Taxes in Germany are levied at various government levels: the federal government, the 16 states (Länder), and numerous municipalities (Städte/Gemeinden). The structured tax system has evolved significantly, since the reunification of Germany in 1990 and the integration within the European Union, which has influenced tax policies. Today, income tax and Value-Added Tax (VAT) are the primary sources of tax revenue. These taxes reflect Germany's commitment to a balanced approach between direct and indirect taxation, essential for funding extensive social welfare programs and public infrastructure. The modern German tax system accentuate on fairness and efficiency, adapting to global economic trends and domestic fiscal needs.

The legal basis for taxation is established in the German Constitution (Grundgesetz), which lays out the basic principles governing tax law. Most taxation is decided by the federal government and the states together, some are allocated solely at the federal level (e.g., customs), some are allocated to the states (excise taxes), and districts and municipalities may enact their own tax laws. Notwithstanding the division of tax law jurisdiction, in practice, 95% of all taxes are imposed at the federal level.

Single individual who earn less than 11,604 € (2024) gross per annum pay no taxes in Germany.[1] For a single taxpayer, the applicable income tax rate starts at 14% and rises progressively to 42% for income above €66,760 € (2024). This progression ensures that the tax burden aligns with the ability to pay, reflecting principles of vertical equity. Additionally, the basic allowance (Grundfreibetrag) for 2024 is 11,604 €,[1] which means no income tax is levied on annual income below this threshold.[2]

Married couple:

Married couples benefit from a "splitting" advantage, where their combined income is split for taxation purposes, potentially halving their tax rate compared to single filers under similar income brackets. For instance, if one spouse earns €60,000 and the other €40,000, their combined income of €100,000 is split into two parts of €50,000 each for tax purposes. This results in a lower progressive tax rate being applied to each part, significantly reducing their overall tax liability.[3]

Freelancer:

A freelancer in Germany might have a different set of tax considerations, particularly regarding allowable deductions such as business expenses. If a freelancer earns €80,000 annually but has €20,000 in allowable business expenses, their taxable income reduces to €60,000. The tax calculation would then apply to this adjusted figure, taking into account the progressive tax rates and any applicable tax credits for self-employed individuals.[4]

Corporate tax:

Companies in Germany are subject to corporate tax at a flat rate of 15%. For a company with an annual profit of €200,000, the corporate tax payable would be €30,000. Additionally, the solidarity surcharge and trade tax can alter the effective tax rate, depending on the municipality.[5]

Terminology and concepts

Look up Steuer in Wiktionary, the free dictionary.

The general definition of the term "tax" is contained in the first sentence of paragraph 3(1) of the Tax Code: "Taxes are monetary payments that do not constitute consideration for a particular service and are imposed by a public authority for the purpose of generating revenue on all those who meet the criteria to which the law attaches the obligation to pay; the generation of revenue may be an ancillary purpose."[2]

Look up Grundgesetz in Wiktionary, the free dictionary.

The Grundgesetz (lit. 'Basic Law') is the common term for the German Constitution in German, known in full as the Grundgesetz für die Bundesrepublik Deutschland, or 'Basic Law for the Federal Republic of Germany'.

General legal or administrative jurisdictions in Germany fall roughly into four levels: federal (Bund), state (Land, pluralLänder), district (Kreis, plural Kreise), and municipality (Gemeinde, plural Gemeinden), and tax authority follows this same pattern, although it is concentrated chiefly at the federal and state level.

The fiscal administration (Finanzverwaltung), also known as tax administration: Steuerverwaltung) in Germany is the part of public administration which is responsible for the determination and collection of taxes. The Federal Central Tax Office (Bundeszentralamt für Steuern, or BZSt) is the federal agency responsible for administering certain sections of the country's tax code. It was spun off from the Federal Ministry of Finance in 2006.[7]

Taxation principles

The German Constitution lays down the principles governing taxation in the following articles:

Wikisource has original text related to this article:

When calculating the tax liability, the taxpayer may claim tax-reducing personal characteristics, e.g. special expenses, extraordinary burdens. The ability-to-pay principle includes vertical tax equity, which means that everyone should be taxed according to their ability to pay. Everyone should bear the tax burden to the extent that they are able to do so. This is also the reason for progressive taxation.

Equality in taxation

Tax equity intends the vertical and horizontal tax equity. Horizontal tax equity implies that taxpayers with the same level of income should be taxed equally.

Vertical tax equity implies that taxpayers with different incomes should be taxed according to their ability to pay.Leistungsfähigkeitsprinzip

The federation and the states decide together on most of the tax law. Formally, the states can decide that there is no federal law. In practice, there are federal laws for all taxation issues. (Art. 105 para. 2 Grundgesetz)

The municipalities and the districts (Kreise) can decide on some minor local taxes like the taxation of dogs (Hundesteuer).

