Related Research Articles

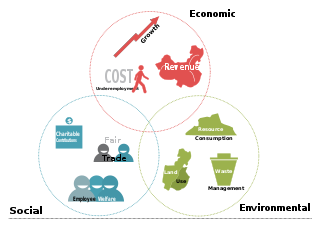

The triple bottom line is an accounting framework with three parts: social, environmental and economic. Some organizations have adopted the TBL framework to evaluate their performance in a broader perspective to create greater business value. Business writer John Elkington claims to have coined the phrase in 1994.

Corporate social responsibility (CSR) or corporate social impact is a form of international private business self-regulation which aims to contribute to societal goals of a philanthropic, activist, or charitable nature by engaging in, with, or supporting professional service volunteering through pro bono programs, community development, administering monetary grants to non-profit organizations for the public benefit, or to conduct ethically oriented business and investment practices. While once it was possible to describe CSR as an internal organizational policy or a corporate ethic strategy similar to what is now known today as Environmental, Social, Governance (ESG); that time has passed as various companies have pledged to go beyond that or have been mandated or incentivized by governments to have a better impact on the surrounding community. In addition national and international standards, laws, and business models have been developed to facilitate and incentivize this phenomenon. Various organizations have used their authority to push it beyond individual or even industry-wide initiatives. In contrast, it has been considered a form of corporate self-regulation for some time, over the last decade or so it has moved considerably from voluntary decisions at the level of individual organizations to mandatory schemes at regional, national, and international levels. Moreover, scholars and firms are using the term "creating shared value", an extension of corporate social responsibility, to explain ways of doing business in a socially responsible way while making profits.

Ayman Sawaf is a social commentator, film producer, entrepreneur, musician and author.

The Progressive utilization theory (PROUT) is a socioeconomic and political philosophy created by the Indian philosopher and spiritual leader Prabhat Ranjan Sarkar. He first conceived of PROUT in 1959. Its proponents (Proutists) claim that it exposes and overcomes the limitations of capitalism, communism and mixed economy. Since its genesis, PROUT has had an economically progressive approach, aiming to improve social development in the world. It is in line with Sarkar's Neohumanist values which aim to provide "proper care" to every being on the planet, including humans, animals and plants.

Spiritual ecology is an emerging field in religion, conservation, and academia that proposes that there is a spiritual facet to all issues related to conservation, environmentalism, and earth stewardship. Proponents of spiritual ecology assert a need for contemporary nature conservation work to include spiritual elements and for contemporary religion and spirituality to include awareness of and engagement in ecological issues.

Futurists are people whose specialty or interest is futurology or the attempt to systematically explore predictions and possibilities about the future and how they can emerge from the present, whether that of human society in particular or of life on Earth in general.

Double bottom line seeks to extend the conventional bottom line, which measures fiscal performance—financial profit or loss—by adding a second bottom line to measure a for-profit business's performance in terms of positive social impact. There is controversy about how to measure the double bottom line, especially since the use of the term "bottom line" implies some form of quantification. A 2004 report by the Center for Responsible Business noted that while there are "generally accepted principles of accounting" for financial returns, "A comparable standard for social impact accounting does not yet exist." Social return on investment has been suggested as a way to quantify the second bottom line, though defining and measuring social impact can prove elusive.

A sustainable business, or a green business, is an enterprise that has a minimal negative impact or potentially a positive effect on the global or local environment, community, society, or economy—a business that strives to meet the triple bottom line. They cluster under different groupings and the whole is sometimes referred to as "green capitalism." Often, sustainable businesses have progressive environmental and human rights policies. In general, a business is described as green if it matches the following four criteria:

- It incorporates principles of sustainability into each of its business decisions.

- It supplies environmentally friendly products or services that replace demand for nongreen products and/or services.

- It is greener than traditional competition.

- It has made an enduring commitment to environmental principles in its business operations.

An ethical bank, also known as a social, alternative, civic, or sustainable bank, is a bank concerned with the social and environmental impacts of its investments and loans. The ethical banking movement includes: ethical investment, impact investment, socially responsible investment, corporate social responsibility, and is also related to such movements as the fair trade movement, ethical consumerism, and social enterprise.

Workplace spirituality or spirituality in the workplace is a movement that began in the early 1920s. It emerged as a grassroots movement with individuals seeking to live their faith and/or spiritual values in the workplace. Spiritual or spirit-centered leadership is a topic of inquiry frequently associated with the workplace spirituality movement.

Corporate sustainability is an approach aiming to create long-term stakeholder value through the implementation of a business strategy that focuses on the ethical, social, environmental, cultural, and economic dimensions of doing business. The strategies created are intended to foster longevity, transparency, and proper employee development within business organizations. Firms will often express their commitment to corporate sustainability through a statement of Corporate Sustainability Standards (CSS), which are usually policies and measures that aim to meet, or exceed, minimum regulatory requirements.

John Elkington is an author, advisor and serial entrepreneur. He is an authority on corporate responsibility and sustainable development. He has written and co-authored 20 books, including the Green Consumer Guide, Cannibals with Forks: The Triple Bottom Line of 21st Century Business, The Power of Unreasonable People: How Social Entrepreneurs Create Markets That Change the World, and The Breakthrough Challenge: 10 Ways to Connect Tomorrow's Profits with Tomorrow's Bottom Line.

