The crisis damaged the credibility of the second Major ministry in handling of economic matters. The ruling Conservative Party suffered a landslide defeat five years later at the 1997 general election and did not return to power until 2010. The rebounding of the UK economy in the years following Black Wednesday has been attributed to the depreciation of sterling and the replacement of its currency tracking policy with an inflation targeting monetary stability policy.[1][2]

When the ERM was set up in 1979, the United Kingdom declined to join. This was a controversial decision, as the Chancellor of the Exchequer, Geoffrey Howe, was staunchly pro-European. His successor, Nigel Lawson, whilst not at all advocating a fixed exchange rate system, nevertheless so admired the low inflationary record of West Germany as to become, by the mid-eighties, a self-styled "exchange-rate monetarist", one viewing the sterling–Deutschmark exchange rate as at least as reliable a guide to domestic inflation– and hence to the setting of interest rates– as any of the various M0-M3 measures beloved of those he labelled as "Simon Pure" monetarists. He justified this by pointing to the dependable strength of the Deutsche Mark and the reliably anti-inflationary management of the Mark by the Bundesbank, both of which he explained by citing the lasting impact in Germany of the disastrous hyperinflation of the inter-war Weimar Republic. Thus, although the UK had not joined the ERM, at Lawson's direction (and with Prime Minister Margaret Thatcher's reluctant acquiescence), from early 1987 to March 1988 the Treasury followed a semi-official policy of "shadowing" the Deutsche Mark.[3] Matters came to a head in a clash between Lawson and Thatcher's economic adviser Alan Walters, when Walters claimed that the Exchange Rate Mechanism was "half baked".[4]

This led to Lawson's resignation as Chancellor; he was replaced by former Treasury Chief Secretary John Major who, with Douglas Hurd, the then Foreign Secretary, convinced the Cabinet to sign Britain up to the ERM in October 1990, effectively guaranteeing that the UK Government would follow an economic and monetary policy preventing the exchange rate between the pound and other member currencies from fluctuating by more than 6%. On 8 October 1990, Thatcher entered the pound into the ERM at DM2.95 to £1. Hence, if the exchange rate ever neared the bottom of its permitted range, DM2.773 (€1.4178 at the DM/Euro conversion rate), the government would be obliged to intervene. In 1989, the UK had inflation three times the rate of Germany, higher interest rates at 15%, and much lower labour productivity than France and Germany, which indicated the UK's different economic state in comparison to other ERM countries.[5]

From the beginning of the 1990s, high German interest rates, set by the Bundesbank to counteract inflationary effects related to excess expenditure on German reunification, caused significant stress across the whole of the ERM. The UK and Italy had additional difficulties with their double deficits, while the UK was also hurt by the rapid depreciation of the United States dollar– a currency in which many British exports were priced– that summer. Issues of national prestige and the commitment to a doctrine that the fixing of exchange rates within the ERM was a pathway to a single European currency inhibited the adjustment of exchange rates. In the wake of the rejection of the Maastricht Treaty by the Danish electorate in a referendum in the spring of 1992, and an announcement that there would be a referendum in France as well, those ERM currencies that were trading close to the bottom of their ERM bands came under pressure from foreign exchange traders.[6]

In the months leading up to Black Wednesday, among many other currency traders, George Soros had been building a huge short position in sterling that would become immensely profitable if the currency fell below the lower band of the ERM. Soros believed the rate at which the United Kingdom was brought into the Exchange Rate Mechanism was too high, inflation was too high (triple the German rate), and British interest rates were hurting their asset prices.[7]

The currency traders act

The UK government attempted to prop up the depreciating pound to avoid withdrawal from the monetary system the country had joined only two years earlier. John Major authorised the spending of billions of pounds worth of foreign currency reserves to buy up sterling being sold on the currency markets. These measures failed to prevent the pound falling below its minimum level in the ERM. The Treasury took the decision to defend sterling's position, believing that to devalue would promote inflation.[8]

