The Federal Reserve System (often shortened to the Federal Reserve, or simply the Fed) is the central banking system of the United States. It was created on December 23, 1913, with the enactment of the Federal Reserve Act, after a series of financial panics (particularly the panic of 1907) led to the desire for central control of the monetary system in order to alleviate financial crises.[list 1] Although an instrument of the U.S. government, the Federal Reserve System considers itself "an independent central bank because its monetary policy decisions do not have to be approved by the president or by anyone else in the executive or legislative branches of government, it does not receive funding appropriated by Congress, and the terms of the members of the board of governors span multiple presidential and congressional terms."[11] Over the years, events such as the Great Depression in the 1930s and the Great Recession during the 2000s have led to the expansion of the roles and responsibilities of the Federal Reserve System.[6][12]

Congress established three key objectives for monetary policy in the Federal Reserve Act: maximizing employment, stabilizing prices, and moderating long-term interest rates.[13] The first two objectives are sometimes referred to as the Federal Reserve's dual mandate.[14] Its duties have expanded over the years, and include supervising and regulating banks, maintaining the stability of the financial system, and providing financial services to depository institutions, the U.S. government, and foreign official institutions.[15] The Fed also conducts research into the economy and provides numerous publications, such as the Beige Book and the FRED database.[16]

The Federal Reserve System is composed of several layers. It is governed by the presidentially appointed board of governors or Federal Reserve Board (FRB). Twelve regional Federal Reserve Banks, located in cities throughout the nation, regulate and oversee privately owned commercial banks.[17] Nationally chartered commercial banks are required to hold stock in, and can elect some board members of, the Federal Reserve Bank of their region.

The Federal Open Market Committee (FOMC) sets monetary policy by adjusting the target for the federal funds rate, which generally influences market interest rates and, in turn, US economic activity via the monetary transmission mechanism. The FOMC consists of all seven members of the board of governors and the twelve regional Federal Reserve Bank presidents, though only five bank presidents vote at a time: the president of the New York Fed and four others who rotate through one-year voting terms. There are also various advisory councils.[list 2] It has a structure unique among central banks, and is also unusual in that the United States Department of the Treasury, an entity outside of the central bank, prints the currency used.[23]

The federal government sets the salaries of the board's seven governors, and it receives all the system's annual profits after dividends on member banks' capital investments are paid, and an account surplus is maintained. In 2015, the Federal Reserve earned a net income of $100.2 billion and transferred $97.7 billion to the U.S. Treasury,[24] and 2020 earnings were approximately $88.6 billion with remittances to the U.S. Treasury of $86.9 billion.[25]

Before the founding of the Federal Reserve System, the United States underwent several financial crises. A particularly severe crisis in 1907 led Congress to enact the Federal Reserve Act in 1913. The primary declared motivation for creating the Federal Reserve System was to address banking panics.[6] Other stated purposes, are "to furnish an elastic currency, to afford means of rediscounting commercial paper, [and] to establish a more effective supervision of banking in the United States".[34]

Today, the purposes of the Federal Reserve include the responsibilities to:[15][35]

Banks usually invest the majority of the funds received from depositors. However, banking institutions in the United States are required to hold reserves—amounts of currency and deposits in other banks—equal to a fraction of the amount of the bank's deposit liabilities owed to customers. This practice is called fractional-reserve banking. On rare occasions, too many of the bank's customers will withdraw their savings such that the bank cannot continue operating on its own; this is called a bank run. Bank runs can lead to a multitude of social and economic problems. The Federal Reserve System was designed as an attempt to prevent or minimize the occurrence of bank runs, and possibly act as a lender of last resort when a bank run occurs. Many economists, following Nobel laureate Milton Friedman, believe that the Federal Reserve inappropriately refused to lend money to small banks during the bank runs of 1929; Friedman argued that this contributed to the Great Depression.[37]

Check clearing system

Before the establishment of the Federal Reserve, during times of economic uncertainty, some banks refused to clear checks from certain other banks, which led to large-scale bank failure in the early 20th-century. Hence, a national check-clearing system was created in the Federal Reserve System.[38] The Federal Reserve can physically accept and transport cheques.[39]

Lender of last resort

In the United States of America, the Federal Reserve serves as the lender of last resort to those institutions that cannot obtain credit elsewhere, institutions the collapse of which would have serious implications for the economy. It took over this role from the private sector clearing houses which operated during the Free Banking Era. The availability of liquidity is intended to prevent bank runs.[40]

Fluctuations

Reserve Banks provide liquidity to banks to meet short-term needs stemming from seasonal fluctuations in deposits or unexpected withdrawals through its discount window and credit operations. Longer-term liquidity may also be provided in exceptional circumstances. The rate the Fed charges banks for these loans is called the discount rate (officially the primary credit rate). By making these loans, the Fed serves as a buffer against unexpected day-to-day fluctuations in reserve demand and supply. This contributes to the effective functioning of the banking system, alleviates pressure in the reserves market, and reduces the extent of unexpected movements in the interest rates.[41] For example, on September 16, 2008, the Federal Reserve Board authorized an $85billion loan to stave off the bankruptcy of international insurance giant American International Group (AIG).[42]

Obverse of a Federal Reserve $1 note issued in 2021

As the central bank of the United States, the Fed serves as a banker's bank and as the government's bank. As the banker's bank, it helps to assure the safety and efficiency of the payments system. As the government's bank or fiscal agent, the Fed processes a variety of financial transactions involving trillions of dollars. The U.S. Treasury keeps a checking account with the Federal Reserve, through which incoming federal tax deposits and outgoing government payments are handled. As part of this service relationship, the Fed sells and redeems U.S. government securities such as savings bonds and Treasury bills, notes and bonds. It also issues the nation's coin and paper currency. The U.S. Treasury, through its Bureau of the Mint and Bureau of Engraving and Printing, actually produces the nation's cash supply and, in effect, sells the paper currency to the Federal Reserve Banks at manufacturing cost, and the coins at face value. The Federal Reserve Banks then distribute it to other financial institutions in various ways.[43] During the Fiscal Year 2020, the Bureau of Engraving and Printing delivered 57.95billion notes at an average cost of 7.4 cents per note.[44][45]

Federal funds, officially Federal Reserve Deposits, are the reserve balances that private banks keep at their local Federal Reserve Bank.[46] These balances are the namesake reserves of the Federal Reserve System. The purpose of keeping funds at a Federal Reserve Bank is to have a mechanism for private banks to lend funds to one another. This market for funds plays an important role in the Federal Reserve System as it is the basis for its monetary policy work. Monetary policy is put into effect partly by influencing how much interest the private banks charge each other for the lending of these funds. Federal reserve accounts contain federal reserve credit, which can be converted into federal reserve notes.[citation needed]

Bank regulator

The Federal Reserve regulates private banks. The system was designed out of a compromise between the competing philosophies of privatization and government regulation. In 2006 Donald L. Kohn, vice chairman of the board of governors, summarized the history of this compromise:[47]

Agrarian and progressive interests, led by William Jennings Bryan, favored a central bank under public, rather than banker, control. However, the vast majority of the nation's bankers, concerned about government intervention in the banking business, opposed a central bank structure directed by political appointees. The legislation that Congress ultimately adopted in 1913 reflected a hard-fought battle to balance these two competing views and created the hybrid public-private, centralized-decentralized structure that we have today.