Sustainability accounting was originated about 20 years ago and is considered a subcategory of financial accounting that focuses on the disclosure of non-financial information about a firm's performance to external stakeholders, such as capital holders, creditors, and other authorities. Sustainability accounting represents the activities that have a direct impact on society, environment, and economic performance of an organisation. Sustainability accounting in managerial accounting contrasts with financial accounting in that managerial accounting is used for internal decision making and the creation of new policies that will have an effect on the organisation's performance at economic, ecological, and social level. Sustainability accounting is often used to generate value creation within an organisation.

Return on investment (ROI) or return on costs (ROC) is a ratio between net income and investment. A high ROI means the investment's gains compare favourably to its cost. As a performance measure, ROI is used to evaluate the efficiency of an investment or to compare the efficiencies of several different investments. In economic terms, it is one way of relating profits to capital invested.

Blended Value refers to an emerging conceptual framework in which non-profit organizations, businesses, and investments are evaluated based on their ability to generate a blend of financial, social, and environmental value. The term is usually attributed to Jed Emerson, and sometimes used interchangeably with triple bottom line. Blended value propositions are founded on the notion that value cannot be bifurcated, and is inherently made up of more than one measurement of performance. For example, under a blended value proposition, a for-profit business would consider their social and environmental impact on society alongside their financial performance measurement. Within the same context, non-profits would consider their financial efficiency and sustainability in tandem with their social and environmental performance. Blended value suggests the true measure of any organization is in its ability to holistically perform in all 3 areas.

A sustainability organization is (1) an organized group of people that aims to advance sustainability and/or (2) those actions of organizing something sustainably. Unlike many business organizations, sustainability organizations are not limited to implementing sustainability strategies which provide them with economic and cultural benefits attained through environmental responsibility. For sustainability organizations, sustainability can also be an end in itself without further justifications.

After Capitalism: Economic Democracy in Action is a 2012 book by United States author Dada Maheshvarananda, an activist, yoga monk and writer. The book argues that global capitalism is terminally ill because it suffers from four fatal flaws: growing inequity and concentration of wealth, addiction to speculation instead of production, rising unsustainable debt and its tendency to exploit the natural environment.

Conscious business enterprises and people are those that choose to follow a business strategy, in which they seek to benefit both human beings and the environment.

Causal layered analysis (CLA) is a technique used in strategic planning, futures studies and foresight to more effectively shape the future. The technique was pioneered by Sohail Inayatullah, a Pakistani-Australian futures studies researcher.

Triple bottom line cost-benefit analysis (TBL-CBA) is an evidence-based economic method that combines cost–benefit analysis (CBA) and life-cycle cost analysis (LCCA) across the triple bottom line (TBL) to weigh costs and benefits to project stakeholders. The TBL-CBA process quantifies total net present value, return on investment, and project payback. TBL-CBA uses location-specific data to give asset owners and design professionals the flexibility and capability to provide a rigorous analysis of investment alternatives through all stages of planning and design.

References

- ↑ "Sustainability – From Principle To Practice". Goethe-Institut. March 2008. Archived from the original on 2014-10-20.

- ↑ "Enhancing the role of industry through for example, private-public partnerships" (PDF). United Nations Environment Programme. May 2011. Archived from the original (PDF) on 2012-11-12.

- ↑ Barkemeyer, Ralf; Figge, Frank; Holt, Diane; Hahn, Tobias (2009). "What the Papers Say: Trends in Sustainability: A Comparative Analysis of 115 Leading National Newspapers Worldwide". The Journal of Corporate Citizenship (33): 69–86. JSTOR jcorpciti.33.69. SSRN 2375569.

- 1 2 3 Sawaf, Ayman; Gabrielle, Rowan (2014). Sacred Commerce: A Blueprint for a New Humanity (2nd ed.). EQ Enterprises. pp. 24–28. ISBN 978-0-9906987-0-8.

- 1 2 "Spirituality as the fourth bottom line? | USC Research Bank - University of the Sunshine Coast". research.usc.edu.au. Archived from the original on 2016-03-04. Retrieved 2015-09-21.

- 1 2 3 Taback, Hal; Ramanan, Ram (2013-07-29). Environmental Ethics and Sustainability: A Casebook for Environmental Professionals. CRC Press. ISBN 9781466584211.

- 1 2 "Compassion as the fourth bottom line?". The Values-Based Business. 10 August 2014. Archived from the original on 2015-09-04. Retrieved 2015-09-21.

- ↑ Inayatullah, Sohail (1 August 2005). "Spirituality as the fourth bottom line?". Futures. 37 (6): 573–579. doi:10.1016/j.futures.2004.10.015.

- ↑ "Happiness-Spirituality as The Fourth Bottom Line | Triple Bottom Line Magazine". www.tbl.com.pk. 18 July 2008. Archived from the original on 2016-03-04. Retrieved 2015-09-21.

- ↑ "T02-Fourth Bottom Line". 25 January 2010. Archived from the original on 2015-06-12. Retrieved 2015-09-21.

- ↑ "SPIRITUALITY AS THE FOURTH BOTTOM LINE". www.metafuture.org. Archived from the original on 2015-09-23. Retrieved 2015-09-21.