A central bank, reserve bank, or monetary authority is the institution that manages the currency, money supply, and interest rates of a state or formal monetary union, and oversees their commercial banking system. In contrast to a commercial bank, a central bank possesses a monopoly on increasing the monetary base in the state, and also generally controls the printing/coining of the national currency, which serves as the state's legal tender. A central bank also acts as a lender of last resort to the banking sector during times of financial crisis. Most central banks also have supervisory and regulatory powers to ensure the solvency of member institutions, to prevent bank runs, and to discourage reckless or fraudulent behavior by member banks.

In finance and economics, a monetary authority is the entity which controls the money supply of a given currency, often with the objective of controlling inflation, interest rates, real GDP or the unemployment rate. With its monetary tools, a monetary authority is able to effectively influence the development of the short-term interest rates for that currency, but can also influence other parameters which control the cost and availability of money.

A currency, in the most specific sense is money in any form when in use or circulation as a medium of exchange, especially circulating banknotes and coins. A more general definition is that a currency is a system of money in common use, especially for people in a nation. Under this definition, US dollars (US$), pounds sterling (£), Australian dollars (A$), European euros (€), Russian rubles (₽) and Indian Rupees (₹) are examples of currencies. These various currencies are recognized as stores of value and are traded between nations in foreign exchange markets, which determine the relative values of the different currencies. Currencies in this sense are defined by governments, and each type has limited boundaries of acceptance.

Reserves of SDRs, forex and gold in 2006Foreign exchange reserves minus external debt

In a strict sense, foreign-exchange reserves should only include foreign banknotes, foreign bank deposits, foreign treasury bills, and short and long-term foreign government securities.[2] However, the term in popular usage also adds gold reserves, special drawing rights (SDRs), and International Monetary Fund (IMF) reserve positions. This broader figure is more readily available, but it is more accurately termed official international reserves or international reserves.

A banknote is a type of negotiable promissory note, made by a bank, payable to the bearer on demand. Banknotes were originally issued by commercial banks, which were legally required to redeem the notes for legal tender when presented to the chief cashier of the originating bank. These commercial banknotes only traded at face value in the market served by the issuing bank. Commercial banknotes have primarily been replaced by national banknotes issued by central banks.

A gold reserve was the gold held by a national central bank, intended mainly as a guarantee to redeem promises to pay depositors, note holders, or trading peers, during the eras of the gold standard, and also as a store of value, or to support the value of the national currency.

Special drawing rights are supplementary foreign-exchange reserve assets defined and maintained by the International Monetary Fund (IMF). The SDR is the unit of account for the IMF, and is not a currency per se. SDRs instead represent a claim to currency held by IMF member countries for which they may be exchanged. The SDR was created in 1969 to supplement a shortfall of preferred foreign-exchange reserve assets, namely gold and the U.S. dollar.

Foreign-exchange reserves are called reserve assets in the balance of payments and are located in the capital account. Hence, they are usually an important part of the international investment position of a country. The reserves are labeled as reserve assets under assets by functional category. In terms of financial assets classifications, the reserve assets can be classified as Gold bullion, Unallocated gold accounts, Special drawing rights, currency, Reserve position in the IMF, interbank position, other transferable deposits, other deposits, debt securities, loans, equity (listed and unlisted), investment fund shares and financial derivatives, such as forward contracts and options. There is no counterpart for reserve assets in liabilities of the International Investment Position. Usually, when the monetary authority of a country has some kind of liability, this will be included in other categories, such as Other Investments. [3] In the Central Bank's Balance Sheet, foreign exchange reserves are assets, along with domestic credit.

The balance of payments, also known as balance of international payments and abbreviated B.O.P. or BoP, of a country is the record of all economic transactions between the residents of the country and the rest of the world in a particular period of time. These transactions are made by individuals, firms and government bodies. Thus the balance of payments includes all external visible and non-visible transactions of a country. It is an important issue to be studied, especially in international financial management field, for a few reasons.

In macroeconomics and international finance, the capital account is one of two primary components of the balance of payments, the other being the current account. Whereas the current account reflects a nation's net income, the capital account reflects net change in ownership of national assets.

