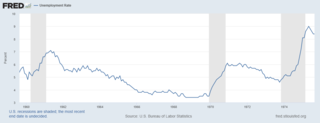

In economics, a recession is a business cycle contraction that occurs when there is a period of broad decline in economic activity. Recessions generally occur when there is a widespread drop in spending. This may be triggered by various events, such as a financial crisis, an external trade shock, an adverse supply shock, the bursting of an economic bubble, or a large-scale anthropogenic or natural disaster. There is no official definition of a recession, according to the IMF.

Monetarism is a school of thought in monetary economics that emphasizes the role of policy-makers in controlling the amount of money in circulation. It gained prominence in the 1970s but was mostly abandoned as a direct guidance to monetary policy during the following decade because of the rise of inflation targeting through movements of the official interest rate.

In economics, deflation is a decrease in the general price level of goods and services. Deflation occurs when the inflation rate falls below 0%. Inflation reduces the value of currency over time, but deflation increases it. This allows more goods and services to be bought than before with the same amount of currency. Deflation is distinct from disinflation, a slowdown in the inflation rate; i.e., when inflation declines to a lower rate but is still positive.

The monetary policy of the United States is the set of policies which the Federal Reserve follows to achieve its twin objectives of high employment and stable inflation.

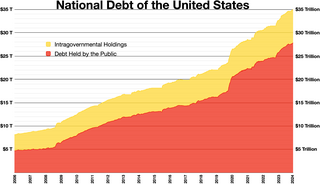

The national debt of the United States is the total national debt owed by the federal government of the United States to Treasury security holders. The national debt at any point in time is the face value of the then-outstanding Treasury securities that have been issued by the Treasury and other federal agencies. The terms "national deficit" and "national surplus" usually refer to the federal government budget balance from year to year, not the cumulative amount of debt. In a deficit year the national debt increases as the government needs to borrow funds to finance the deficit, while in a surplus year the debt decreases as more money is received than spent, enabling the government to reduce the debt by buying back some Treasury securities. In general, government debt increases as a result of government spending and decreases from tax or other receipts, both of which fluctuate during the course of a fiscal year. There are two components of gross national debt:

The causes of the Great Depression in the early 20th century in the United States have been extensively discussed by economists and remain a matter of active debate. They are part of the larger debate about economic crises and recessions. The specific economic events that took place during the Great Depression are well established.

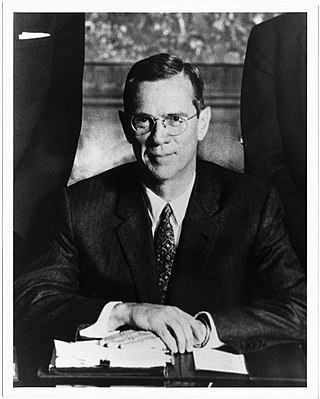

William McChesney Martin Jr. was an American business executive who served as the 9th chairman of the Federal Reserve from 1951 to 1970, making him the longest holder of that position. He was nominated to the post by President Harry S. Truman and reappointed by four of his successors. Martin, who once considered becoming a Presbyterian minister, was described by a Washington journalist as "the happy Puritan".

Arthur Frank Burns was an American economist and diplomat who served as the 10th chairman of the Federal Reserve from 1970 to 1978. He previously chaired the Council of Economic Advisers under President Dwight D. Eisenhower from 1953 to 1956, and served as the first Counselor to the President under Richard Nixon from January to November 1969. He also taught and researched at Rutgers University, Columbia University, and the National Bureau of Economic Research.

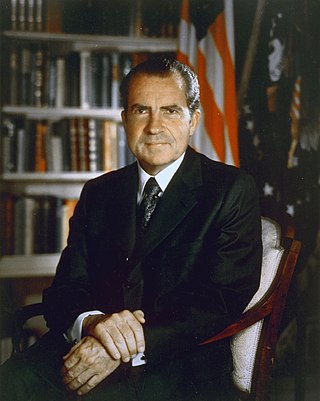

The Nixon shock was the effect of a series of economic measures, including wage and price freezes, surcharges on imports, and the unilateral cancellation of the direct international convertibility of the United States dollar to gold, taken by United States President Richard Nixon on 15th August 1971 in response to increasing inflation.

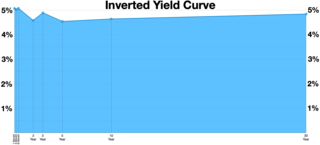

In finance, an inverted yield curve is a yield curve in which short-term debt instruments have a greater yield than longer term bonds. An inverted yield curve is an unusual phenomenon; bonds with shorter maturities generally provide lower yields than longer term bonds.

The recession of 1937–1938 was an economic downturn that occurred during the Great Depression in the United States.

The recession of 1958, also known as the Eisenhower Recession, was a sharp worldwide economic downturn in 1958. The effect of the recession spread beyond the United States to Europe and Canada, causing many businesses to shut down. Officially, recessionary circumstances lasted from the middle of 1957 to April 1958. Though it is generally regarded as a moderate recession, it was the most significant recession during the post–World War II economic expansion between 1945 and 1973.

The early 1980s recession was a severe economic recession that affected much of the world between approximately the start of 1980 and 1982. It is widely considered to have been the most severe recession since World War II until the 2007–2008 financial crisis.

The Depression of 1920–1921 was a sharp deflationary recession in the United States, United Kingdom and other countries, beginning 14 months after the end of World War I. It lasted from January 1920 to July 1921. The extent of the deflation was not only large, but large relative to the accompanying decline in real product.

The financial position of the United States includes assets of at least $269 trillion and debts of $145.8 trillion to produce a net worth of at least $123.8 trillion. GDP in 2014 Q1 decline was due to foreclosures and increased rates of household saving. There were significant declines in debt to GDP in each sector except the government, which ran large deficits to offset deleveraging or debt reduction in other sectors.

The recession of 1969–1970 was a relatively mild recession in the United States. According to the National Bureau of Economic Research, the recession lasted for 11 months, beginning in December 1969 and ending in November 1970. It followed an economic slump that began in 1968.

The recession of 1960–1961 was a recession in the United States. According to the National Bureau of Economic Research, the recession lasted for 10 months, beginning in April 1960 and ending in February 1961. The recession preceded the third-longest economic expansion in U.S. history, from February 1961 until the beginning of the recession of 1969–1970 in December 1968.

The United States entered recession in January 1980 and returned to growth 6 months later in July 1980. Although recovery took hold, the unemployment rate remained unchanged through the start of a second recession in July 1981. The downturn ended 16 months later, in November 1982. The economy entered a strong recovery and experienced a lengthy expansion through 1990.

David I. Meiselman was an American economist. Among his contributions to the field of economics are his work on the term structure of interest rates, the foundation today of the implementation of monetary policy by major central banks, and his work with Milton Friedman on the impact of monetary policy on the performance of the economy and inflation.