The Federal Reserve System is the central banking system of the United States. It was created on December 23, 1913, with the enactment of the Federal Reserve Act, after a series of financial panics led to the desire for central control of the monetary system in order to alleviate financial crises. Over the years, events such as the Great Depression in the 1930s and the Great Recession during the 2000s have led to the expansion of the roles and responsibilities of the Federal Reserve System.

The monetary policy of The United States is the set of policies related to the minting and printing of United States dollars, plus the legal exchange of currency, demand deposits, the money supply, etc. In the United States, the central bank, The Federal Reserve System, colloquially known as "The Fed" is the monetary authority.

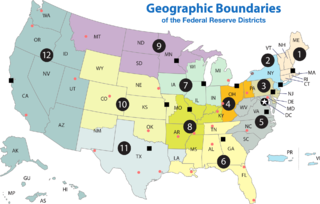

A Federal Reserve Bank is a regional bank of the Federal Reserve System, the central banking system of the United States. There are twelve in total, one for each of the twelve Federal Reserve Districts that were created by the Federal Reserve Act of 1913. The banks are jointly responsible for implementing the monetary policy set forth by the Federal Open Market Committee, and are divided as follows:

In macroeconomics, an open market operation (OMO) is an activity by a central bank to give liquidity in its currency to a bank or a group of banks. The central bank can either buy or sell government bonds in the open market or, in what is now mostly the preferred solution, enter into a repo or secured lending transaction with a commercial bank: the central bank gives the money as a deposit for a defined period and synchronously takes an eligible asset as collateral.

Reserve requirements are central bank regulations that set the minimum amount that a commercial bank must hold in liquid assets. This minimum amount, commonly referred to as the commercial bank's reserve, is generally determined by the central bank on the basis of a specified proportion of deposit liabilities of the bank. This rate is commonly referred to as the reserve ratio. Though the definitions vary, the commercial bank's reserves normally consist of cash held by the bank and stored physically in the bank vault, plus the amount of the bank's balance in that bank's account with the central bank. A bank is at liberty to hold in reserve sums above this minimum requirement, commonly referred to as excess reserves.

A lender of last resort (LOLR) is the institution in a financial system that acts as the provider of liquidity to a financial institution which finds itself unable to obtain sufficient liquidity in the interbank lending market when other facilities or such sources have been exhausted. It is, in effect, a government guarantee to provide liquidity to financial institutions. Since the beginning of the 20th century, most central banks have been providers of lender of last resort facilities, and their functions usually also include ensuring liquidity in the financial market in general.

In the United States, federal funds are overnight borrowings between banks and other entities to maintain their bank reserves at the Federal Reserve. Banks keep reserves at Federal Reserve Banks to meet their reserve requirements and to clear financial transactions. Transactions in the federal funds market enable depository institutions with reserve balances in excess of reserve requirements to lend reserves to institutions with reserve deficiencies. These loans are usually made for one day only, that is, "overnight". The interest rate at which these deals are done is called the federal funds rate. Federal funds are not collateralized; like eurodollars, they are an unsecured interbank loan.

The discount window is an instrument of monetary policy that allows eligible institutions to borrow money from the central bank, usually on a short-term basis, to meet temporary shortages of liquidity caused by internal or external disruptions. The term originated with the practice of sending a bank representative to a reserve bank teller window when a bank needed to borrow money.

Excess reserves are bank reserves held by a bank in excess of a reserve requirement for it set by a central bank.

The Federal Reserve Bank of Atlanta,, is the sixth district of the 12 Federal Reserve Banks of the United States and is headquartered in midtown Atlanta, Georgia.

Bank rate, also known as discount rate in American English, is the rate of interest which a central bank charges on its loans and advances to a commercial bank. The bank rate is known by a number of different terms depending on the country, and has changed over time in some countries as the mechanisms used to manage the rate have changed.

Quantitative easing (QE) is a monetary policy action where a central bank purchases predetermined amounts of government bonds or other financial assets in order to stimulate economic activity. Quantitative easing is a novel form of monetary policy that came into wide application after the financial crisis of 2007-2008. It is intended to mitigate an economic recession when inflation is very low or negative, making standard monetary policy ineffective. Quantitative tightening (QT) does the opposite, where for monetary policy reasons, a central bank sells off some portion of its holdings of government bonds or other financial assets.

This is a list of historical rate actions by the United States Federal Open Market Committee (FOMC). The FOMC controls the supply of credit to banks and the sale of treasury securities. The Federal Open Market Committee meets every two months during the fiscal year. At scheduled meetings, the FOMC meets and makes any changes it sees as necessary, notably to the federal funds rate and the discount rate. The committee may also take actions with a less firm target, such as an increasing liquidity by the sale of a set amount of Treasury bonds, or affecting the price of currencies both foreign and domestic by selling dollar reserves. Jerome Powell is the current chairperson of the Federal Reserve and the FOMC.

On March 17, 2008, in response to the subprime mortgage crisis and the collapse of Bear Stearns, the Federal Reserve announced the creation of a new lending facility, the Primary Dealer Credit Facility (PDCF). Eligible borrowers include all financial institutions listed as primary dealers, and the term of the loan is a repurchase agreement, or "repo" loan, whereby the broker dealer sells a security in exchange for funds through the Fed's discount window. The security in question acts as collateral, and the Federal Reserve charges an interest rate equivalent to the Fed's primary credit rate. The facility was intended to improve the ability of broker dealers to access liquidity in the overnight loan market that banks use to meet their reserve requirements.

The Term Securities Lending Facility (TSLF) was a 28-day facility managed by the United States Federal Reserve offering Treasury general collateral (GC) to the primary dealers in exchange for other program-eligible collateral. It was created to combat the liquidity crisis in American banks that had begun in late 2007, part of the broader financial crisis of 2007-2008. The facility was open from March 2008 through January 2010.

The U.S. central banking system, the Federal Reserve, in partnership with central banks around the world, took several steps to address the subprime mortgage crisis. Federal Reserve Chairman Ben Bernanke stated in early 2008: "Broadly, the Federal Reserve’s response has followed two tracks: efforts to support market liquidity and functioning and the pursuit of our macroeconomic objectives through monetary policy." A 2011 study by the Government Accountability Office found that "on numerous occasions in 2008 and 2009, the Federal Reserve Board invoked emergency authority under the Federal Reserve Act of 1913 to authorize new broad-based programs and financial assistance to individual institutions to stabilize financial markets. Loans outstanding for the emergency programs peaked at more than $1 trillion in late 2008."

The interbank lending market is a market in which banks lend funds to one another for a specified term. Most interbank loans are for maturities of one week or less, the majority being overnight. Such loans are made at the interbank rate. A sharp decline in transaction volume in this market was a major contributing factor to the collapse of several financial institutions during the financial crisis of 2007–2008.

The Subprime mortgage crisis solutions debate discusses various actions and proposals by economists, government officials, journalists, and business leaders to address the subprime mortgage crisis and broader financial crisis of 2007–08.

Central bank liquidity swap is a type of currency swap used by a country's central bank to provide liquidity of its currency to another country's central bank. In a liquidity swap, the lending central bank uses its currency to buy the currency of another borrowing central bank at the market exchange rate, and agrees to sell the borrower's currency back at a rate that reflects the interest accrued on the loan. The borrower's currency serves as collateral.

United States policy responses to the late-2000s recession explores legislation, banking industry and market volatility within retirement plans.