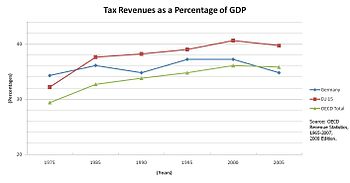

Tax revenues 1975–2005 as a percentage of GDP for Germany, in comparison to the OECD and the EU 15

So even if Germany is a federal state, 95% of all taxes are imposed on a federal level. The income of these taxes is allocated by the federation and the states as following (Constitution, Art. 106):

The federation receives exclusively the revenue of:

Customs

Taxes on alcopops, cars, distilled beverages, coffee, mineral oil products, sparkling wine, electricity, tobacco, and insurance

Supplement on income taxes so-called solidarity surcharge (Solidaritätszuschlag)

The municipalities and/or districts receive exclusively the revenue of:

Real property tax

Taxes on other beverages, dogs, and inns.

Most of the revenue is earned by income tax and VAT. The revenues of these taxes are distributed between the federation and the states by quota. The municipalities receive a part of the income of the states. In addition, there is a compensation between rich and poor states (Constitution, Art. 107).

Structure and basic information

Administration

Germany's fiscal administration is divided into federal tax authorities and state tax authorities. The local tax offices (Finanzamt, plural Finanzämter) belong to the latter. They administer the "shared taxes" for the federation and the states and process the tax returns. The number of tax offices in Germany totals around 650.

As a result of discussions in 2006 and 2009 between federation and states (the so-called Föderalismusreform[de; fr]), the Federation also administers some taxes. The competent authority is the Federal Central Tax Office (Bundeszentralamt für Steuern, or BZSt) which is also competent authority for certain applications of tax refund from abroad. Since 2009, the BZSt allocates an identification number for tax purposes to every taxable person.

Jurisdiction

There is at least one Fiscal Court in every state (Berlin and Brandenburg, however, share a court located in Cottbus). Appeals against the decisions of the Fiscal Courts are heard by the Federal Fiscal Court (Bundesfinanzhof) in Munich.

Fiscal code

The common rules and procedures applying to all taxes are contained in the fiscal code (Abgabenordnung) as so-called general tax law. The individual tax laws regulate in which case tax is incurred.

The German Fiscal Code (Abgabenordnung, AO) is divided into nine parts, which essentially reflect the chronological sequence of the taxation procedure. The introductory provisions explain the basic tax concepts that apply to all taxes.

Tax identification numbers

From 2009 onward, every German resident receives a personal tax identification number. Businesses also receive a business identification number (Wirtschaftssteuer-Identifikationsnummer).[8] The competent authority is the Federal Central Tax Office (Bundeszentralamt für Steuern).[9] A taxpayer in Germany gets two types of tax numbers - Tax ID (Steueridentifikationsnummer) and Tax Number (Steuernummer). Tax ID is issued by the Federal Central Tax Office and the Tax Number is assigned by the local tax office (Finanzamt).[10]

Tax revenue

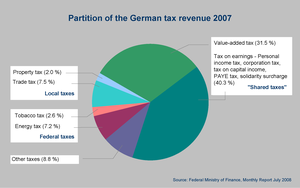

German tax revenue 2007

According to the latest Revenue Statistics report published by the Organisation for Economic Co-operation and Development (OECD), Germany has seen a significant increase in its tax-to-GDP ratio. In 2021, the ratio stood at 39.5%, up 1.6 percentage points from 37.9% in 2020. This increase is higher than the average for OECD countries, which rose from 33.6% to 34.1% between 2020 and 2021.

Looking at the longer-term trend, Germany’s tax-to-GDP ratio has been steadily increasing since 2000 when it was at 36.4%. In comparison, the OECD average has also risen over the same period, from 32.9% in 2000 to 34.1% in 2021. The highest tax-to-GDP ratio recorded in Germany was in 2021 at 39.5%, while the lowest was in 2004 at 34.3%.[11]

During 2021 Germany was ranked 10th in OECD tax-to-GDP ratio out of 38 OECD countries.

Compared to the OECD average, Germany’s tax structure is distinguished by significantly higher revenues from social security contributions and personal income taxes, profits and gains. On the other hand, Germany has a lower proportion of revenues from corporate income and gains taxes, property taxes, value-added taxes (VAT), and goods and services taxes (excluding VAT/GST). Additionally, Germany does not generate any revenue from payroll taxes.[3]

Community taxes made up the largest share of the total at EUR 626.0 billion, or 82.3 percent. Compared with the previous year, they increased by 15.0 percent or EUR 81.8 billion. The main contributors were taxes on sales (+31.3 billion euros) and income- and profit-related tax types such as corporate income tax (+17.9 billion euros), assessed income tax (+13.4 billion euros) and payroll tax (+9.1 billion euros).Radware Captcha Page

Tax revenue is distributed to Germany's three levels of government: the federation, the states, and the municipalities. All of these are jointly entitled to the most important types of tax (i.e., value-added tax and income tax). For this reason, these taxes are also known as shared taxes. Tax revenue is distributed proportionately using a formula prescribed in the German Constitution.