In the structure of the Federal Reserve System, private banks elect members of the board of directors at their regional Federal Reserve Bank while the members of the board of governors are selected by the president of the United States and confirmed by the United States Senate.[citation needed]

The Board of Governors of the Federal Reserve System has a number of supervisory and regulatory responsibilities in the U.S. banking system, but not complete responsibility. A general description of the types of regulation and supervision involved in the U.S. banking system is given by the Federal Reserve:[48]

The Board also plays a major role in the supervision and regulation of the U.S. banking system. It has supervisory responsibilities for state-chartered banks[49] that are members of the Federal Reserve System, bank holding companies (companies that control banks), the foreign activities of member banks, the U.S. activities of foreign banks, and Edge Act and "agreement corporations" (limited-purpose institutions that engage in a foreign banking business). The Board and, under delegated authority, the Federal Reserve Banks, supervise approximately 900 state member banks and 5,000 bank holding companies. Other federal agencies also serve as the primary federal supervisors of commercial banks; the Office of the Comptroller of the Currency supervises national banks, and the Federal Deposit Insurance Corporation supervises state banks that are not members of the Federal Reserve System.

Some regulations issued by the Board apply to the entire banking industry, whereas others apply only to member banks, that is, state banks that have chosen to join the Federal Reserve System and national banks, which by law must be members of the System. The Board also issues regulations to carry out major federal laws governing consumer credit protection, such as the Truth in Lending, Equal Credit Opportunity, and Home Mortgage Disclosure Acts. Many of these consumer protection regulations apply to various lenders outside the banking industry as well as to banks.

The Board has regular contact with members of the President's Council of Economic Advisers and other key economic officials. The Chair also meets from time to time with the President of the United States and has regular meetings with the Secretary of the Treasury. The Chair has formal responsibilities in the international arena as well.

The Federal Banking Agency Audit Act, enacted in 1978 as Public Law 95-320 and 31 U.S.C. section 714 establish that the board of governors of the Federal Reserve System and the Federal Reserve banks may be audited by the Government Accountability Office (GAO).[50] The GAO has authority to audit check-processing, currency storage and shipments, and some regulatory and bank examination functions – though there are restrictions to what the GAO may audit.[51]

Regulatory and oversight responsibilities

The board of directors of each Federal Reserve Bank District also has regulatory and supervisory responsibilities. If the board of directors of a district bank has judged that a member bank is performing or behaving poorly, it will report this to the board of governors. This policy is described in law:

Each Federal reserve bank shall keep itself informed of the general character and amount of the loans and investments of its member banks with a view to ascertaining whether undue use is being made of bank credit for the speculative carrying of or trading in securities, real estate, or commodities, or for any other purpose inconsistent with the maintenance of sound credit conditions; and, in determining whether to grant or refuse advances, rediscounts, or other credit accommodations, the Federal reserve bank shall give consideration to such information. The chairman of the Federal reserve bank shall report to the Board of Governors of the Federal Reserve System any such undue use of bank credit by any member bank, together with his recommendation. Whenever, in the judgment of the Board of Governors of the Federal Reserve System, any member bank is making such undue use of bank credit, the Board may, in its discretion, after reasonable notice and an opportunity for a hearing, suspend such bank from the use of the credit facilities of the Federal Reserve System and may terminate such suspension or may renew it from time to time.[52]

National payments system

In the Depository Institutions Deregulation and Monetary Control Act of 1980, Congress reaffirmed that the Federal Reserve should promote an efficient nationwide payments system. The act subjects all depository institutions, not just member commercial banks, to reserve requirements and grants them equal access to Reserve Bank payment services. The twelve Federal Reserve Banks provide banking services to depository institutions and to the federal government. For depository institutions, they maintain accounts and provide various payment services, including collecting checks, electronically transferring funds, and distributing and receiving currency and coin. For the federal government, the Reserve Banks act as fiscal agents, paying Treasury checks; processing electronic payments; and issuing, transferring, and redeeming U.S. government securities.[53]

The Federal Reserve plays a role in the nation's retail and wholesale payments systems by providing financial services to depository institutions. Retail payments are generally for relatively small-dollar amounts and often involve a depository institution's retail clients. The Reserve Banks' retail banking services include distributing currency and coin, collecting checks, electronically transferring funds through FedACH (the Federal Reserve's automated clearing house system), and beginning in 2023, facilitating instant payments using the FedNow service. The Reserve Banks' wholesale banking services include electronically transferring funds through the Fedwire Funds Service and transferring securities issued by the U.S. government, its agencies, and certain other entities through the Fedwire Securities Service. Unlike retail services, wholesale payments are generally for large-dollar amounts and often involve a depository institution's large corporate customers or counterparties.[54]

The Federal Reserve System has a "unique structure that is both public and private" and is described as "independent within the government" rather than "independent of government".[11][55] The System does not draw upon public funding, and derives its authority and purpose from the Federal Reserve Act, which was passed by Congress in 1913 and is subject to Congressional modification or repeal.[56] The four main components of the Federal Reserve System are the board of governors, the Federal Open Market Committee, the twelve regional Federal Reserve Banks, and the member banks throughout the country.

The seven-member board of governors is a large federal agency that functions in business oversight by examining national banks.[57]:12,15 It is charged with the overseeing of the 12 District Reserve Banks and setting national monetary policy. It also supervises and regulates the U.S. banking system in general.[58] Governors are appointed by the president of the United States and confirmed by the Senate for staggered 14-year terms.[41][59] One term begins every two years, on February 1 of even-numbered years, and members serving a full term cannot be renominated for a second term.[60] "[U]pon the expiration of their terms of office, members of the Board shall continue to serve until their successors are appointed and have qualified." The law provides for the removal of a member of the board by the president of the United States "for cause".[61] The board is required to make an annual report of operations to the Speaker of the U.S. House of Representatives.