Remarks by Bundesbank President Helmut Schlesinger triggered the attack on the pound.[citation needed] An interview of Schlesinger by the Wall Street Journal was reported by the German financial paper Handelsblatt.[9] On the evening of Tuesday, 15 September 1992, the headline was already circulating. Schlesinger said he thought he was speaking off the record. He told the journalist that "a more comprehensive realignment" of currencies would be needed, following a recent devaluation of the Italian lira.[10] Schlesinger later wrote that he stated a fact and this could not have triggered the crisis.[11] This remark hugely increased pressure on the pound leading to large sterling sales.[12]

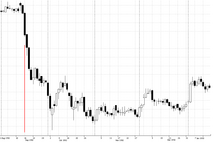

Currency traders began a massive sell-off of pounds on Wednesday, 16 September 1992. The Exchange Rate Mechanism required the Bank of England to accept any offers to sell pounds. However, the Bank of England only accepted orders during the trading day. When the markets opened in London the next morning, the Bank of England began their attempt to prop up their currency, as decided by Norman Lamont, the chancellor of the exchequer, and Robin Leigh-Pemberton, governor of the Bank of England. They began accepting orders of £300million twice before 8:30am, but to little effect.[13] The Bank of England's intervention was ineffective because traders were dumping pounds far faster. The Bank of England continued to buy, and traders continued to sell, until Lamont told Prime Minister John Major that their pound purchasing was failing to produce results.[14]

At 10:30am on 16 September, the British government announced an increase in the base interest rate, from an already high 10%, to 12% to tempt speculators to buy pounds. Despite this and a promise later the same day to raise base rates again to 15%, dealers kept selling pounds, convinced that the government would not keep its promise. By 7:00pm that evening, Lamont announced Britain would leave the ERM and rates would remain at the new level of 12%; however, on the next day the interest rate was back to 10%.[14]

It was later revealed that the decision to withdraw had been agreed at an emergency meeting during the day between Lamont, Major, foreign secretary Douglas Hurd, president of the Board of Trade Michael Heseltine, and home secretary Kenneth Clarke (the latter three all being staunch pro-Europeans as well as senior Cabinet ministers),[15] and that the interest rate hike to 15% had only been a temporary measure to prevent a rout in the pound that afternoon.[16]

Aftermath

Other ERM countries such as Italy, whose currencies had breached their bands during the day, returned to the system with broadened bands or with adjusted central parities.[17]

Some commentators, following Norman Tebbit, took to referring to ERM as an "Eternal Recession Mechanism"[18] after the UK fell into recession during the early 1990s. While many people in the UK recall Black Wednesday as a national disaster that permanently affected the country's international prestige, some Conservatives claim that the forced ejection from the ERM was a "Golden Wednesday"[19] or "White Wednesday",[20] the day that paved the way for an economic revival, with the Conservatives handing Tony Blair's New Labour a much stronger economy in 1997 than had existed in 1992[20] as the new economic policy swiftly devised in the aftermath of Black Wednesday led to re-establishment of economic growth with falling unemployment and inflation.[21]Monetary policy switched to inflation targeting.[22][23]

The Conservative Party government's reputation for economic excellence had been damaged to the extent that the electorate was more inclined to support a claim of the opposition of the time– that the economic recovery ought to be credited to external factors, as opposed to government policies implemented by the Conservatives. The Conservatives had recently won the 1992 general election, and the Gallup poll for September showed a small lead of 2.5% for the Conservative Party. By the October poll, following Black Wednesday, their share of the intended vote in the poll had plunged from 43% to 29%.[24] The Conservative government then suffered a string of by-election defeats which saw its 21-seat majority eroded by December 1996. The party's performances in local government elections were similarly dismal during this time, while Labour made huge gains.

Black Wednesday was a major factor in the Conservatives losing the 1997 general election to Labour,[citation needed] who won by a landslide under the leadership of Tony Blair. The Conservatives failed to gain significant ground at the 2001 general election under the leadership of William Hague, with Labour winning another landslide majority. The Conservatives did not take Government again until David Cameron led them to victory in the 2010 general election, 13 years later. Five years later in 2015, the party won its first overall majority 23 years after its last in 1992, five months before the crisis.