Individuals who are residents in Germany or have their normal place of abode there have full income tax liability. This type of tax liability is known as unlimited tax liability and is based on the definition of habitual residence. A person is resident where he or she stays under circumstances that indicate that he or she is staying at that place or in that area on more than a temporary basis. Habitual residence within the scope of the Tax Act shall always be deemed to be a continuous stay of more than six months from the beginning; short-term interruptions shall not be taken into consideration. This is clarified in paragraph 9 of the Tax Code.

All the income earned by these persons both at home and abroad is subject to German tax (principle of world income). The principle of world income indicates that the taxpayer's taxation extends to all their world income, regardless of where the income was earned. The principle is stated in the Income Tax Guidelines (EStR). The Income Tax Guidelines (EStR) are not binding on the taxpayer, but only on the tax authorities.

Persons who neither have a residence in Germany nor stay in Germany for more than 183 days, but who receive certain domestic income pursuant to Section 49 income tax law (EStG), have limited income tax liability subject to Section 1 (4) income tax law (EStG).

Types of income

For the purposes of charging income tax in Germany, earnings are divided into seven different types of income. A distinction is made between:

Income from agriculture and forestry

Income from business operations

Income from self-employed work

Income from employed work

Income from capital

Income from letting property

Miscellaneous income.

If a taxpayer's income does not fall into any of these categories, then it is not subject to income tax. This includes winnings at a lottery, for example.

Income tax

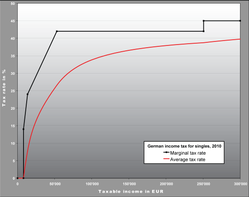

German income tax rate in 2010 as a function of taxable income

The rate of income tax in Germany ranges from 0% to 45%. The German income tax is a progressive tax, which means that the average tax rate (i.e., the ratio of tax and taxable income) increases monotonically with increasing taxable income. Moreover, the German taxation system warrants that an increase in taxable income never results in a decrease of the net income after taxation. The latter property is due to the fact that the marginal tax rate (i.e., the tax paid on one euro additional taxable income) is always below 100%. The marginal tax rate brackets and the resulting average tax rate of the income tax are depicted in the graph to the right; in the 14-24% and 24-42% brackets, the rate increases linearly with income within the bracket. The tax liability of married couples who file jointly is assessed on half their total income, and the result from applying the tax tariff is multiplied by two afterwards. Due to the progressive tax schedule, this always more favorable than taxing each spouse separately. This splitting advantage increases with the income difference between both spouses.

The assessment basis for income tax is the taxable income. The calculations are governed by the income tax scale. Every year, an income tax table is compiled that shows employees the amount of income tax deducted briefly. This is regulated in §32a EStG (Income Tax Act).

There is a distinction between the wage tax and the income tax in German income tax legislation. The wage tax is a collection form of the income tax.

The wage tax is levied for all employees. As soon as further income is added or income from a self-employed activity is present, one speaks of income tax. This is due to the different designations "wage" for employees and "income" for all other income.

Income tax comprises a total of seven types of income, including salaries and income from freelance and self-employed activities. Wage tax and capital gains tax are therefore not independent types of tax, but collection forms of income tax.

One additional fact about the income tax system in Germany is that it is assessed on the net income of an individual or married couple, which includes a deduction for the social security contributions they pay. In 2019, this averages somewhere around 19.7% of personal income. So, in reality, the marginal tax rates displayed below only apply to ~80.3% of the income of an individual up to 55,960 euros. This in turn decreases the income tax liability for the average employee by around 4%, although it still is possible to pay an effective rate of nearly 45% if one's income is high enough.

Finally, there is a tax refund that averages around 1000 euros. As an employee, you can declare income-related expenses in your tax declaration. These are "expenses incurred to acquire, secure and maintain income" (Section 9 (1) sentence 1 of the German Income Tax Act, EStG). These include "all expenses caused by the occupation" (R 9.1 para. 1 sentence 1 Wage Tax Guidelines, LStR). This means that expenses incurred due to a profession can be claimed in the tax return. Specifically, these can be the following expenses, among others: work equipment, job application costs, costs for work and official clothing (if this is typical work clothing e.g. doctor's coat, safety shoes or uniforms), contributions to professional associations, account management fees and expenses for travel between home and the first place of work. The employee lump sum is only available for income from non-self-employment. It cannot therefore be applied to income from self-employment, renting or leasing.