The chair and vice chair of the board of governors are appointed by the president of the United States from among the sitting governors. They both serve a four-year term and they can be renominated as many times as the president chooses, until their terms on the board of governors expire.[62]

List of members of the board of governors

Board of governors in April 2019, when two of the seven seats were vacant

The current members of the board of governors are:[60]

↑On August 25, 2025, President Donald Trump announced that he was removing Cook from the Federal Reserve Board of Governors, citing alleged misconduct. Federal law allows governors to be removed only “for cause,” a provision intended to protect the central bank’s independence. Cook disputed the allegations and filed suit in federal court, arguing that her dismissal was unlawful and politically motivated. As litigation proceeds, she remains legally considered an active governor,[63] pending a judicial ruling on whether the president had authority to remove her.

The Federal Open Market Committee (FOMC) consists of 12 members, seven from the board of governors and five from the regional Federal Reserve Bank presidents, and must obtain consensus on all decisions. The FOMC oversees and sets policy on open market operations, the principal tool of national monetary policy. The FOMC also directs operations undertaken by the Federal Reserve in foreign exchange markets. All Regional Reserve Bank presidents contribute to the committee's assessment of the economy and of policy options, but only the five presidents who are then members of the FOMC vote on policy decisions. The FOMC determines its own internal organization and, by tradition, elects the chair of the board of governors as its chair and the president of the Federal Reserve Bank of New York as its vice chair. Formal meetings typically are held eight times each year in Washington, D.C.[64]

There is very strong consensus among economists against politicising the FOMC.[65]

The Federal Advisory Council (FAC) is a statutory body established under the Federal Reserve Act of 1913 to provide the Board of Governors of the Federal Reserve System with insights and recommendations from the banking industry and regional economic perspectives. Comprising one representative from each of the 12 Federal Reserve Districts, the Council meets at least four times annually in Washington, D.C. to discuss economic and banking issues and offer advisory opinions to the Board. Each Federal Reserve Bank’s board of directors selects its district’s representative, typically a senior executive from a member bank, ensuring diverse geographic and institutional input.[6]

Map of the 12 Federal Reserve Districts, with the 12 Federal Reserve Banks marked as black squares, and all Branches within each district (24 total) marked as red circles. The Washington, DC, headquarters is marked with a star. (Also, a 25th branch in Buffalo, NY, was closed in 2008.)The 12 Reserve Banks buildings in 1936

There are 12 Federal Reserve Banks, each of which is responsible for member banks located in its district. They are located in Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Chicago, St. Louis, Minneapolis, Kansas City, Dallas, and San Francisco. The size of each district was set based upon the population distribution of the United States when the Federal Reserve Act was passed. The charter and organization of each bank is established by law and cannot be altered by the member banks.[41][66] Each regional bank has a president, who is the chief executive officer of their bank. Each president is nominated by their bank's board of directors, but the nomination is contingent upon approval by the board of governors. Presidents serve five-year terms and may be reappointed.[67]

Plaque marking a bank as a member

Member banks

A member bank is a private institution and owns stock in its regional Federal Reserve Bank. All nationally chartered banks hold stock in one of the Federal Reserve Banks. State chartered banks may choose to be members (and hold stock in their regional Federal Reserve bank) upon meeting certain standards. The amount of stock a member bank must own is equal to 3% of its combined capital and surplus.[68] About 38% of U.S. banks are members of their regional Federal Reserve Bank.[11][69]

Holding stock in a Federal Reserve bank is not like owning stock in a publicly traded company. These stocks cannot be sold or traded, and member banks do not control the Federal Reserve Bank as a result of owning this stock. From their Regional Bank, member banks with $10billion or less in assets receive a dividend of 6%, while member banks with more than $10billion in assets receive the lesser of 6% or the current 10-year Treasury auction rate.[70] The remainder of the regional Federal Reserve Banks' profits is given over to the United States Treasury Department. In 2015, the Federal Reserve Banks made a profit of $100.2billion and distributed $2.5billion in dividends to member banks as well as returning $97.7billion to the U.S. Treasury.[24]

Accountability

An external auditor selected by the audit committee of the Federal Reserve System regularly audits the Board of Governors and the Federal Reserve Banks. The GAO will audit some activities of the Board of Governors. These audits do not cover "most of the Fed's monetary policy actions or decisions, including discount window lending, open-market operations and any other transactions made under the direction of the Federal Open Market Committee" ...[nor may the GAO audit] "dealings with foreign governments and other central banks."[71]

The annual and quarterly financial statements prepared by the Federal Reserve System conform to a basis of accounting that is set by the Federal Reserve Board and does not conform to Generally Accepted Accounting Principles (GAAP) or government Cost Accounting Standards (CAS). The financial reporting standards are defined in the Financial Accounting Manual for the Federal Reserve Banks.[72] The cost accounting standards are defined in the Planning and Control System Manual.[72]As of 27August2012[update], the Federal Reserve Board has been publishing unaudited financial reports for the Federal Reserve banks every quarter.[73]

The term "monetary policy" refers to the actions undertaken by a central bank, such as the Federal Reserve, to influence economic activity (the overall demand for goods and services) to help promote national economic goals. The Federal Reserve Act of 1913 gave the Federal Reserve authority to set monetary policy in the United States. The Fed's mandate for monetary policy is commonly known as the dual mandate of promoting maximum employment and stable prices, the latter being interpreted as a stable inflation rate of 2 percent per year on average. The Fed's monetary policy influences economic activity by influencing the general level of interest rates in the economy, which again via the monetary transmission mechanism affects households' and firms' demand for goods and services and in turn employment and inflation.[36]

The Federal Reserve sets monetary policy by influencing the federal funds rate, which is the rate of interbank lending of reserve balances. The rate that banks charge each other for these loans is determined in the interbank market, and the Federal Reserve influences this rate through the "tools" of monetary policy described in the Tools section below. The federal funds rate is a short-term interest rate that the FOMC focuses on, which affects the longer-term interest rates throughout the economy. The Federal Reserve explained the implementation of its monetary policy in 2021:

The FOMC has the ability to influence the federal funds rate–and thus the cost of short-term interbank credit–by changing the rate of interest the Fed pays on reserve balances that banks hold at the Fed. A bank is unlikely to lend to another bank (or to any of its customers) at an interest rate lower than the rate that the bank can earn on reserve balances held at the Fed. And because overall reserve balances are currently abundant, if a bank wants to borrow reserve balances, it likely will be able to do so without having to pay a rate much above the rate of interest paid by the Fed.[36]

Changes in the target for the federal funds rate affect overall financial conditions through various channels, including subsequent changes in the market interest rates that commercial banks and other lenders charge on short-term and longer-term loans, and changes in asset prices and in currency exchange rates, which again affects private consumption, investment and net export. By easening or tightening the stance of monetary policy, i.e. lowering or raising its target for the federal funds rate, the Fed can either spur or restrain growth in the overall US demand for goods and services.[36]

