International Financial Reporting Standards, commonly called IFRS, are accounting standards issued by the IFRS Foundation and the International Accounting Standards Board (IASB). They constitute a standardised way of describing the company's financial performance and position so that company financial statements are understandable and comparable across international boundaries. They are particularly relevant for companies with shares or securities publicly listed.

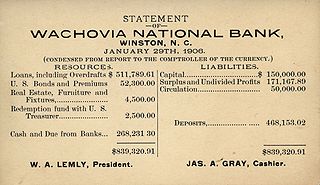

Financial statements are formal records of the financial activities and position of a business, person, or other entity.

Financial instruments are monetary contracts between parties. They can be created, traded, modified and settled. They can be cash (currency), evidence of an ownership interest in an entity or a contractual right to receive or deliver in the form of currency (forex); debt ; equity (shares); or derivatives.

In accounting, fair value is a rational and unbiased estimate of the potential market price of a good, service, or asset. The derivation takes into account such objective factors as the costs associated with production or replacement, market conditions and matters of supply and demand. Subjective factors may also be considered such as the risk characteristics, the cost of and return on capital, and individually perceived utility.

(CCE) are the most liquid current assets found on a business's balance sheet. Cash equivalents are short-term commitments "with temporarily idle cash and easily convertible into a known cash amount". An investment normally counts as a cash equivalent when it has a short maturity period of 90 days or less, and can be included in the cash and cash equivalents balance from the date of acquisition when it carries an insignificant risk of changes in the asset value. If it has a maturity of more than 90 days, it is not considered a cash equivalent. Equity investments mostly are excluded from cash equivalents, unless they are essentially cash equivalents.

Financial risk management is the practice of protecting economic value in a firm by managing exposure to financial risk - principally credit risk and market risk, with more specific variants as listed aside - as well as some aspects of operational risk. As for risk management more generally, financial risk management requires identifying the sources of risk, measuring these, and crafting plans to mitigate them. See Finance § Risk management for an overview.

A finance lease is a type of lease in which a finance company is typically the legal owner of the asset for the duration of the lease, while the lessee not only has operating control over the asset but also some share of the economic risks and returns from the change in the valuation of the underlying asset.

The following outline is provided as an overview of and topical guide to finance:

Hedge accounting is an accountancy practice, the aim of which is to provide an offset to the mark-to-market movement of the derivative in the profit and loss account.

Launched prior to the millennium, FAS 133 Accounting for Derivative Instruments and Hedging Activities provided an "integrated accounting framework for derivative instruments and hedging activities."

A financial asset is a non-physical asset whose value is derived from a contractual claim, such as bank deposits, bonds, and participations in companies' share capital. Financial assets are usually more liquid than tangible assets, such as commodities or real estate.

A foreign exchange hedge is a method used by companies to eliminate or "hedge" their foreign exchange risk resulting from transactions in foreign currencies. This is done using either the cash flow hedge or the fair value method. The accounting rules for this are addressed by both the International Financial Reporting Standards (IFRS) and by the US Generally Accepted Accounting Principles as well as other national accounting standards.

IAS 39: Financial Instruments: Recognition and Measurement was an international accounting standard which outlined the requirements for the recognition and measurement of financial assets, financial liabilities, and some contracts to buy or sell non-financial items. It was released by the International Accounting Standards Board (IASB) in 2003, and was replaced in 2014 by IFRS 9, which became effective in 2018.

The accounting term Hedge relationship relates to the treatment of an insurance contract for risk mitigation on an underlying asset, and the set of tests for the valuation of this insurer/insuree contract. More specifically, "Hedge relationship" describes the criteria for including the fair value of derivatives on balance sheet as part of an effort to regulate and normalize the use of hedging in corporate accounting.

Impairment of assets is the diminishing in quality, strength, amount, or value of an asset. An impairment cost must be included under expenses when the book value of an asset exceeds the recoverable amount. Fixed assets, commonly known as PPE, refers to long-lived assets such as buildings, land, machinery, and equipment; these assets are the most likely to experience impairment, which may be caused by several factors.

Russian Accounting Standards (RAS; Russian: Российские стандарты бухгалтерского учёта, РСБУ), also called Russian Accounting Principles (RAP) or Russian GAAP or GAAP (Russia), refer to the body of regulatory documents concerning financial accounting and reporting standards in the Russian Federation.

International Accounting Standard 16 Property, Plant and Equipment or IAS 16 is an international financial reporting standard adopted by the International Accounting Standards Board (IASB). It concerns accounting for property, plant and equipment, including recognition, determination of their carrying amounts, and the depreciation charges and impairment losses to be recognised in relation to them.

IFRS 9 is an International Financial Reporting Standard (IFRS) published by the International Accounting Standards Board (IASB). It addresses the accounting for financial instruments. It contains three main topics: classification and measurement of financial instruments, impairment of financial assets and hedge accounting. The standard came into force on 1 January 2018, replacing the earlier IFRS for financial instruments, IAS 39.

IFRS 4 is an International Financial Reporting Standard (IFRS) issued by the International Accounting Standards Board (IASB) providing guidance for the accounting of insurance contracts. The standard was issued in March 2004, and was amended in 2005 to clarify that the standard covers most financial guarantee contracts. Paragraph 35 of IFRS also applies the standard to financial instruments with discretionary participation features.

IFRS 7, titled Financial Instruments: Disclosures, is an International Financial Reporting Standard (IFRS) published by the International Accounting Standards Board (IASB). It requires entities to provide certain disclosures regarding financial instruments in their financial statements. The standard was originally issued in August 2005 and became applicable on 1 January 2007, superseding the earlier standard IAS 30, Disclosures in the Financial Statements of Banks and Similar Financial Institutions, and replacing the disclosure requirements of IAS 32, previously titled Financial Instruments: Disclosure and Presentation.