On top of income tax, the so-called solidarity surcharge (Solidaritätszuschlag or Soli) is levied at a rate of 5.5% of the income tax for higher incomes. The solidarity surcharge was introduced in 1991 and, since 1995, has been justified with the additional costs of the German reunification. These include the debts and pension obligations of the East German government, as well as the costs of upgrading infrastructure and environmental remediation in the new states of Germany. From January 2021, the application of the solidarity surcharge tax has been significantly reduced. For single individuals with an income tax burden of up to €17,543 (equivalent to a taxable income of €65,500) and married couples filing jointly with an income tax burden of up to €35,086 (equivalent to a taxable income of €131,000), no solidarity surcharge is levied. Above these thresholds, a sliding scale is applied until the full 5.5% rate is reached for single individuals with a taxable income of €101,400 and married couples filing jointly with a taxable income of €202,800.[12]

Above this threshold, the solidarity surcharge rate averages at 5.5%.

For example, if €10,000 income tax result from a certain annual taxable income, a solidarity surcharge of €550 will be levied on top. As a result, the tax payer owes the taxation office €10,550.

The solidarity surcharge was introduced as a supplementary tax to income tax and corporate income tax and must in principle be paid by all employed persons.

The reasons for the introduction of the solidarity surcharge were financial compensation for:

Additional burdens from the Gulf conflict

Structurally weak countries in Central, Eastern and Southern Europe

Costs of German reunification

In addition to the solidarity surcharge, members of officially recognized churches are required to pay church tax as a surcharge on their income tax. The rate varies between 8% and 9%, depending on the federal state in which the individual resides.[12]

Tax on benefits in kind

Every individual has to pay for any perks or benefits they receive from an employer, which includes, for example, the use of a car. This applies to private car usage too if the car is owned by a company or a self-employed individual. In the case of cars, this is based on either a log-book method or a flat-rate method, which depends on the gross-list-price of a car rounded down to the next €100. This means the original list-price without any reduction or discount at the time of first original use, whether or not the car is used or some years old. VAT and every extra features (e.g. GPS, leather seats etc.) need to be included. Tax is paid on one per cent of this basis as the taxable amount every month.

The Federal Central Tax Office (BZSt) is responsible for administering insurance and fire protection tax in the whole nation.

Insurance tax is a transaction tax, which is linked to legal and commercial transactions. In the case of insurance tax, the payment of the insurance premium for an insurance relationship is taxed, not the insurance contract or coverage. It does not matter if the insurance relationship is established by contract or otherwise (e.g. by law or membership in an association). An agreement between several individuals or associations to jointly bear losses or damages that may be subject to insurance is also considered an insurance contract. The debtor of the insurance tax is the policyholder, but the insurer must pay the tax on their behalf.

In contrast, the fire protection tax is not a true transaction tax. The receipt of the insurance premium from insurance is taxed, not the payment. The debtor of the tax is the insurer, who must also pay it.[13]

Since insurance and fire protection taxes are registration taxes, the payment or the receipt due date of the insurance premium must be calculated, declared, and paid to the Federal Central Tax Office by the tax debtor himself within 15 days of the end of each registration period.

The basis of assessment for the insurance and fire protection tax is the insurance premium (§5 Insurance Tax Act, §3 Fire Protection Tax Act). The respective tax rates are based on §6 of the Insurance Tax Act. according to §4 of the Fire Protection Tax Act.

The insurance premium is any benefit that is to be made to the insurer for the establishment and implementation of the insurance relationship. These include e.g. also, premiums, contributions, advance contributions, advances, entrance fees, additional contributions, levies, fees for the issuance of the insurance policy, and other ancillary costs.

Calculation and payment

The tax debtor must calculate, declare, and pay the insurance and fire protection tax to the Federal Central Tax Office within 15 days of the end of each registration period based on the payment or receipt or due date of the insurance premium.

The assessment basis for insurance and fire protection tax is the insurance premium (§5 Insurance Tax Act, §3 Fire Protection Tax Act). The respective tax rates are determined by §6 of the Insurance Tax Act or §4 of the Fire Protection Tax Act.

Insurance premium refers to any benefit provided to the insurer for establishing and implementing the insurance relationship. This includes premiums, contributions, advance contributions, advances, entrance fees, additional contributions, levies, fees for issuing the insurance policy, and other ancillary costs.[13]

Withholding taxes

Tax on income from employed work and tax on capital income are both retained by being deducted at source (pay-as-you-earn tax, wages tax, or withholding tax). Here, an amount of tax is retained directly by the employer or by the bank before the earnings are paid out.

The taxation at source for employment income will be carried out based in taxation classes based on the personal status. The tax classes essentially differ by the exemption threshold that is applied. Married couples face a decision of opting for a combination of classes III/V or IV/IV. In the former case, the spouse with higher earnings receives the twice the basic exemption rate, while the second earner is taxed at very low earnings. In the latter case, both spouses are taxed based on the standard exemption rate. The choice of tax classes only matters for the withholding tax and hence for the income that is immediately at disposal. After the income tax assessment, which happens a few months after the tax year has ended, the tax rebate is not affected by the choice of tax class. Beyond, employers are also liable to deduct the contributions to the social security system at source.

class I = single, living in a registered civil partnership, divorced, widowed or married, unless they fall under tax category II, III or IV.

class II = single but is entitled to single parent allowance.

class III = married and spouse does not earn wages, or the spouse earns a wage but is classified under tax category V by request of both spouses, or to widowed workers for the calendar year following that of the spouse's death if both were residing in Germany and were not separated on the day of the spouse's death.

class IV = married, both spouses earn a wage, reside in Germany, and are not separated.

class V = married but one of the spouses, at both spouses' request, is classified under tax category III.

class VI = workers receiving multiple wages from more than one employer, in order for wage tax to be withheld for the second and any additional employment contracts.

