Marcos Administration (1981–1985)

The tax system under the Marcos administration was generally regressive as it was heavily dependent on indirect taxes. Indirect taxes and international trade taxes accounted for about 35% of total tax revenue, while direct taxes only accounted for 25%. Government expenditure for economic services peaked during this period, focusing mainly on infrastructure development, with about 33% of the budget spent on capital outlays. In response to the higher global interest rates and to the depreciation of the peso, the government became increasingly reliant on domestic financing to finance fiscal deficit. The government also started liberalizing tariff policy during this period by enacting the initial Tariff Reform Program, which narrowed the tariff structure from a range of 100%–0% to 50%–10%, and the Import Liberalization Program, which aimed at reducing or eliminating tariffs and realigning indirect taxes. [22] [23] [24]

Corazon Aquino (1986–1992)

During the final years of the Marcos administration, from 1981 to 1985, the overall revenue effort averaged 11.7 percent while the tax effort averaged 10.3 percent. The tax system can be characterized as heavily dependent on indirect taxes and, therefore, regressive and weak.

Recognizing the inherent weaknesses of the tax system of Ferdinand Marcos, Corazon Aquino, a few months after she took power in 1986, reformed the tax system. Under a revolutionary government, Aquino exercised executive and legislative powers and overhauled the weak tax system with virtually no resistance. The 1986 tax reform program (TRP) aimed to simplify the tax system, make revenues more responsive to economic activity, promote horizontal equity, and promote growth by correcting existing taxes that impaired business incentives.

The dual tax schedules were unified on the personal income tax system, with the lower 0-35 percent schedule adopted for both compensation and professional incomes. To minimize revenue loss and preserve the relative burden of individuals, ceilings on allowable business deductions were proposed and adopted. Unfortunately, this complementary measure was not fully implemented due to intense lobbying by various professional groups. Passive incomes were taxed at the uniform rate of 20%, rendering passive income taxation neutral concerning investment decisions involving bank deposits and royalty-generating ventures. Personal exemptions were increased to adjust for inflation and to eliminate the taxation of those earning below the poverty threshold income. Married taxpayers were allowed to file separate returns, which lowered the tax burden on married couples by removing the effects of the progressive rates on their combined incomes.

The tax on corporations was simplified. A uniform rate of 35 percent on corporate income replaced the two-tiered corporate tax structure. Tax on inter-corporate dividends was eliminated, and the tax on dividends was phased out gradually over three years. The exemptions from income taxes of franchise grantees were withdrawn. The imposition of an income tax on franchise grantees put this previously favored group on an equal footing with similarly situated individuals or firms. Uniform franchise taxes were imposed on similar types of utilities.

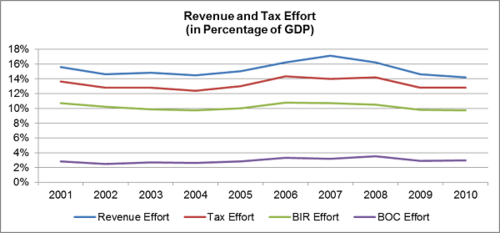

As a result of the 1986 tax reform program, average tax effort rose to 13.1 percent during the Aquino administration (1986–1992) and to 16.2 percent during the Ramos administration (1993–1998). Revenue effort rose steadily until the next round of tax reforms. Tax effort increased from 10.7% in 1985 to 15.4% in 1992, then peaked at 17.0% in 1997. The share of direct taxes to total taxes increased while that of trade taxes decreased. Income taxes could have performed better, and the tax system's fairness enhanced, had BIR implemented fully the approved reform imposing ceilings on allowable deductions. Overall responsiveness of the tax system to changes in economic activity improved from an average of 0.9% from 1980–1985 to an average of 1.5% from 1986 to 1991. The buoyancy coefficient for import duties rose from an average of 0.5% before the reform to an average of 1.89% from 1986 to 1991. [22]

Estrada Administration (1999–2000)

President Estrada, who assumed office at the height of the Asian financial crisis, faced a large fiscal deficit, which was mainly attributed to the sharp deterioration in the tax effort (as a result of the 1997 CTRP: increased tax incentives, narrowing of VAT base and lowering of tariff walls) and higher interest payments given the sharp depreciation of the peso during the crisis. The administration also had to pay P60 billion worth of accounts payables left unpaid by the Ramos administration to contractors and suppliers. Public spending focused on social services, with spending on basic education reaching its peak. To finance the fiscal deficit, Estrada created a balance between domestic and foreign borrowing. [22] [23]

Arroyo Administration (2002–2009)

The Arroyo administration in 2001 inherited a poor fiscal position that was attributed to weakening tax effort (still resulting from the 1997 CTRP) and rising debt servicing costs (due to peso depreciation). Large fiscal deficits and heavy losses for monitored government corporations lingered from 2001 to 2004 as her caretaker administration struggled to reverse downward trends. Following her election in 2004, the national debt-to-GDP ratio reached a high of 79% in that year, before dropping every year thereafter to 57.5% by 2009, her last full year in office. Lesser roads and bridges and other infrastructure were built during the Arroyo administration compare to the previous three administrations. Educational spending likewise increased from only Ps 9.3 Billion in 2001 to Ps 22.7 Billion by 2009. The cost of medicines was brought down by as much as 50% as a result of the Cheaper Medicines Act and the opening of Botikas ng Bayan and Botikas ng Barangay, while the ground-breaking conditional cash transfers (CCT) program was adapted from Latin America to stimulate positive behaviors among the poor. As a result, the Arroyo administration contributed to ever-declining levels in self-rated poverty, from a high of 68% at the start of the Ramons administration, to around 50% at the end of the Arroyo one. Much of the fuel for government activism came from an expanded value-added tax (from 10% to 12%) in 2005 (see final reports of various Cabinet agencies concerned), which with other fiscal reforms paved the way for successive sovereign credit rating upgrades by the time Arroyo stepped down in June 2010. These fiscal reforms complemented conservative liquidity management by the Central Bank, allowing the peso, for the first time ever, to close even stronger at the end of a presidential term than at the start.