A security is a tradable financial asset. The term commonly refers to any form of financial instrument, but its legal definition varies by jurisdiction. In some jurisdictions the term specifically excludes financial instruments other than equities and fixed income instruments. In some jurisdictions it includes some instruments that are close to equities and fixed income, e.g., equity warrants. In some countries and languages the term "security" is commonly used in day-to-day parlance to mean any form of financial instrument, even though the underlying legal and regulatory regime may not have such a broad definition.

Official international reserves assets allow a central bank to purchase the domestic currency, which is considered a liability for the central bank (since it prints the money or fiat currency as IOUs). Thus, the quantity of foreign exchange reserves can change as a central bank implements monetary policy,[4] but this dynamic should be analyzed generally in the context of the level of capital mobility, the exchange rate regime and other factors. This is known as Trilemma or Impossible trinity. Hence, in a world of perfect capital mobility, a country with fixed exchange rate would not be able to execute an independent monetary policy.

An IOU is usually an informal document acknowledging debt. An IOU differs from a promissory note in that an IOU is not a negotiable instrument and does not specify repayment terms such as the time of repayment. IOUs usually specify the debtor, the amount owed, and sometimes the creditor. IOUs may be signed or carry distinguishing marks or designs to ensure authenticity. In some cases, IOUs may be redeemable for a specific product or service rather than a quantity of currency, constituting a form of scrip.

Monetary policy is the process by which the monetary authority of a country, typically the central bank or currency board, controls either the cost of very short-term borrowing or the money supply, often targeting inflation or the interest rate to ensure price stability and general trust in the currency.

In finance, an exchange rate is the rate at which one currency will be exchanged for another. It is also regarded as the value of one country’s currency in relation to another currency. For example, an interbank exchange rate of 114 Japanese yen to the United States dollar means that ¥114 will be exchanged for each US$1 or that US$1 will be exchanged for each ¥114. In this case it is said that the price of a dollar in relation to yen is ¥114, or equivalently that the price of a yen in relation to dollars is $1/114.

A central bank that implements a fixed exchange rate policy may face a situation where supply and demand would tend to push the value of the currency lower or higher (an increase in demand for the currency would tend to push its value higher, and a decrease lower) and thus the central bank would have to use reserves to maintain its fixed exchange rate. Under perfect capital mobility, the change in reserves is a temporary measure, since the fixed exchange rate attaches the domestic monetary policy to that of the country of the base currency. Hence, in the long term, the monetary policy has to be adjusted in order to be compatible with that of the country of the base currency. Without that, the country will experience outflows or inflows of capital. Fixed pegs were usually used as a form of monetary policy, since attaching the domestic currency to a currency of a country with lower levels of inflation should usually assure convergence of prices.

In economics, supply is the amount of a resource that firms, producers, labourers, providers of financial assets, or other economic agents are willing and able to provide to the marketplace or directly to another agent in the marketplace. Supply can be in currency, time, raw materials, or any other scarce or valuable object that can be provided to another agent. This is often fairly abstract. For example in the case of time, supply is not transferred to one agent from another, but one agent may offer some other resource in exchange for the first spending time doing something. Supply is often plotted graphically with the quantity provided plotted horizontally and the price plotted vertically.

Demand is the quantity of a good that consumers are willing and able to purchase at various prices during a given period of time.

In a pure flexible exchange rate regime or floating exchange rate regime, the central bank does not intervene in the exchange rate dynamics; hence the exchange rate is determined by the market. Theoretically, in this case reserves are not necessary. Other instruments of monetary policy are generally used, such as interest rates in the context of an inflation targeting regime. Milton Friedman was a strong advocate of flexible exchange rates, since he considered that independent monetary (and in some cases fiscal) policy and openness of the capital account are more valuable than a fixed exchange rate. Also, he valued the role of exchange rate as a price. As a matter of fact, he believed that sometimes it could be less painful and thus desirable to adjust only one price (the exchange rate) than the whole set of prices of goods and wages of the economy, that are less flexible.[5]

A floating exchange rate is a type of exchange-rate regime in which a currency's value is allowed to fluctuate in response to foreign-exchange market events. A currency that uses a floating exchange rate is known as a floating currency. A floating currency is contrasted with a fixed currency whose value is tied to that of another currency, material goods or to a currency basket.