Tools

There are four main tools of monetary policy that the Federal Reserve uses to implement its monetary policy:[77][78]

Interest on reserve balances (IORB)

Interest paid on funds that banks hold in their reserve balance accounts at their Federal Reserve Bank.[79] IORB is the primary tool for moving the federal funds rate within the target range.[77]

Overnight reverse repurchase agreement (ON RRP) facility

The Fed's standing offer to many large nonbank financial institutions to deposit funds at the Fed and earn interest. Acts as a supplementary tool for moving the FFR within the target range.[77]

The Federal Reserve System implements monetary policy largely by targeting the federal funds rate. This is the interest rate that banks charge each other for overnight loans of federal funds, which are the reserves held by banks at the Fed. This rate is actually determined by the market and is not explicitly mandated by the Fed. The Fed therefore tries to align the effective federal funds rate with the targeted rate, mainly by adjusting its IORB rate.[81] The Federal Reserve System usually adjusts the federal funds rate target by 0.25% or 0.50% at a time.

Interest on reserve balances

The interest on reserve balances (IORB) is the interest that the Fed pays on funds held by commercial banks in their reserve balance accounts at the individual Federal Reserve System banks. It is an administrated interest rate (i.e. set directly by the Fed as opposed to a market interest rate which is determined by the forces of supply and demand).[81] As banks are unlikely to lend their reserves in the FFR market for less than they get paid by the Fed, the IORB guides the effective FFR and is used as the primary tool of the Fed's monetary policy.[82][81]

Open market operations are done through the sale and purchase of United States Treasury securities, or "Treasurys". The Federal Reserve buys Treasurys both directly and via primary dealers, which have accounts at depository institutions.[83]

The Federal Reserve's objective for open market operations has varied over the years. During the 1980s, the focus gradually shifted toward attaining a specified level of the federal funds rate (the rate that banks charge each other for overnight loans of federal funds, which are the reserves held by banks at the Fed), a process that was largely complete by the end of the decade.[84]

Until the 2008 financial crisis, the Fed used open market operations as its primary tool to adjust the supply of reserve balances in order to keep the federal funds rate around the Fed's target.[85] This regime is also known as a limited reserves regime.[82] After the 2008 financial crisis, the Federal Reserve has adopted a so-called ample reserves regime where open market operations leading to modest changes in the supply of reserves are no longer effective in influencing the FFR. Instead the Fed uses its administered rates, in particular the IORB rate, to influence the FFR.[82][81] However, open market operations are still an important maintenance tool in the overall framework of the conduct of monetary policy as they are used for ensuring that reserves remain ample.[82]

To smooth temporary or cyclical changes in the money supply, the desk engages in repurchase agreements (repos) with its primary dealers. Repos are essentially secured, short-term lending by the Fed. On the day of the transaction, the Fed deposits money in a primary dealer's reserve account, and receives the promised securities as collateral. When the transaction matures, the process unwinds: the Fed returns the collateral and charges the primary dealer's reserve account for the principal and accrued interest. The term of the repo (the time between settlement and maturity) can vary from 1 day (called an overnight repo) to 65 days.[86]

The Federal Reserve System also directly sets the discount rate, which is the interest rate for "discount window lending", overnight loans that member banks borrow directly from the Fed. This rate is generally set at a rate close to 100 basis points above the target federal funds rate. The idea is to encourage banks to seek alternative funding before using the "discount rate" option.[87] The equivalent operation by the European Central Bank is referred to as the "marginal lending facility".[88]

Both the discount rate and the federal funds rate influence the prime rate, which is usually about 3 percentage points higher than the federal funds rate.

Term Deposit facility

The Term Deposit facility is a program through which the Federal Reserve Banks offer interest-bearing term deposits to eligible institutions.[89] It is intended to facilitate the implementation of monetary policy by providing a tool by which the Federal Reserve can manage the aggregate quantity of reserve balances held by depository institutions. Funds placed in term deposits are removed from the accounts of participating institutions for the life of the term deposit and thus drain reserve balances from the banking system. The program was announced December 9, 2009, and approved April 30, 2010, with an effective date of June 4, 2010.[90] Fed Chair Ben S. Bernanke, testifying before the House Committee on Financial Services, stated that the Term Deposit Facility would be used to reverse the expansion of credit during the Great Recession, by drawing funds out of the money markets into the Federal Reserve Banks.[91] It would therefore result in increased market interest rates, acting as a brake on economic activity and inflation.[92] The Federal Reserve authorized up to five "small-value offerings" in 2010 as a pilot program.[93] After three of the offering auctions were successfully completed, it was announced that small-value auctions would continue on an ongoing basis.[94]

Quantitative easing (QE) policy

A little-used tool of the Federal Reserve is the quantitative easing policy.[95] Under that policy, the Federal Reserve buys back corporate bonds and mortgage backed securities held by banks or other financial institutions. This in effect puts money back into the financial institutions and allows them to make loans and conduct normal business. The bursting of the United States housing bubble prompted the Fed to buy mortgage-backed securities for the first time in November 2008. Over six weeks, a total of $1.25trillion were purchased in order to stabilize the housing market, about one-fifth of all U.S. government-backed mortgages.[96]

Expired policy tools

Reserve requirements

An instrument of monetary policy adjustment historically employed by the Federal Reserve System was the fractional reserve requirement, also known as the required reserve ratio.[97] The required reserve ratio set the balance that the Federal Reserve System required a depository institution to hold in the Federal Reserve Banks.[98] The required reserve ratio was set by the board of governors of the Federal Reserve System.[99] The reserve requirements have changed over time and some history of these changes is published by the Federal Reserve.[100]

As a response to the 2008 financial crisis, the Federal Reserve started making interest payments on depository institutions' required and excess reserve balances. The payment of interest on excess reserves gave the central bank greater opportunity to address credit market conditions while maintaining the federal funds rate close to the target rate set by the FOMC.[101] The reserve requirement did not play a significant role in the post-2008 interest-on-excess-reserves regime,[102] and in March 2020, the reserve ratio was set to zero for all banks, which meant that no bank was required to hold any reserves, and hence the reserve requirement effectively ceased to exist, though the legal framework exists for it to be reinstated at any time.[1][103]

Temporary policy tools during the 2008 financial crisis

In order to address problems related to the subprime mortgage crisis and United States housing bubble, several new tools were created. The first new tool, called the Term auction facility, was added on December 12, 2007. It was announced as a temporary tool,[104] but remained in place for a prolonged period of time.[105] Creation of the second new tool, called the Term Securities Lending Facility, was announced on March 11, 2008.[106] The main difference between these two facilities was that the Term auction Facility was used to inject cash into the banking system whereas the Term securities Lending Facility was used to inject treasury securities into the banking system.[107] Creation of the third tool, called the Primary Dealer Credit Facility (PDCF), was announced on March 16, 2008.[108] The PDCF was a fundamental change in Federal Reserve policy because it enabled the Fed to lend directly to primary dealers, which was previously against Fed policy.[109] The differences between these three facilities was described by the Federal Reserve:[110]

The Term auction Facility program offers term funding to depository institutions via a bi-weekly auction, for fixed amounts of credit. The Term securities Lending Facility will be an auction for a fixed amount of lending of Treasury general collateral in exchange for OMO-eligible and AAA/Aaa rated private-label residential mortgage-backed securities. The Primary Dealer Credit Facility now allows eligible primary dealers to borrow at the existing Discount Rate for up to 120 days.