In 1997, the UK Treasury estimated the cost of Black Wednesday at £3.14billion,[26] which was revised to £3.3billion in 2005, following documents released under the Freedom of Information Act (earlier estimates placed losses at a much higher range of £13–27billion).[27] Trading losses in August and September made up a minority of the losses (estimated at £800million) and the majority of the loss to the central bank arose from non-realised profits of a potential devaluation. Treasury papers suggested that, had the government maintained $24billion foreign currency reserves and the pound had fallen by the same amount, the UK might have made a £2.4billion profit on sterling's devaluation.[28][29]

↑ Marsh, David; Keegan, William; Roberts, Richard (15 September 2017). Six Days in September: Black Wednesday, Brexit and the making of Europe. OMFIF Press. ISBN9780995563636.

Eichengreen, Barry; Naef, Alain (2022). "Imported or Home Grown? The 1992-3 EMS Crisis". Journal of International Economics. Cambridge, MA. doi:10.3386/w29488. Our analysis focuses on a neglected factor in the crisis: the role of the weak dollar in intra-EMS tensions.

The Treaty on European Union, commonly known as the Maastricht Treaty, is the foundation treaty of the European Union (EU). Concluded in 1992 between the then-twelve member states of the European Communities, it announced "a new stage in the process of European integration" chiefly in provisions for a shared European citizenship, for the eventual introduction of a single currency, and for common foreign and security policies, and a number of changes to the European institutions and their decision taking procedures, not least a strengthening of the powers of the European Parliament and more majority voting on the Council of Ministers. Although these were seen by many to presage a "federal Europe", key areas remained inter-governmental with national governments collectively taking key decisions. This constitutional debate continued through the negotiation of subsequent treaties, culminating in the 2007 Treaty of Lisbon.

Norman Stewart Hughson Lamont, Baron Lamont of Lerwick, is a British politician and former Conservative MP for Kingston-upon-Thames. He served as Chancellor of the Exchequer from 1990 until 1993. He was created a life peer in 1998. Lamont was a supporter of the Eurosceptic organisation Leave Means Leave.

The global financial system is the worldwide framework of legal agreements, institutions, and both formal and informal economic action that together facilitate international flows of financial capital for purposes of investment and trade financing. Since emerging in the late 19th century during the first modern wave of economic globalization, its evolution is marked by the establishment of central banks, multilateral treaties, and intergovernmental organizations aimed at improving the transparency, regulation, and effectiveness of international markets. In the late 1800s, world migration and communication technology facilitated unprecedented growth in international trade and investment. At the onset of World War I, trade contracted as foreign exchange markets became paralyzed by money market illiquidity. Countries sought to defend against external shocks with protectionist policies and trade virtually halted by 1933, worsening the effects of the global Great Depression until a series of reciprocal trade agreements slowly reduced tariffs worldwide. Efforts to revamp the international monetary system after World War II improved exchange rate stability, fostering record growth in global finance.

Sterling is the currency of the United Kingdom and nine of its associated territories. The pound is the main unit of sterling, and the word pound is also used to refer to the British currency generally, often qualified in international contexts as the British pound or the pound sterling.

The European Exchange Rate Mechanism (ERM II) is a system introduced by the European Economic Community on 1 January 1999 alongside the introduction of a single currency, the euro as part of the European Monetary System (EMS), to reduce exchange rate variability and achieve monetary stability in Europe.

The Central Bank of Ireland is the Irish member of the Eurosystem and had been the monetary authority for Ireland from 1943 to 1998, issuing the Irish pound. It is also the country's main financial regulatory authority, and since 2014 has been Ireland's national competent authority within European Banking Supervision.

In public finance, a currency board is a monetary authority which is required to maintain a fixed exchange rate with a foreign currency. This policy objective requires the conventional objectives of a central bank to be subordinated to the exchange rate target. In colonial administration, currency boards were popular because of the advantages of printing appropriate denominations for local conditions, and it also benefited the colony with the seigniorage revenue. However, after World War II many independent countries preferred to have central banks and independent currencies.

The Reserve Bank of Australia (RBA) is Australia's central bank and banknote issuing authority. It has had this role since 14 January 1960, when the Reserve Bank Act 1959 removed the central banking functions from the Commonwealth Bank.