Inflation targeting is a monetary policy regime in which a central bank has an explicit target inflation rate for the medium term and announces this inflation target to the public. The assumption is that the best that monetary policy can do to support long-term growth of the economy is to maintain price stability. The central bank uses interest rates, its main short-term monetary instrument.

Milton Friedman was an American economist who received the 1976 Nobel Memorial Prize in Economic Sciences for his research on consumption analysis, monetary history and theory and the complexity of stabilization policy. With George Stigler and others, Friedman was among the intellectual leaders of the second generation of Chicago price theory, a methodological movement at the University of Chicago's Department of Economics, Law School and Graduate School of Business from the 1940s onward. Several students and young professors who were recruited or mentored by Friedman at Chicago went on to become leading economists, including Gary Becker, Robert Fogel, Thomas Sowell and Robert Lucas Jr.

Mixed exchange rate regimes ('dirty floats', target bands or similar variations) may require the use of foreign exchange operations to maintain the targeted exchange rate within the prescribed limits, such as fixed exchange rate regimes. As seen above, there is an intimate relation between exchange rate policy (and hence reserves accumulation) and monetary policy. Foreign exchange operations can be sterilized (have their effect on the money supply negated via other financial transactions) or unsterilized.

Non-sterilization will cause an expansion or contraction in the amount of domestic currency in circulation, and hence directly affect inflation and monetary policy. For example, to maintain the same exchange rate if there is increased demand, the central bank can issue more of the domestic currency and purchase foreign currency, which will increase the sum of foreign reserves. Since (if there is no sterilization) the domestic money supply is increasing (money is being 'printed'), this may provoke domestic inflation. Also, some central banks may let the exchange rate appreciate to control inflation, usually by the channel of cheapening tradable goods.

Since the amount of foreign reserves available to defend a weak currency (a currency in low demand) is limited, a currency crisis or devaluation could be the end result. For a currency in very high and rising demand, foreign exchange reserves can theoretically be continuously accumulated, if the intervention is sterilized through open market operations to prevent inflation from rising. On the other hand, this is costly, since the sterilization is usually done by public debt instruments (in some countries Central Banks are not allowed to emit debt by themselves). In practice, few central banks or currency regimes operate on such a simplistic level, and numerous other factors (domestic demand, production and productivity, imports and exports, relative prices of goods and services, etc.) will affect the eventual outcome. Besides that, the hypothesis that the world economy operates under perfect capital mobility is clearly flawed.

As a consequence, even those central banks that strictly limit foreign exchange interventions often recognize that currency markets can be volatile and may intervene to counter disruptive short-term movements (that may include speculative attacks). Thus, intervention does not mean that they are defending a specific exchange rate level. Hence, the higher the reserves, the higher is the capacity of the central bank to smooth the volatility of the Balance of Payments and assure consumption smoothing in the long term.

Reserve accumulation

After the end of the Bretton Woods system in the early 1970s, many countries adopted flexible exchange rates. In theory reserves are not needed under this type of exchange rate arrangement; thus the expected trend should be a decline in foreign exchange reserves. However, the opposite happened and foreign reserves present a strong upward trend. Reserves grew more than gross domestic product (GDP) and imports in many countries. The only ratio that is relatively stable is foreign reserves over M2.[6] Below are some theories that can explain this trend.

Theories

Signaling or vulnerability indicator

Ratios relating reserves to other external sector variables are popular among credit risk agencies and international organizations to assess the external vulnerability of a country. For example, Article IV of 2013[7] uses total external debt to gross international reserves, gross international reserves in months of prospective goods and nonfactor services imports to broad money, broad money to short-term external debt, and short-term external debt to short-term external debt on residual maturity basis plus current account deficit. Therefore, countries with similar characteristics accumulate reserves to avoid negative assessment by the financial market, especially when compared to members of a peer group.