The taxation at source for capital income will be done with a flat tax rate of 25% (add solidarity surcharge of 5.5% of the amount of tax and, if applicable, church tax).

Deductions

German income tax law allows a considerable number of taxpayers' costs to be deducted from income when computing taxable income. This applies to costs immediately related to earnings. Apart from this, other costs are also deductible, e.g., certain insurance payments, costs incurred by sickness, costs for home help, and maintenance payments.

For the years 2020 to 2022, employees working at home can deduct EUR 5 per calendar day worked from home (increasing to EUR 6 from the assessment period 2023), up to a maximum of EUR 600 annually. This means that a maximum of 120 days can be claimed (increasing to 210 days from the assessment period 2023).[5]

Taxation Deduction of Foreign Income Earners

Domestic income earned by foreign artists, athletes, licensees, and supervisory board members as defined in Section 49 of the Income Tax Act (EStG) is subject to limited tax liability. This income is taxed through a special procedure known as the tax deduction procedure under § 50a EStG.

In this procedure, the domestic debtors of the remuneration, such as organizers and licensees, are required to withhold taxes from their payments to the foreign remuneration creditors and pay the taxes to the Federal Central Tax Office (BZSt) for discharge. To pay the tax, they must electronically submit a tax return to the BZSt and pay the calculated taxes. This procedure is similar to wage tax deductions, where employers must withhold and pay taxes for their employees. [14]

Requests for discharge

Refund and Exemption of Withholding Tax for Foreign Remuneration Creditors Foreign remuneration creditors may apply for a refund of the withholding tax paid by a remuneration debtor on their behalf under § 50a EStG. This is possible if the relevant double taxation agreement (DBA) exempts the remuneration from German taxation in whole or in part. Alternatively, the remuneration creditor can apply for an exemption certificate before payment. If the remuneration debtor has this certificate at the time of payment, they do not have to withhold any taxes or only at a lower rate.[14]

Tax return

The obligation to file an income tax return does not apply to everybody. For example, single assessed tax payers who exclusively earn income subject to withholding tax are exempt from this obligation, because their tax debt is deemed to be at least settled by the withholding tax. Nevertheless, any person having full tax liability is allowed to file a tax return, taking into account the tax already withheld at the source and possible deductions. In many cases, this may result in a tax refund.

In Germany, married couples are required to file joint tax returns unless they are legally separated or one spouse requests to file separately (then legal action can be taken).[15]

Income tax for non-residents

Individuals who are neither resident of Germany nor have their normal place of abode there are only liable to pay tax in Germany if they earn income there which has a close domestic (German) context. This includes in particular income from real estate in Germany or from a permanent establishment in Germany.

Tax obligations for non-resident German property owners

Every non-resident German property owner is subject to a personal levy on income derived from their German property. Non-resident real estate investors are also obliged to file a German property tax return each year.[16]

Tax residency status and property ownership

In order to be considered a resident in Germany, an individual must spend over 183 days in the country during a two-year period. It is important to note that German real estate owners are liable for taxation regardless of their tax residency status.

Germany has reached tax treaties with about 90 countries to avoid double taxation. These agreements fall under public international law and aim to avoid both double taxation and double non-taxation of individuals and companies. The basic structure of the double taxation agreements which Germany has signed follows the Model Tax Convention drawn up by the OECD.

In addition to the double taxation agreements in the field of income and wealth taxes, there are special double taxation agreements in the field of inheritance and gift taxes and motor vehicle tax, as well as agreements in the field of legal and administrative assistance and the exchange of information. In particular, the exchange of information between tax authorities is an important element in detecting and combating tax evasion and avoidance and in enabling accurate taxation.Doppelbesteuerungsabkommen und andere Abkommen im Steuerbereich - Bundesfinanzministerium - Themen

Social Security Contributions

Employment income earned in Germany is subject to different insurance contributions covering health, pension, nursing and unemployment insurance. Contributions are levied as a percent of income until a certain ceiling shared equally between employee and employer. Table of contributions for 2018:[17]

Insurance policy

Yearly ceiling

Employer%

Employee%

Pension insurance

West: 78,000.00 €/ East: 69,600.00 €

9.30%

9.30%

Unemployment insurance

West: 78,000.00 €/ East: 69,600.00 €

1.5%

1.5%

Nursing insurance

53,100.00 €

0.775–1.275%

1.275%–1.775%

Health insurance

53,100.00 €

7.3%

7.3%

Additional employee contribution depending on health insurance company

Corporation tax is charged first and foremost on corporate enterprises, in particular public and private limited companies, as well as other corporations such as e.g. cooperatives, associations and foundations. Sole proprietorships and partnerships are not subject to corporation tax: profits earned by these set-ups are attributed to their individual partners and then taxed in the context of their personal income tax bills.

