International Financial Reporting Standards, commonly called IFRS, are accounting standards issued by the IFRS Foundation and the International Accounting Standards Board (IASB). They constitute a standardised way of describing the company's financial performance and position so that company financial statements are understandable and comparable across international boundaries. They are particularly relevant for companies with shares or securities publicly listed.

Generally Accepted Accounting Practice in the UK, or UK GAAP or GAAP (UK), is the overall body of regulation establishing how company accounts must be prepared in the United Kingdom. Company accounts must also be prepared in accordance with applicable company law (for UK companies, the Companies Act 2006; for companies in the Channel Islands and the Isle of Man, companies law applicable to those jurisdictions).

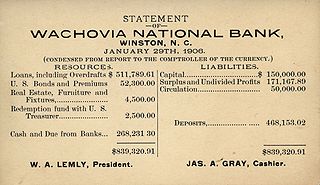

Financial statements are formal records of the financial activities and position of a business, person, or other entity.

Publicly traded companies typically are subject to rigorous standards. Small and midsized businesses often follow more simplified standards, plus any specific disclosures required by their specific lenders and shareholders. Some firms operate on the cash method of accounting which can often be simple and straightforward. Larger firms most often operate on an accrual basis. Accrual basis is one of the fundamental accounting assumptions and if it is followed by the company while preparing the Financial statements then no further disclosure is required. Accounting standards prescribe in considerable detail what accruals must be made, how the financial statements are to be presented, and what additional disclosures are required.

The Securities and Exchange Board of India (SEBI) is the regulatory body for securities and commodity market in India under the administrative domain of Ministry of Finance within the Government of India. It was established on 12 April 1988 as an executive body and was given statutory powers on 30 January 1992 through the SEBI Act, 1992.

The Institute of Chartered Accountants of India, abbreviated as ICAI, is India's largest professional accounting body under the administrative control of Ministry of Corporate Affairs, Government of India. It was established on 1 July 1949 as a statutory body under the Chartered Accountants Act, 1949 enacted by the Parliament for promotion, development and regulation of the profession of Chartered Accountancy in India.

The Global Reporting Initiative is an international independent standards organization that helps businesses, governments, and other organizations understand and communicate their impacts on issues such as climate change, human rights, and corruption.

The CDP is an international non-profit organisation based in the United Kingdom, Japan, India, China, Germany, Brazil and the United States that helps companies, cities, states, regions and public authorities disclose their environmental impact. It aims to make environmental reporting and risk management a business norm, driving disclosure, insight, and action towards a sustainable economy. In 2022, nearly 18,700 organizations disclosed their environmental information through CDP.

The Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR) is hosted by the United Nations Conference on Trade and Development (UNCTAD). Created in 1982 by the United Nations Economic and Social Council (ECOSOC), its mission is to facilitate investment, development and economic stability by promoting good practices in corporate transparency and accounting.

The Limited Liability Partnership Act, 2008 was enacted by the Parliament of India to introduce and legally sanction the concept of LLP in India. Unlike the general partnerships in India, LLP is a body corporate and legal entity separate from its partners, have Perpetual succession and any change in the partners of an LLP shall not affect the existence, rights or liabilities of the LLP.

The Climate Disclosure Standards Board (CDSB) is a non-profit organization working to provide material information for investors and financial markets through the integration of climate change-related information into mainstream financial reporting. CDSB operates on the premise that investors and financial institutions can make better and informed decisions if companies are open, transparent and analyse the risks and opportunities associated with climate change-related information. To this end, CDSB acts as a forum for collaboration on how existing standards and practices can be used to link financial and climate change-related information using its Framework for reporting environmental information, natural capital and associated business impacts.

The Indian Corporate Law Service (Hindi: भारतीय कॉरपोरेट विधि सेवा), abbreviated as ICLS, is one of the Central Civil Services and it functions under the Ministry of Corporate Affairs, Government of India. The service is entrusted with the responsibility of the implementation of Companies Act,1956(now repealed), Companies Act, 2013 and The Limited liability Partnership Act, 2008.

India's National Voluntary Guidelines on Social, Environmental and Economic Responsibilities of Business (NVGs) were released by the Ministry of Corporate Affairs (MCA) in July 2011 by Mr. Murli Deora, the former Honourable Minister for Corporate Affairs. The national framework on Business Responsibility is essentially a set of nine principles that offer businesses an Indian understanding and approach to inculcating responsible business conduct.

The Companies Act 2013 is an Act of the Parliament of India which forms the primary source of Indian company law. It received presidential assent on 29 August 2013, and largely superseded the Companies Act 1956.

Small finance banks (SFB) are a type of niche banks in India. Banks with a SFB license can provide basic banking service of acceptance of deposits and lending. The aim behind these is to provide financial inclusion to sections of the economy not being served by other banks, such as small business units, small and marginal farmers, micro and small industries and unorganised sector entities.

Auditing in India is a system of independently reviewing the records/activities and expressing an opinion thereon.

The Pradhan Mantri fasal bima yojana (PMFBY) launched on 18 February 2016 by Prime Minister Narendra Modi is an insurance service for farmers for their yields. It was formulated in line with One Nation–One Scheme theme by replacing earlier two schemes Agricultural insurance in India#National Agriculture Insurance Scheme and Modified National Agricultural Insurance Scheme by incorporating their best features and removing their inherent drawbacks (shortcomings). It aims to reduce the premium burden on farmers and ensure early settlement of crop assurance claim for the full insured sum.

Income Computation and Disclosure Standards (ICDS) were issued by the Government of India in exercise of powers conferred to it under section 145(2) of The Income Tax Act, 1961.

Narain Dass Gupta is Member of Parliament Rajya Sabha from NCT of Delhi, practicing chartered accountant, and former president of the Institute of Chartered Accountants of India (ICAI). He is a financial policy expert who has written several books on taxation.

The Task Force on Climate Related Financial Disclosures (TCFD) provides information to investors about what companies are doing to mitigate the risks of climate change, as well as be transparent about the way in which they are governed. It was established in December 2015 by the Group of 20 (G20) and the Financial Stability Board (FSB), and is chaired by Michael Bloomberg. It consists of governance, strategy, risk management, and metrics and targets. It will become mandatory for companies to report on these disclosures by 2025 in the UK, although some companies will have to report earlier.