Precautionary aspect

Reserves are used as savings for potential times of crises, especially balance of payments crises. Original fears were related to the current account, but this gradually changed to also include financial account needs.[8] Furthermore, the creation of the IMF was viewed as a response to the need of countries to accumulate reserves. If a specific country is suffering from a balance of payments crisis, it would be able to borrow from the IMF. However, the process of obtaining resources from the Fund is not automatic, which can cause problematic delays especially when markets are stressed. Therefore, the fund only serves as a provider of resources for longer term adjustments. Also, when the crisis is generalized, the resources of the IMF could prove insufficient. After the 2008 crisis, the members of the Fund had to approve a capital increase, since its resources were strained.[9] Moreover, after the 1997 Asian crisis, reserves in Asian countries increased because of doubt in the IMF reserves.[10] Also, during the 2008 crisis, the Federal Reserve instituted currency swap lines with several countries, alleviating liquidity pressures in dollars, thus reducing the need to use reserves.

External trade

Most countries engage in international trade, so to ensure no interruption, reserves are important. A rule usually followed by central banks is to hold the equivalency of at least three months of imports in foreign currency. Also, an increase in reserves occurred when commercial openness increased (part of the process known as globalization). Reserve accumulation was faster than that which would be explained by trade, since the ratio has increased to several months of imports. Furthermore, the external trade factor explains why the ratio of reserves in months of imports is closely watched by credit risk agencies.

Financial openness

The opening of a financial account of the balance of payments has been important during the last decade. Hence, financial flows such as direct investment and portfolio investment became more important. Usually financial flows are more volatile that enforce the necessity of higher reserves. Moreover, holding reserves, as a consequence of the increasing of financial flows, is known as Guidotti–Greenspan rule that states a country should hold liquid reserves equal to their foreign liabilities coming due within a year. For example, international wholesale financing relied more on Korean banks in the aftermath of the 2008 crisis, when the Korean Won depreciated strongly, because the Korean banks' ratio of short-term external debt to reserves was close to 100%, which exacerbated the perception of vulnerability.[11]

Exchange rate policy

Reserve accumulation can be an instrument to interfere with the exchange rate. Since the first General Agreement on Tariffs and Trade (GATT) of 1948 to the foundation of the World Trade Organization (WTO) in 1995, the regulation of trade is a major concern for most countries throughout the world. Hence, commercial distortions such as subsidies and taxes are strongly discouraged. However, there is no global framework to regulate financial flows. As an example of regional framework, members of the European Union are prohibited from introducing capital controls, except in an extraordinary situation. The dynamics of China's trade balance and reserve accumulation during the first decade of the 2000 was one of the main reasons for the interest in this topic. Some economists are trying to explain this behavior. Usually, the explanation is based on a sophisticated variation of mercantilism, such as to protect the take-off in the tradable sector of an economy, by avoiding the real exchange rate appreciation that would naturally arise from this process. One attempt[12] uses a standard model of open economy intertemporal consumption to show that it is possible to replicate a tariff on imports or a subsidy on exports by closing the current account and accumulating reserves. Another[13] is more related to the economic growth literature. The argument is that the tradable sector of an economy is more capital intense than the non-tradable sector. The private sector invests too little in capital, since it fails to understand the social gains of a higher capital ratio given by externalities (like improvements in human capital, higher competition, technological spillovers and increasing returns to scale). The government could improve the equilibrium by imposing subsidies and tariffs, but the hypothesis is that the government is unable to distinguish between good investment opportunities and rent seeking schemes. Thus, reserves accumulation would correspond to a loan to foreigners to purchase a quantity of tradable goods from the economy. In this case, the real exchange rate would depreciate and the growth rate would increase. In some cases, this could improve welfare, since the higher growth rate would compensate the loss of the tradable goods that could be consumed or invested. In this context, foreigners have the role to choose only the useful tradable goods sectors.

Intergenerational savings

Reserve accumulation can be seen as a way of "forced savings". The government, by closing the financial account, would force the private sector to buy domestic debt in the lack of better alternatives. With these resources, the government buys foreign assets. Thus, the government coordinates the savings accumulation in the form of reserves. Sovereign wealth funds are examples of governments that try to save the windfall of booming exports as long-term assets to be used when the source of the windfall is extinguished.