Corporations domiciled or managed in Germany are deemed to have full corporation tax liability. This means that their domestic and foreign earnings are all taxable in Germany. Some corporate enterprises are exempted from corporation tax, e.g. charitable foundations, Church institutions, and sports clubs.

As of 1 January 2008, Germany's corporation tax rate is 15%. Counting both the solidarity surcharge (5.5% of corporation tax) and trade tax (averaging 14% as of 2008), tax on corporations in Germany is just below 30%.

Assessment base

The assessment base for the corporation tax charged is the revenue which the corporate enterprise has earned during the calendar year. Taxable profits are determined using the result posted in the annual accounts (balance sheet and Income statement) drawn up under the Commercial Code. What is deemed income under tax law sometimes diverges from the way earnings are determined under commercial law, in which case tax law provisions prevail.

Dividends

When dividends are paid to an individual person, capital yield tax at a rate of 25% is charged. Since 1 January 2009, this tax is final for individuals who are residents of Germany. Solidarity surcharge is also imposed on capital yields tax.

When dividends are paid to an enterprise with full corporation tax liability, the recipient business is largely exempted from paying tax on these revenues. In its tax assessment, merely 5% of the dividends are added to profits as non-deductible operating expenses. The same applies if a taxable corporate enterprise sells shares in another company.

Deducting tax from dividends paid by a subsidiary with full tax liability to a foreign parent domiciled in the EU is waived on certain conditions, e.g., the parent company has to have a direct holding in the subsidiary of at least 15%.

Integrated fiscal units (group taxation)

Under German tax law, separate companies may be treated as integrated fiscal units for tax purposes (Organschaft). In an integrated fiscal unit, a legally independent company (the controlled company) agrees under a profit and loss pooling agreement to become dependent on another business (the controlling company) in financial, economic and organisational terms. The controlled company undertakes to pay over its entire profits to the controlling company. Another requirement is that the controlling company has to hold the majority of voting rights in the controlled company.

In tax terms, recognition of a fiscal unit means that the income of the controlled company is allocated to the controlling company. This provides an opportunity to balance profits and losses within the integrated fiscal unit.

Trade tax

Entrepreneurs engaging in business operations are subject to trade tax (Gewerbesteuer) as well as income tax/corporation tax. In contrast to the latter, trade tax is charged by the local authorities or municipalities, who are entitled to the entire amount. The rate levied is fixed by each local authority separately within the range of rates prescribed by the central government. As from 1 January 2008, the rate averages 14% of profits subject to trade tax.

Assessment procedure

The business entity has to file the trade tax return with the tax office, like its other tax returns. Taking any allowances into account, the local tax office (Finanzamt) calculates the trade earnings and then gives the applicable figure for a trade tax assessment to the local authority collecting the tax. The underlying profit base, as well as the book-tax differences for the local trade tax jurisdictions, may differ from that used for the corporation tax. On the basis of the collecting rate (Hebesatz) in force in its area, the local authority calculates the trade tax payable.

Unincorporated enterprises

One-man businesses and members of a partnership may deduct a large portion of trade tax from their personal income tax bill.

Incorporated enterprises

As from 1 January 2008, corporate entities may no longer deduct trade tax from their taxable profits.

Real property tax

Municipalities levy a tax on real property (Grundsteuern). The tax rates vary because they depend on the decision of the local parliament. The tax is payable every quarter. In 2018, the German Constitutional Court ruled the current property tax as not in line with the constitution. This is because properties are taxed based on their value from the early 1960s (1930s in East Germany), violating the horizontal equity principle.

Real property transfer tax

Transfers of real property are taxable (Grunderwerbsteuer). The vendee and the vendor are common debtors of the tax. In general the vendee has to pay the tax. The tax rate is defined by the individual states. In general the tax rate is 3.5%, but all states except Bavaria and Saxony have increased it since 2011. Most states now have a tax rate of 4.5% or 5%; the highest are North Rhine-Westphalia, Saarland and Schleswig-Holstein with 6.5%.