The Term auction Facility was a program in which the Federal Reserve auctioned term funds to depository institutions.[104] The creation of this facility was announced by the Federal Reserve on December 12, 2007, and was done in conjunction with the Bank of Canada, the Bank of England, the European Central Bank, and the Swiss National Bank to address elevated pressures in short-term funding markets.[112] The reason it was created was that banks were not lending funds to one another and banks in need of funds were refusing to go to the discount window. Banks were not lending money to each other because there was a fear that the loans would not be paid back. Banks refused to go to the discount window because it was usually associated with the stigma of bank failure.[113][114][115][116] Under the Term auction Facility, the identity of the banks in need of funds was protected in order to avoid the stigma of bank failure.[117]Foreign exchange swap lines with the European Central Bank and Swiss National Bank were opened so the banks in Europe could have access to U.S. dollars.[117] The final Term Auction Facility auction was carried out on March 8, 2010.[118]

Term securities lending facility

The Term securities Lending Facility was a 28-day facility that offered Treasury general collateral to the Federal Reserve Bank of New York's primary dealers in exchange for other program-eligible collateral. It was intended to promote liquidity in the financing markets for Treasury and other collateral and thus to foster the functioning of financial markets more generally.[119] Like the Term auction Facility, the TSLF was done in conjunction with the Bank of Canada, the Bank of England, the European Central Bank, and the Swiss National Bank. The resource allowed dealers to switch debt that was less liquid for U.S. government securities that were easily tradable. The currency swap lines with the European Central Bank and Swiss National Bank were increased. The TSLF was closed on February 1, 2010.[120]

Primary dealer credit facility

The Primary Dealer Credit Facility (PDCF) was an overnight loan facility that provided funding to primary dealers in exchange for a specified range of eligible collateral and was intended to foster the functioning of financial markets more generally.[110] The PDCF established in 2008 was closed on February 1, 2010, alongside other crisis-era facilities.[121] A new PDCF was introduced in March 2020 in response to COVID-19-related market disruptions, and that facility ceased extending credit in 2021.[122]

Asset Backed Commercial Paper Money Market Mutual Fund Liquidity Facility

The Asset Backed Commercial Paper Money Market Mutual Fund Liquidity Facility (ABCPMMMFLF) was also called the AMLF. The Facility began operations on September 22, 2008, and was closed on February 1, 2010.[123] All U.S. depository institutions, bank holding companies (parent companies or U.S. broker-dealer affiliates), or U.S. branches and agencies of foreign banks were eligible to borrow under this facility pursuant to the discretion of the FRBB.

Collateral eligible for pledge under the Facility was required to meet the following criteria:

was purchased by Borrower on or after September 19, 2008, from a registered investment company that held itself out as a money market mutual fund;

was purchased by Borrower at the Fund's acquisition cost as adjusted for amortization of premium or accretion of discount on the ABCP through the date of its purchase by Borrower;

was rated at the time pledged to FRBB, not lower than A1, F1, or P1 by at least two major rating agencies or, if rated by only one major rating agency, the ABCP must have been rated within the top rating category by that agency;

was issued by an entity organized under the laws of the United States or a political subdivision thereof under a program that was in existence on September 18, 2008; and

had stated maturity that did not exceed 120 days if the Borrower was a bank or 270 days for non-bank Borrowers.

Commercial Paper Funding Facility

On October 7, 2008, the Federal Reserve further expanded the collateral it would loan against to include commercial paper using the Commercial Paper Funding Facility (CPFF). The action made the Fed a crucial source of credit for non-financial businesses in addition to commercial banks and investment firms. Fed officials said they would buy as much of the debt as necessary to get the market functioning again. They refused to say how much that might be, but they noted that around $1.3 trillion worth of commercial paper would qualify. There was $1.61 trillion in outstanding commercial paper, seasonally adjusted, on the market as of 1October2008[update], according to the most recent data from the Fed. That was down from $1.70 trillion in the previous week. Since the summer of 2007, the market had shrunk from more than $2.2 trillion.[124][125] This program lent out a total $738 billion before it was closed. Forty-five out of 81 of the companies participating in this program were foreign firms. Research shows that Troubled Asset Relief Program (TARP) recipients were twice as likely to participate in the program than other commercial paper issuers who did not take advantage of the TARP bailout. The Fed incurred no losses from the CPFF.[126]

In response to the economic disruptions caused by the COVID-19 pandemic, the Federal Reserve reintroduced the Commercial Paper Funding Facility (CPFF) on March 17, 2020, to support the flow of credit to households and businesses by purchasing eligible commercial paper.[127] The CPFF was modeled after the 2008 crisis-era facility and aimed to stabilize the commercial paper market.[128] The facility ceased operations on March 31, 2021, and is not in place as of April 2025.[128]

Term Asset-Backed Security Loan Facility

The Term Asset-Backed Securities Loan Facility (TALF) was a temporary program announced on November 25, 2008, and launched in March 2009 by the Federal Reserve in collaboration with the U.S. Treasury to stimulate consumer and business lending. It provided non-recourse loans to investors to purchase asset-backed securities (ABS), such as auto loans, student loans, and credit card receivables, aiming to enhance liquidity in these markets.[129] The facility ceased issuing new loans in June 2010 and was fully wound down by 2015. As a significant tool during the 2008 financial crisis, TALF focused on ABS markets rather than direct banking system liquidity, distinguishing it from other crisis-era facilities.[130]

The first attempt at a national currency was during the American Revolutionary War. In 1775, the Continental Congress, as well as the states, began issuing paper currency, calling the bills "Continentals".[132] The Continentals were backed only by future tax revenue, and were used to help finance the Revolutionary War. Overprinting, as well as British counterfeiting, caused the value of the Continental to diminish quickly. This experience with paper money led the United States to strip the power to issue Bills of Credit (paper money) from a draft of the new Constitution on August 16, 1787,[133] as well as banning such issuance by the various states, and limiting the states' ability to make anything but gold or silver coin legal tender on August 28.[134]

In 1791, the government granted the First Bank of the United States a charter to operate as the U.S. central bank until 1811.[135] The First Bank of the United States came to an end under President Madison when Congress refused to renew its charter. The Second Bank of the United States was established in 1816, and lost its authority to be the central bank of the U.S. twenty years later under President Jackson when its charter expired. Both banks were based upon the Bank of England.[136] Ultimately, a third national bank, known as the Federal Reserve, was established in 1913 and still exists to this day.