Costs

There are costs in maintaining large currency reserves. Price fluctuations in exchange markets result in gains and losses in the purchasing power of reserves. In addition to fluctuations in exchange rates, the purchasing power of fiat money decreases constantly due to devaluation through inflation. Therefore, a central bank must continually increase the amount of its reserves to maintain the same power to manipulate exchange rates. Reserves of foreign currency provide a small return in interest. However, this may be less than the reduction in purchasing power of that currency over the same period of time due to inflation, effectively resulting in a negative return known as the "quasi-fiscal cost". In addition, large currency reserves could have been invested in higher yielding assets.

Several calculations have been attempted to measure the cost of reserves. The traditional one is the spread between government debt and the yield on reserves. The caveat is that higher reserves can decrease the perception of risk and thus the government bond interest rate, so this measures can overstate the cost. Alternatively, another measure compares the yield in reserves with the alternative scenario of the resources being invested in capital stock to the economy, which is hard to measure. One interesting[6] measure tries to compare the spread between short term foreign borrowing of the private sector and yields on reserves, recognizing that reserves can correspond to a transfer between the private and the public sectors. By this measure, the cost can reach 1% of GDP to developing countries. While this is high, it should be viewed as an insurance against a crisis that could easily cost 10% of GDP to a country. In the context of theoretical economic models it is possible to simulate economies with different policies (accumulate reserves or not) and directly compare the welfare in terms of consumption. Results are mixed, since they depend on specific features of the models.

A case to point out is that of the Swiss National Bank, the central bank of Switzerland. The Swiss franc is regarded as a safe haven currency, so it usually appreciates during market's stress. In the aftermath of the 2008 crisis and during the initial stages of the Eurozone crisis, the Swiss franc (CHF) appreciated sharply. The central bank resisted appreciation by buying reserves. After accumulating reserves during 15 months until June 2010, the SNB let the currency appreciate. As a result, the loss with the devaluation of reserves just in 2010 amounted to CHF 27 Billion or 5% of GDP (part of this was compensated by the profit of almost CHF6 Billion due to the surge in the price of gold).[14] In 2011, after the currency appreciated against the Euro from 1.5 to 1.1, the SNB announced a ceiling at the value of CHF 1.2. In the middle of 2012, reserves reached 71% of GDP.

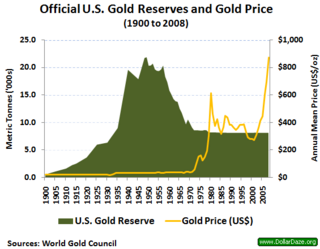

Official international reserves, the means of official international payments, formerly consisted only of gold, and occasionally silver. But under the Bretton Woods system, the US dollar functioned as a reserve currency, so it too became part of a nation's official international reserve assets. From 1944–1968, the US dollar was convertible into gold through the Federal Reserve System, but after 1968 only central banks could convert dollars into gold from official gold reserves, and after 1973 no individual or institution could convert US dollars into gold from official gold reserves. Since 1973, no major currencies have been convertible into gold from official gold reserves. Individuals and institutions must now buy gold in private markets, just like other commodities. Even though US dollars and other currencies are no longer convertible into gold from official gold reserves, they still can function as official international reserves.

Central banks throughout the world have sometimes cooperated in buying and selling official international reserves to attempt to influence exchange rates and avert financial crisis. For example, in the Baring crisis (the "Panic of 1890"), the Bank of England borrowed GBP 2 million from the Banque de France.[17] The same was true for the Louvre Accord and the Plaza Accord in the post gold-standard era.