In macroeconomics and modern monetary policy, a devaluation is an official lowering of the value of a country's currency within a fixed exchange-rate system, in which a monetary authority formally sets a lower exchange rate of the national currency in relation to a foreign reference currency or currency basket. The opposite of devaluation, a change in the exchange rate making the domestic currency more expensive, is called a revaluation. A monetary authority maintains a fixed value of its currency by being ready to buy or sell foreign currency with the domestic currency at a stated rate; a devaluation is an indication that the monetary authority will buy and sell foreign currency at a lower rate.

The five economic tests were the criteria defined by the UK treasury under Gordon Brown that were to be used to assess the UK's readiness to join the Economic and Monetary Union of the European Union (EMU), and so adopt the euro as its official currency. In principle, these tests were distinct from any political decision to join.

The European Monetary System (EMS) was a multilateral adjustable exchange rate agreement in which most of the nations of the European Economic Community (EEC) linked their currencies to prevent large fluctuations in relative value. It was initiated in 1979 under then President of the European Commission Roy Jenkins as an agreement among the Member States of the EEC to foster monetary policy co-operation among their Central Banks for the purpose of managing inter-community exchange rates and financing exchange market interventions.

Quantitative easing (QE) is a monetary policy action where a central bank purchases predetermined amounts of government bonds or other financial assets in order to stimulate economic activity. Quantitative easing is a novel form of monetary policy that came into wide application after the financial crisis of 2007–2008. It is used to mitigate an economic recession when inflation is very low or negative, making standard monetary policy ineffective. Quantitative tightening (QT) does the opposite, where for monetary policy reasons, a central bank sells off some portion of its holdings of government bonds or other financial assets.

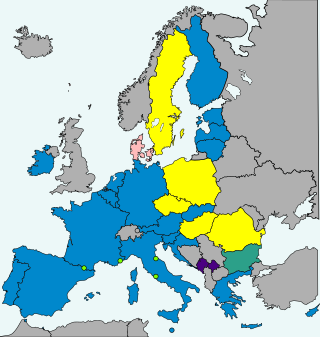

The euro came into existence on 1 January 1999, although it had been a goal of the European Union (EU) and its predecessors since the 1960s. After tough negotiations, the Maastricht Treaty entered into force in 1993 with the goal of creating an economic and monetary union (EMU) by 1999 for all EU states except the UK and Denmark.

The United Kingdom did not seek to adopt the euro as its official currency for the duration of its membership of the European Union (EU), and secured an opt-out at the euro's creation via the Maastricht Treaty in 1992, wherein the Bank of England would only be a member of the European System of Central Banks.

Denmark uses the krone as its currency and does not use the euro, having negotiated the right to opt out from participation under the Maastricht Treaty of 1992. In 2000, the government held a referendum on introducing the euro, which was defeated with 53.2% voting no and 46.8% voting yes. The Danish krone is part of the ERM II mechanism, so its exchange rate is tied to within 2.25% of the euro.

The Central Bank of Trinidad and Tobago is the central bank of Trinidad and Tobago.

The Lawson Boom was the macroeconomic conditions prevailing in the United Kingdom at the end of the 1980s, which became associated with the policies of Margaret Thatcher's Chancellor of the Exchequer, Nigel Lawson.

The United States dollar is the official currency of the United States and several other countries. The Coinage Act of 1792 introduced the U.S. dollar at par with the Spanish silver dollar, divided it into 100 cents, and authorized the minting of coins denominated in dollars and cents. U.S. banknotes are issued in the form of Federal Reserve Notes, popularly called greenbacks due to their predominantly green color.

The 1976 sterling crisis was a currency crisis in the United Kingdom. Inflation, a balance of payments deficit, a public spending deficit, and the 1973 oil crisis were contributors.

The 1972 United Kingdom budget was a budget delivered by Anthony Barber, the Chancellor of the Exchequer, on 21 March 1972. The budget is remembered for its large tax cuts, and led to high inflation and demands for higher wages, as well as the 1976 sterling crisis when the UK government was forced to ask the International Monetary Fund for financial help. It also led the Conservative Party to abandon "Post-war consensus" policies.

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.