quantity of a particular commodity or financial instrument from the seller of the option at or before a certain time for a certain price. This effectively gives the owner a long position in the given asset. The seller is obliged to sell the commodity or financial instrument to the buyer if the buyer so decides. This effectively gives the seller a short position in the given asset. The buyer pays a fee for this right. The term "call" comes from the fact that the owner has the right to "call the stock away" from the seller.

In finance, a put or put option is a derivative instrument in financial markets that gives the holder the right to sell an asset, at a specified price, by a specified date to the writer of the put. The purchase of a put option is interpreted as a negative sentiment about the future value of the underlying stock. The term "put" comes from the fact that the owner has the right to "put up for sale" the stock or index.

In finance, a warrant is a security that entitles the holder to buy or sell stock, typically the stock of the issuing company, at a fixed price called the exercise price.

In finance, the style or family of an option is the class into which the option falls, usually defined by the dates on which the option may be exercised. The vast majority of options are either European or American (style) options. These options—as well as others where the payoff is calculated similarly—are referred to as "vanilla options". Options where the payoff is calculated differently are categorized as "exotic options". Exotic options can pose challenging problems in valuation and hedging.

In finance, the strike price of an option is a fixed price at which the owner of the option can buy, or sell, the underlying security or commodity. The strike price may be set by reference to the spot price, which is the market price of the underlying security or commodity on the day an option is taken out. Alternatively, the strike price may be fixed at a discount or premium.

In finance, a futures contract is a standardized legal contract to buy or sell something at a predetermined price for delivery at a specified time in the future, between parties not yet known to each other. The asset transacted is usually a commodity or financial instrument. The predetermined price of the contract is known as the forward price. The specified time in the future when delivery and payment occur is known as the delivery date. Because it derives its value from the value of the underlying asset, a futures contract is a derivative.

In finance, an equity derivative is a class of derivatives whose value is at least partly derived from one or more underlying equity securities. Options and futures are by far the most common equity derivatives, however there are many other types of equity derivatives that are actively traded.

A swaption is an option granting its owner the right but not the obligation to enter into an underlying swap. Although options can be traded on a variety of swaps, the term "swaption" typically refers to options on interest rate swaps.

Employee stock options (ESO) is a label that refers to compensation contracts between an employer and an employee that carries some characteristics of financial options.

A rights issue or rights offer is a dividend of subscription rights to buy additional securities in a company made to the company's existing security holders. When the rights are for equity securities, such as shares, in a public company, it can be a non-dilutive pro rata way to raise capital. Rights issues are typically sold via a prospectus or prospectus supplement. With the issued rights, existing security-holders have the privilege to buy a specified number of new securities from the issuer at a specified price within a subscription period. In a public company, a rights issue is a form of public offering.

In finance, the intrinsic value of an asset or security is its value as calculated with regard to an inherent, objective measure; this is in distinction to its price, which is determined relative to other similar assets.

A barrier option is an option whose payoff is conditional upon the underlying asset's price breaching a barrier level during the option's lifetime.

An energy derivative is a derivative contract based on an underlying energy asset, such as natural gas, crude oil, or electricity. Energy derivatives are exotic derivatives and include exchange-traded contracts such as futures and options, and over-the-counter derivatives such as forwards, swaps and options. Major players in the energy derivative markets include major trading houses, oil companies, utilities, and financial institutions.

In finance, a price (premium) is paid or received for purchasing or selling options. This article discusses the calculation of this premium in general. For further detail, see: Mathematical finance § Derivatives pricing: the Q world for discussion of the mathematics; Financial engineering for the implementation; as well as Financial modeling § Quantitative finance generally.

In finance, the expiration date of an option contract is the last date on which the holder of the option may exercise it according to its terms. In the case of options with "automatic exercise", the net value of the option is credited to the long and debited to the short position holders.

Pin risk occurs when the market price of the underlier of an option contract at the time of the contract's expiration is close to the option's strike price. In this situation, the underlier is said to have pinned. The risk to the writer (seller) of the option is that they cannot predict with certainty whether the option will be exercised or not. So the writer cannot hedge their position precisely and may end up with a loss or gain. There is a chance that the price of the underlier may move adversely, resulting in an unanticipated loss to the writer. In other words, an option position may result in a large, undesired risky position in the underlier immediately after expiration, regardless of the actions of the writer.

In finance, an option is a contract which conveys to its owner, the holder, the right, but not the obligation, to buy or sell a specific quantity of an underlying asset or instrument at a specified strike price on or before a specified date, depending on the style of the option. Options are typically acquired by purchase, as a form of compensation, or as part of a complex financial transaction. Thus, they are also a form of asset and have a valuation that may depend on a complex relationship between underlying asset price, time until expiration, market volatility, the risk-free rate of interest, and the strike price of the option. Options may be traded between private parties in over-the-counter (OTC) transactions, or they may be exchange-traded in live, public markets in the form of standardized contracts.

OneChicago was a US-based all-electronic futures exchange with headquarters in Chicago, Illinois. The exchange offered approximately 12,509 single-stock futures (SSF) products with names such as IBM, Apple and Google. All trading was cleared through Options Clearing Corporation (OCC). The OneChicago exchange closed in September 2020.

In finance, a perpetual futures contract, also known as a perpetual swap, is an agreement to non-optionally buy or sell an asset at an unspecified point in the future. Perpetual futures are cash-settled, and differ from regular futures in that they lack a pre-specified delivery date, and can thus be held indefinitely without the need to roll over contracts as they approach expiration. Payments are periodically exchanged between holders of the two sides of the contracts, long and short, with the direction and magnitude of the settlement based on the difference between the contract price and that of the underlying asset, as well as, if applicable, the difference in leverage between the two sides.

References

- ↑ "Characteristics and Risks of Standardized Options" (PDF). Options Clearing Corporation. Retrieved 2007-06-21.

- ↑ "Options Settlement – How Options Contracts Are Settled". www.optionstrading.org. Retrieved 2017-01-05.

- ↑ John C. Hull (2002). Options, Futures and Other Derivatives, 5th edition . Prentice Hall. p. 744. ISBN 0-13-009056-5.

- ↑ "OCC Infomemo #30048: Underlying Prices for Expiration" Accessed Jan 21, 2012