Post Gold Standard Era

Historically, especially before the 1997 Asian financial crisis, central banks had rather meager reserves (by today's standards) and were therefore subject to the whims of the market, of which there was accusations of hot money manipulation, however Japan was the exception. In the case of Japan, forex reserves began their ascent a decade earlier, shortly after the Plaza Accord in 1985, and were primarily used as a tool to weaken the surging yen.[18] This effectively granted the United States a massive loan as they were almost exclusively invested in US Treasuries, which assisted the US to engage the Soviet Union in an arms race which ended with the latter's bankruptcy, and at the same time, turned Japan into the world's largest creditor and the US the largest debtor, as well as swelled Japan's domestic debt (Japan sold its own currency to fund the buildup of dollar based assets). By end of 1980, foreign assets of Japan were about 13% of GDP but by the end of 1989 had reached an unprecedented 62%.[18] After 1997, nations in Southeast and East Asia began their massive build-up of forex reserves, as their levels were deemed too low and susceptible to the whims of the market credit bubbles and busts. This build-up has major implications for today's developed world economy, by setting aside so much cash that was piled into US and European debt, investment had been crowded out, the developed world economy had effectively slowed to a crawl, giving birth to contemporary negative interest rates.[citation needed]

By 2007, the world had experienced yet another financial crisis, this time the US Federal Reserve organized Central bank liquidity swaps with other institutions. Developed countries authorities adopted extra expansionary monetary and fiscal policies, which led to the appreciation of currencies of some emerging markets. The resistance to appreciation and the fear of lost competitiveness led to policies aiming to prevent inflows of capital and more accumulation of reserves. This pattern was called currency war by an exasperated Brazilian authority, and again in 2016 followed the commodities collapse, Mexico had warned China of triggering currency wars.[19]

Adequacy and excess reserves

The IMF proposed a new metric to assess reserves adequacy in 2011.[20] The metric was based on the careful analysis of sources of outflow during crisis. Those liquidity needs are calculated taking in consideration the correlation between various components of the balance of payments and the probability of tail events. The higher the ratio of reserves to the developed metric, the lower is the risk of a crisis and the drop in consumption during a crisis. Besides that, the Fund does econometric analysis of several factors listed above and finds those reserves ratios are generally adequate among emerging markets.[citation needed]

Reserves that are above the adequacy ratio can be used in other government funds invested in more risky assets such as sovereign wealth funds or as insurance to time of crisis, such as stabilization funds. If those were included, Norway, Singapore and Persian Gulf States would rank higher on these lists, and United Arab Emirates' estimated $627 billion Abu Dhabi Investment Authority would be second after China. Apart from high foreign exchange reserves, Singapore also has significant government and sovereign wealth funds including Temasek Holdings (last valued at US$177 billion) and GIC Private Limited (last valued at US$320 billion).[21]

Currency substitution or dollarization is the use of a foreign currency in parallel to or instead of the domestic currency.

The global financial system is the worldwide framework of legal agreements, institutions, and both formal and informal economic actors that together facilitate international flows of financial capital for purposes of investment and trade financing. Since emerging in the late 19th century during the first modern wave of economic globalization, its evolution is marked by the establishment of central banks, multilateral treaties, and intergovernmental organizations aimed at improving the transparency, regulation, and effectiveness of international markets. In the late 1800s, world migration and communication technology facilitated unprecedented growth in international trade and investment. At the onset of World War I, trade contracted as foreign exchange markets became paralyzed by money market illiquidity. Countries sought to defend against external shocks with protectionist policies and trade virtually halted by 1933, worsening the effects of the global Great Depression until a series of reciprocal trade agreements slowly reduced tariffs worldwide. Efforts to revamp the international monetary system after World War II improved exchange rate stability, fostering record growth in global finance.

The Asian financial crisis was a period of financial crisis that gripped much of East and Southeast Asia beginning in July 1997 and raised fears of a worldwide economic meltdown due to financial contagion.

Hard currency, safe-haven currency or strong currency is any globally traded currency that serves as a reliable and stable store of value. Factors contributing to a currency's hard status might include the long-term stability of its purchasing power, the associated country's political and fiscal condition and outlook, and the policy posture of the issuing central bank.

The Bretton Woods system of monetary management established the rules for commercial and financial relations among the United States, Canada, Western European countries, Australia, and Japan after the 1944 Bretton Woods Agreement. The Bretton Woods system was the first example of a fully negotiated monetary order intended to govern monetary relations among independent states. The chief features of the Bretton Woods system were an obligation for each country to adopt a monetary policy that maintained its external exchange rates within 1 percent by tying its currency to gold and the ability of the IMF to bridge temporary imbalances of payments. Also, there was a need to address the lack of cooperation among other countries and to prevent competitive devaluation of the currencies as well.