First Central Bank, 1791 and Second Central Bank, 1816

The first U.S. institution with central banking responsibilities was the First Bank of the United States, chartered by Congress and signed into law by President George Washington on February 25, 1791, at the urging of Alexander Hamilton. This was done despite strong opposition from Thomas Jefferson and James Madison, among numerous others. The charter was for twenty years and expired in 1811 under President Madison, when Congress refused to renew it.[137]

In 1816, however, Madison revived it in the form of the Second Bank of the United States. Years later, early renewal of the bank's charter became the primary issue in the reelection of President Andrew Jackson. After Jackson, who was opposed to the central bank, was reelected, he pulled the government's funds out of the bank. Jackson was the only President to completely pay off the national debt[138] but his efforts to close the bank contributed to the Panic of 1837. The bank's charter was not renewed in 1836, and it would fully dissolve after several years as a private corporation.

The main motivation for the third central banking system came from the Panic of 1907, which caused a renewed desire among legislators, economists, and bankers for an overhaul of the monetary system.[8][9][10][139] During the last quarter of the 19th century and the beginning of the 20th century, the United States economy went through a series of financial panics.[140] According to many economists, the previous national banking system had two main weaknesses: an inelastic currency and a lack of liquidity.[140] In 1908, Congress enacted the Aldrich–Vreeland Act, which provided for an emergency currency and established the National Monetary Commission to study banking and currency reform.[141] The National Monetary Commission returned with recommendations which were repeatedly rejected by Congress. A revision crafted during a secret meeting on Jekyll Island by Senator Aldrich and representatives of the nation's top finance and industrial groups later became the basis of the Federal Reserve Act.[142]

The head of the bipartisan National Monetary Commission was financial expert and Senate Republican leader Nelson Aldrich. Aldrich set up two commissions – one to study the American monetary system in depth and the other, headed by Aldrich himself, to study the European central banking systems and report on them.[141]

In early November 1910, Aldrich met with five well known members of the New York banking community to devise a central banking bill. Paul Warburg, an attendee of the meeting and longtime advocate of central banking in the U.S., later wrote that Aldrich was "bewildered at all that he had absorbed abroad and he was faced with the difficult task of writing a highly technical bill while being harassed by the daily grind of his parliamentary duties".[143] After ten days of deliberation, the bill, which would later be referred to as the "Aldrich Plan", was agreed upon. It had several key components, including a central bank with a Washington-based headquarters and fifteen branches located throughout the U.S. in geographically strategic locations, and a uniform elastic currency based on gold and commercial paper. Aldrich believed a central banking system with no political involvement was best, but was convinced by Warburg that a plan with no public control was not politically feasible.[143] The compromise involved representation of the public sector on the board of directors.[144]

Aldrich's bill met much opposition from politicians. Critics charged Aldrich of being biased due to his close ties to wealthy bankers such as J. P. Morgan and John D. Rockefeller Jr., Aldrich's son-in-law. Most Republicans favored the Aldrich Plan,[144] but it lacked enough support in Congress to pass because rural and western states viewed it as favoring the "eastern establishment".[5][145] In contrast, progressive Democrats favored a reserve system owned and operated by the government; they believed that public ownership of the central bank would end Wall Street's control of the American currency supply.[144] Conservative Democrats fought for a privately owned, yet decentralized, reserve system, which would still be free of Wall Street's control.[144]

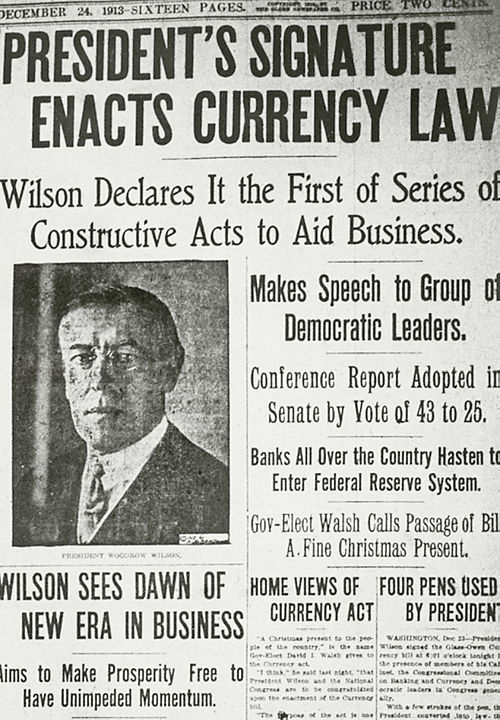

The original Aldrich Plan was dealt a fatal blow in 1912, when Democrats won the White House and Congress.[143] Nonetheless, President Woodrow Wilson believed that the Aldrich plan would suffice with a few modifications. The plan became the basis for the Federal Reserve Act, which was proposed by Senator Robert Owen in May 1913. The primary difference between the two bills was the transfer of control of the board of directors (called the Federal Open Market Committee in the Federal Reserve Act) to the government.[5][137] The bill passed Congress on December 23, 1913,[146] on a mostly partisan basis, with most Democrats voting "yea" and most Republicans voting "nay".[137]

The House voted on December 22, 1913, with 298 voting yes to 60 voting no. The Senate voted 43–25 on December 23, 1913.[147] President Woodrow Wilson signed the bill later that day.[148]

The Banking Act of 1935 created the modern structure of the Federal Reserve and placed monetary decisions beyond presidential control, thus enshrining the independence of the Federal Reserve.[150]

The Federal Reserve records and publishes large amounts of data, including the Board of Governors' Economic Data and Research page,[151] Statistical Releases and Historical Data Page,[152] and the St. Louis Fed's FRED (Federal Reserve Economic Data) page.[153] The Federal Open Market Committee (FOMC) examines many economic indicators prior to determining monetary policy.[154] Some economists have criticised the economic data compiled by the Fed. The Fed sponsors much of the monetary economics research in the U.S., and Lawrence H. White objects that this makes it less likely for researchers to publish findings challenging the status quo.[155]

Net worth of households and nonprofit organizations

Total Net Worth—Balance Sheet of Households and Nonprofit Organizations 1949–2012

The net worth of households and nonprofit organizations in the United States is published by the Federal Reserve in a report titled Flow of Funds.[156] At the end of the third quarter of fiscal year 2012, this value was $64.8 trillion. At the end of the first quarter of fiscal year 2014, this value was $95.5 trillion.[157] As of the fourth quarter of 2024, the net worth of households and nonprofit organizations reached $172.7 trillion, driven primarily by gains in corporate equity and real estate values.[158]

The Federal Reserve stopped publishing M3 statistics in March 2006, saying that the data cost a lot to collect but did not provide significantly useful information.[159] The other three money supply measures continue to be provided in detail.