Real estate investors are also impacted by the speculation tax (Spekulationssteuer). This tax applies to gains generated on real estate investments, if sold less than ten years after purchase. Depreciation deductions of prior years are added to the sales price of the home, to derive a higher taxable gain.[18]

Vendor profit from real estate sales in Germany is considered capital gains if the real estate has been held for less than ten years.[19]

For example, if an individual purchased an apartment in 2015 and rented it out, and now wants to sell it for a profit, they would have to pay taxes on their profit if they sell the property before the speculative period ends in 2025.[20]

Inheritance and gift tax

A single law regulates both inheritance tax and gift tax, requiring the payment of rates from 7% to 50% both on transfers following death and on gifts among the living. In contrast to the U.S. estate tax, the inheritance and gift tax is paid by the recipient of the transfer. The tax rates depend on the amount and on the relationship between donor and recipient. There are also substantial exemption rates, amounting to €500,000 for transfers between married partners and €400,000 for transfers to own (step-)children. Deductions as high as 100% apply to cases such as family houses and the possessions of entrepreneurs.

Capital gains tax

In Germany there is no special capital gains tax. Only under certain conditions gains from private disposal may be taxed. Since 1 January 2009 Germany levies a final tax (Abgeltungsteuer) amounting to 25% plus 5.5% solidarity surcharge. This may take effect like a capital gains tax for resident persons e.g. disposal of shares. The Abgeltungsteuer replaces the earlier half revenue procedure[de] that had been in effect in Germany since 2001.

Recipients residing abroad can be relieved through exemption from tax deduction or reimbursement of already withheld and remitted capital gains tax in a written application procedure.

Relief can also be obtained through the data carrier procedure (DTV). The DTV is only suitable for financial institutions that regularly submit a large number of applications for reimbursement of German capital gains tax (KapSt) and solidarity surcharge (SolZ) on behalf of their customers residing abroad.[21]

Consumption taxes

Value-added tax

As a matter of principle, all services and products generated in Germany by a business entity are subject to value-added tax (VAT). The German VAT is part of the European Union value added tax system.

Exemptions

Certain goods and services are exempted from value-added tax by law; this applies for German and foreign businesses alike.

For example, the following are exempted from German value-added tax:

services provided by certain professional groups (e.g. doctors)

financial services (e.g. granting loans)

letting real estate in the long-term

cultural services provided to the public (e.g. by public theatres, museums, zoos, etc.),

value-added by certain institutions providing general education or vocational training

services provided in an honorary or voluntary capacity.

Tax rate

The rate of value-added tax rate generally in force in Germany is 19%.[23] A reduced tax rate of 7% applies e.g. on sales of certain foods, books and magazines and transports.

Due to COVID-19, the government accepted a lowering to 16% (reduced: 5%) from 1 July 2020 until 31 December 2020 for the rates.[24] The overall intended effect of the reduction, stimulating the economy, was marginal[citation needed][25] and further diminished by the costs of adjusting prices (which not all businesses did), changing sales and billing systems, and doing that twice in such a short time.

Payment of the tax

Within ten days of the end of each calendar quarter, the business entity has to send the tax office an advance return in which it has to give its own computation of the tax for the preceding calendar quarter. The amount payable is the value-added tax it has invoiced, minus any amounts of deductible input tax. Deductible input tax is the value-added tax which the entrepreneur has been charged by other business entities.

The amount thus calculated has to be paid to the tax office through an advance. This means that the amount due must be paid in full before the next fiscal quarter. Larger businesses have to file the advance return every month. For entrepreneurs who have only just taken up professional or commercial operations, the monthly reporting period likewise applies during the first calendar year and in the year after that.

At the end of the calendar year, the entrepreneur has to file an annual tax return in which it has again calculated the tax.

Small businesses

Entrepreneurs whose turnover (plus the value-added tax on it) has not exceeded EUR 17,500 in the preceding calendar year and is not expected to exceed EUR 50,000 in the current year (small enterprises), do not need to pay value-added tax. However, these small enterprises are not allowed to deduct the input tax they have been billed.

VAT refund for travelers

Travelers from non-EU member states can shop VAT-free in Germany. To be eligible for VAT exemption, you must meet the following conditions:

You must have a residence in a non-EU member state and be able to prove this to the seller with personal documents (passport, identity card or other border crossing document).

You must not have a residence permit that allows you to stay in Germany for more than 3 months.

The total value of the delivery, including VAT, must exceed 50 euros.

You must carry the goods with you in your personal luggage within 3 months of purchase.

Personal luggage includes items that you carry with you when crossing the border, such as hand luggage or items in a vehicle you use, as well as checked hand luggage. Forwarded or shipped baggage does not qualify.

Since January 1, 2020, only purchases with an invoice amount of 50.01 euros or more can lead to a VAT exemption for the supplying retailer. Since the customs administration only confirms the export by a person resident in a third country, a stamp imprint does not make any statement about an associated tax exemption for the trader that he can pass on to his customer.[26]

The 50 EUR value limit will be abolished when an automated confirmation of the export of goods by a person resident in the third country is possible. An IT system intended for this purpose is currently under development, but a specific date for commissioning cannot yet be named. [26]

According to the source the following are exempt from the tourist tax exemption:

services provided in Germany (for example, you have to pay for bus or train journeys, restaurant visits and hotel accommodation including German VAT)

Goods for equipping private vehicles of all kinds (e.g. bumpers, exterior mirrors, tow rope and first aid kit)

Goods for the supply of a vehicle such as fuel, engine oil or care products

An important thing to mention is that one's nationality is irrelevant, only the place of residence is decisive. For example, a Swiss citizen who lives in Germany cannot shop here tax-free.