In economics, hot money is the flow of funds from one country to another in order to earn a short-term profit on interest rate differences and/or anticipated exchange rate shifts. These speculative capital flows are called 'hot money' because they can move very quickly in and out of markets, potentially leading to market instability.

The Mexican peso crisis was a currency crisis sparked by the Mexican government's sudden devaluation of the peso against the U.S. dollar in December 1994, which became one of the first international financial crises ignited by capital flight.

The impossible trinity is a concept in international economics which states that it is impossible to have all three of the following at the same time:

The Triffin dilemma or Triffin paradox is the conflict of economic interests that arises between short-term domestic and long-term international objectives for countries whose currencies serve as global reserve currencies. This dilemma was identified in the 1960s by Belgian-American economist Robert Triffin, who pointed out that the country whose currency, being the global reserve currency, foreign nations wish to hold, must be willing to supply the world with an extra supply of its currency to fulfill world demand for these foreign exchange reserves, thus leading to a trade deficit.

The Nixon shock was a series of economic measures undertaken by United States President Richard Nixon in 1971, in response to increasing inflation, the most significant of which were wage and price freezes, surcharges on imports, and the unilateral cancellation of the direct international convertibility of the United States dollar to gold.

Currency intervention, also known as foreign exchange market intervention or currency manipulation, is a monetary policy operation. It occurs when a government or central bank buys or sells foreign currency in exchange for their own domestic currency, generally with the intention of influencing the exchange rate and trade policy.

A fixed exchange rate, sometimes called a pegged exchange rate, is a type of exchange rate regime in which a currency's value is fixed against either the value of another single currency, a basket of other currencies, or another measure of value, such as gold.

Original sin is a term in economics literature, proposed by Barry Eichengreen, Ricardo Hausmann, and Ugo Panizza in a series of papers to refer to a situation in which "most countries are not able to borrow abroad in their domestic currency."

Domestic liability dollarization (DLD) refers to the denomination of banking system deposits and lending in a currency other than that of the country in which they are held. DLD does not refer exclusively to denomination in US dollars, as DLD encompasses accounts denominated in internationally traded "hard" currencies such as the British pound sterling, the Swiss franc, the Japanese yen, and the Euro.

Fear of floating refers to situations where a country prefers a fixed exchange rate to a floating exchange rate regime. This is more relevant in emerging economies, especially when they suffered from financial crisis in last two decades. In foreign exchange markets of the emerging market economies, there is evidence showing that countries who claim they are floating their currency, are actually reluctant to let the nominal exchange rate fluctuate in response to macroeconomic shocks. In the literature, this is first convincingly documented by Calvo and Reinhart with "fear of floating" as the title of one of their papers in 2000. Since then, this widespread phenomenon of reluctance to adjust exchange rates in emerging markets is usually called "fear of floating". Most of the studies on "fear of floating" are closely related to literature on costs and benefits of different exchange rate regimes.

1 2 Rodrik, Dani. "The social cost of foreign exchange reserves." International Economic Journal 20.3 (2006): 253-266.

↑ "Archived copy"(PDF). Archived(PDF) from the original on 8 September 2013. Retrieved 15 February 2013.CS1 maint: Archived copy as title (link) Colombia2013 Article IV Consultation

↑ Bastourre, Diego, Jorge Carrera, and Javier Ibarlucia. "What is driving reserve accumulation? A dynamic panel data approach." Review of International Economics 17.4 (2009): 861–877.

↑ Jeanne, Olivier. "Capital Account Policies and the Real Exchange Rate." No. w18404. National Bureau of Economic Research, 2012.

↑ Korinek, Anton, and Luis Serven. "Undervaluation through foreign reserve accumulation: static losses, dynamic gains." World Bank Policy Research Working Paper Series, Vol (2010).

Eichengreen, Barry. Exorbitant Privilege: The Rise and Fall of the Dollar and the Future of the International Monetary System. Oxford University Press, USA, 2011.

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.