One of the Fed's main roles is to maintain price stability, which means that the Fed's ability to keep a low inflation rate is a long-term measure of their success.[160] Although the Fed is not required to maintain inflation within a specific range, their long run target for the growth of the PCE price index is between 1.5 and 2 percent.[161] There has been debate among policy makers as to whether the Federal Reserve should have a specific inflation targeting policy.[162]

Low (as opposed to zero or negative) inflation may reduce the severity of economic recessions by enabling the labor market to adjust more quickly in a downturn, and reduce the risk that a liquidity trap prevents monetary policy from stabilizing the economy.[167] The task of keeping the rate of inflation low and stable is usually given to monetary authorities.

United States unemployment rates 1975–2010 showing variance between the fifty states

Budget

The Federal Reserve is self-funded. Over 90% of Fed revenues come from open market operations, specifically the interest on the portfolio of Treasury securities as well as "capital gains/losses" that may arise from the buying/selling of the securities and their derivatives as part of Open Market Operations. The balance of revenues come from sales of financial services (check and electronic payment processing) and discount window loans.[168]

The Federal Reserve Board creates a budget report once per year for Congress. There are two reports with budget information. The one that lists the complete balance statements with income and expenses, as well as the net profit or loss, is the large report simply titled, "Annual Report". It also includes data about employment throughout the system. The other report, which explains in more detail the expenses of the different aspects of the whole system, is called "Annual Report: Budget Review".[169]

Remittance payments to the Treasury

Federal Reserve remittances to the U.S. Treasury (annually)Federal Reserve Remittances to the Treasury (weekly)

In 2023, the Federal Reserve reported a net negative income of $114.3 billion.[172] This triggered the creation of a deferred asset liability on the Federal Reserve balance sheet booked as "Interest on Federal Reserve notes due to U.S. Treasury" totaling $133.3 billion.[173] The deferred asset is the amount of net excess revenues the Federal Reserve must realize before remittances can continue. It does not have any impact on the ability of the Federal Reserve to conduct monetary policy or meet its obligations.[174] The Federal Reserve has estimated the deferred asset will last until mid-2027.[175]

Total combined assets for all 12 Federal Reserve Banks, 2007–2009Total combined liabilities for all 12 Federal Reserve Banks, 2007–2009

One of the keys to understanding the Federal Reserve is the Federal Reserve balance sheet (or balance statement). In accordance with Section 11 of the Federal Reserve Act, the board of governors of the Federal Reserve System publishes once each week the "Consolidated Statement of Condition of All Federal Reserve Banks" showing the condition of each Federal Reserve bank and a consolidated statement for all Federal Reserve banks. The board of governors requires that excess earnings of the Reserve Banks be transferred to the Treasury as interest on Federal Reserve notes.[176]

The Federal Reserve releases its balance sheet every Thursday.[177] Below is the balance sheet as of 8April2021[update] (in billions of dollars):

ASSETS:

Gold Stock

11.04

Special Drawing Rights Certificate Acct.

5.20

Treasury Currency Outstanding (Coin)

1.46

Securities, unamortized premiums and discounts, repurchase agreements, and loans

The Federal Reserve System has faced various criticisms since its inception in 1913. Some of the most common critiques focus on its monetary policy, lack of transparency, and its potential role in exacerbating financial instability.[179] Critics argue that the Fed’s expansionary policies—such as lowering interest rates and increasing the money supply—can lead to inflation, asset bubbles, and economic distortions. Prominent economists like Milton Friedman have criticized the Fed for contributing to economic downturns, including its role in the Great Depression.[29]Libertarian figures such as Ron Paul have been especially vocal in calling for greater accountability and transparency within the Fed, advocating for measures such as auditing the Federal Reserve to ensure it serves the public interest rather than benefiting large financial institutions. Additionally, some critics, including Rand Paul, argue that the Fed disproportionately serves the interests of the banking elite, given the backgrounds of many of its officials in finance and banking, leading to potential conflicts of interest and policies that favor Wall Street over the general economy.

Another area of criticism is the Federal Reserve’s departure from the gold standard in 1971, which many argue has contributed to long-term inflationary pressures and a devaluation of the U.S. dollar. Ron Paul believes the Fed should be abolished and replaced with a return to the gold standard.[32] Advocates of Austrian economics, such as Ludwig von Mises and Murray Rothbard, believe that the move to fiat currency destabilized the monetary system and undermined financial stability.[180] The Federal Reserve’s handling of the 2008 financial crisis has also been a focal point of criticism, with some arguing that the Fed’s response—bailing out large banks and financial institutions—created moral hazard and worsened the economic collapse.[181]

During COVID-19 pandemic, the Federal Reserve's policies such as increasing its bank reserves, quantitative easing (QE), and keeping interest rates near zero until March 2022 had been criticised by economists, especially monetarists, as greatly contributing to the inflation spike which peaked at a record high in half a century.[182][183][184]

123"FAQ". Who Owns the Federal Reserve?. Board of Governors of the Federal Reserve System. Retrieved December 1, 2015.

↑BoG 2005, pp.1 "It was founded by Congress in 1913 to provide the nation with a safer, more flexible, and more stable monetary and financial system. Over the years, its role in banking and the economy has expanded."; Patrick, Sue C. (1993). Reform of the Federal Reserve System in the Early 1930s: The Politics of Money and Banking. Garland. ISBN978-0-8153-0970-3.

↑"What is the Federal Reserve's mandate in setting monetary policy?". Federalreserve.gov. January 25, 2012. Archived from the original on January 26, 2012. Retrieved April 30, 2012. The Congress established two key objectives for monetary policy—maximum employment and stable prices—in the Federal Reserve Act. These objectives are sometimes referred to as the Federal Reserve's dual mandate.

12"FRB: Mission". Federalreserve.gov. November 6, 2009. Retrieved October 29, 2011.

↑Toma, Mark (February 1, 2010). "Federal Reserve System". EH. Net Encyclopedia. Economic History Association. Archived from the original on May 13, 2011. Retrieved February 27, 2011.

↑Board of Governors of the Federal Reserve System (2021). "2021 Currency Budget"(PDF). federalreserve.gov.

↑"Federal Funds". Federal Reserve Bank of New York. August 2007. Retrieved August 29, 2011.; Cook, Timothy Q.; Laroche, Robert K., eds. (1993). "Instruments of the Money Market"(PDF). Federal Reserve Bank of Richmond. Archived from the original(PDF) on March 25, 2009. Retrieved August 29, 2011.

↑"Frequently Asked Questions Federal Reserve System". Archived from the original on February 17, 2010. Retrieved February 19, 2010. The Board of Governors, the Federal Reserve Banks, and the Federal Reserve System as a whole are all subject to several levels of audit and review. Under the Federal Banking Agency Audit Act, the Government Accountability Office (GAO) has conducted numerous reviews of Federal Reserve activities

↑Smith, Colby; Casselman, Ben (August 29, 2025). "How the Future of the Fed Came to Rest on Lisa Cook". The New York Times. Retrieved September 5, 2025. Until a court rules otherwise, Ms. Cook is still an active governor at the Fed. The central bank stipulated as much in a rare statement related to the president's recent actions against the institution and its members.

↑Docket entry 31, Bloomberg, L.P. v. Board of Governors of the Federal Reserve System, case no. 1:08-cv-09595-LAP, U.S. District Court for the District of New York.

↑Patricia S. Pollard (February 2003). "A Look Inside Two Central Banks: The European System of Central Banks and the Federal Reserve System". Federal Reserve Bank of St. Louis Review. 85 (2): 11–30. doi:10.3886/ICPSR01278. OCLC1569030.

↑"Fed Seeks to Limit Slump by Taking Mortgage Debt". bloomberg.com. March 12, 2008. "The step goes beyond past initiatives because the Fed can now inject liquidity without flooding the banking system with cash...Unlike the newest tool, the past steps added cash to the banking system, which affects the Fed's benchmark interest rate...By contrast, the TSLF injects liquidity by lending Treasuries, which doesn't affect the federal funds rate. That leaves the Fed free to address the mortgage crisis directly without concern about adding more cash to the system than it wants"

↑"US banks borrow $50bn via new Fed facility". Financial Times. February 18, 2008. Archived from the original on December 10, 2022. Before its introduction, banks either had to raise money in the open market or use the so-called "discount window" for emergencies. However, last year many banks refused to use the discount window, even though they found it hard to raise funds in the market, because it was associated with the stigma of bank failure

↑"Fed Boosts Next Two Special Auctions to $30 Billion". Bloomberg. January 4, 2008. The Board of Governors of the Federal Reserve System established the temporary Term Auction Facility, dubbed TAF, in December to provide cash after interest-rate cuts failed to break banks' reluctance to lend amid concern about losses related to subprime mortgage securities. The program will make funding from the Fed available beyond the 20 authorized primary dealers that trade with the central bank

↑"A dirty job, but someone has to do it". economist.com. December 13, 2007. Retrieved August 29, 2011. The Fed's discount window, for instance, through which it lends direct to banks, has barely been approached, despite the soaring spreads in the interbank market. The quarter-point cuts in its federal funds rate and discount rate on December 11 were followed by a steep sell-off in the stockmarket...The hope is that by extending the maturity of central-bank money, broadening the range of collateral against which banks can borrow and shifting from direct lending to an auction, the central bankers will bring down spreads in the one- and three-month money markets. There will be no net addition of liquidity. What the central bankers add at longer-term maturities, they will take out in the overnight market. But there are risks. The first is that, for all the fanfare, the central banks' plan will make little difference. After all, it does nothing to remove the fundamental reason why investors are worried about lending to banks. This is the uncertainty about potential losses from subprime mortgages and the products based on them, and – given that uncertainty – the banks' own desire to hoard capital against the chance that they will have to strengthen their balance sheets.

↑British Parliamentary reports on international finance: the Cunliffe Committee and the Macmillan Committee reports. Ayer Publishing. 1978. ISBN978-0-405-11212-6. description of the founding of Bank of England: 'Its foundation in 1694 arose out the difficulties of the Government of the day in securing subscriptions to State loans. Its primary purpose was to raise and lend money to the State and in consideration of this service it received under its Charter and various Act of Parliament, certain privileges of issuing bank notes. The corporation commenced, with an assured life of twelve years after which the Government had the right to annul its Charter on giving one year's notice. Subsequent extensions of this period coincided generally with the grant of additional loans to the State'

↑FRB: Z.1 Release – Flow of Funds Accounts of the United States, Release Dates See the pdf documents from 1945 to 2007. The value for each year is on page 94 of each document (the 99th page in a pdf viewer) and duplicated on page 104 (109th page in pdf viewer). It gives the total assets, total liabilities, and net worth. This chart is of the net worth.

↑Board of Governors of the Federal Reserve System. (2025, March 13). Financial Accounts of the United States: Flow of Funds, Balance Sheets, and Integrated Macroeconomic Accounts, Fourth Quarter 2024. https://www.federalreserve.gov/releases/z1/20250313/.

Conti-Brown, Peter. The Power and Independence of the Federal Reserve (Princeton University Press, 2016).

Epstein, Lita & Martin, Preston (2003). The Complete Idiot's Guide to the Federal Reserve. Alpha Books. ISBN0-02-864323-2.

Greider, William (1987). Secrets of the Temple. Simon & Schuster. ISBN0-671-67556-7; nontechnical book explaining the structures, functions, and history of the Federal Reserve, focusing specifically on the tenure of Paul Volcker.

Hafer, R. W. The Federal Reserve System: An Encyclopedia. Greenwood Press, 2005. 451 pp, 280 entries; ISBN0-313-32839-0.

Lavelle, Kathryn C. (2013) Money and Banks in the American Political System. New York: Cambridge University Press. 978-1-107-60916-7 Explains basic political processes surrounding the Federal Reserve in the broader system of Congress and the Executive Branch.

Chandler, Lester V. (1971). American Monetary Policy, 1928–1941. Harper & Row. ISBN9780060412272.

Epstein, Gerald; Ferguson, Thomas (December 1984). "Monetary Policy, Loan Liquidation and Industrial Conflict: Federal Reserve System Open Market Operations in 1932". Journal of Economic History. 44: 957–984. doi:10.1017/S0022050700033040. S2CID154187176.

Kubik, Paul J. (1996). "Federal Reserve Policy during the Great Depression: The Impact of Interwar Attitudes regarding Consumption and Consumer Credit". Journal of Economic Issues. 30 (3): 829–842. doi:10.1080/00213624.1996.11505838.

Roberts, Priscilla. 'Quis Custodiet Ipsos Custodes?' The Federal Reserve System's Founding Fathers and Allied Finances in the First World War", Business History Review (1998) 72: 585–603.

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.