A tax is imposed on the owners of motor vehicles. It is levied depending on the type of vehicle (car, motorcycle, commercial truck, trailer, motorhome, etc.). The tax is due annually after the registration of the vehicle. With cars, the tax is different for gasoline and diesel engines. Diesel powered cars are taxed higher. The tax amount also depends on the emissions class (Euro 1 – Euro 6), whether a diesel car has a soot particle filter, and the initial date of vehicle registration.

Initial registration

Taxation based on

Tax free CO2 threshold

– 30 June 2009

displacement in cc

–

1 July 2009 – 31 December 2011

displacement in cc + CO2 emission

120g/km

1 January 2012 – 31 December 2013

displacement in cc + CO2 emission

110g/km

1 January 2014 –

displacement in cc + CO2 emission

95g/km

Purely electric vehicles are exempt from taxes for at least five years after initial registration.[27]

Tax allowances and tax credits

Standard reliefs and work-related expenses:

Standard marital status reliefs, the tax obligation of spouses is determined using a division method.

Compute and aggregate the taxable incomes of each spouse, doubling specific allowances, then divide the total by two.

Apply the tax rate to the halved income figure.

Calculate the tax due by multiplying the tax from the second step by two.

Results: Due to progressive income taxation and disparate income levels, this method reduces the tax burden for couples compared to individual assessments, benefiting the household economically. The greatest benefit of income splitting occurs when one spouse has no taxable income, diminishing as spouses' incomes become more similar. This approach ensures that both earners face equal average and marginal tax rates, regardless of how income is distributed between them.

In 2022, tax credits are available as follows: EUR 2,628 for the first and second child, EUR 2,700 for the third child, and EUR 3,000 for the fourth and subsequent children. Parents are granted an increased tax allowance of EUR 2,810 for child support and an additional EUR 1,464 for care and educational expenses, totaling EUR 4,274. These amounts are doubled for jointly assessed parents and for single parents not receiving alimony from the other parent. If the tax credit is less than the allowance based on these figures, the tax allowance supersedes the tax credit. It is presumed that a single parent will always benefit from the doubled allowances.

In 2022, families with children also receive a one-time bonus of EUR 100 per child, which does not reduce the basic income support for jobseekers. For higher-income households, this bonus will be deducted from the child tax allowance. As of 1 January 2015, single parents are entitled to a standard additional allowance of EUR 1,908 (previously EUR 1,308), increased by EUR 240 for each additional child in the home.

Since 2020, the standard tax allowance for single parents was raised to EUR 4,008, initially as a temporary response to pandemic-related challenges through 2020 and 2021, and made permanent from 2022 onward to support single-parent families.

Deductions include social security and future provisioning expenses (e.g., life insurance), capped according to specific limits. Since 2005, the deduction process is:

Sum all contributions to pension funds (both employee and employer contributions).

Cap this total at the maximum rate of the miners’ pension insurance scheme, rounded to the nearest euro (in 2022: EUR 25,639).

Deduct a specific percentage, starting at 60% in 2005 and increasing by 2% annually to reach 100% in 2025.

The deductible amount is then reduced by the employer's tax-free contributions.

Since 1 January 2010, employees’ annual contributions to statutory health insurance (excluding sickness benefits, assumed to be 96% of total health contributions) and long-term care insurance are deductible from the tax base. If these contributions do not exceed EUR 1,900/3,800 (single/married), additional deductions are allowed for unemployment insurance and other insurance premiums up to this limit.

An increased lump-sum deduction of EUR 1,200 for work-related expenses per employed individual (until 2021: EUR 1,000). Expenses exceeding this amount are fully deductible (no ceiling). A "home office" deduction was introduced for 2020 and 2021, allowing EUR 5 per day for exclusive home working, capped at EUR 600 per year (120 working days). This deduction will continue into 2022 and is considered within the general lump-sum deduction for work-related expenses.

A lump sum allowance of EUR 36/72 (singles/couples) for special expenses, such as tax accountancy. Actual expenses exceeding this allowance are fully deductible if substantiated by the taxpayer.

A one-time lump-sum energy price allowance of EUR 300 for all working taxpayers in 2022, taxable but not reduced by social security contributions.

Financial crisis 2009

Existing depreciations e.g. for certain private housekeeping expenses and for small and medium-sized enterprises have been enhanced. A declining depreciation for movable assets has been reintroduced for two years (2009–2010). Businesses are allowed to carry back losses and to claim refund of paid corporation/income tax. As a result, they get liquidity improvement. From 2010-01-01 on the VAT tax rate concerning hotel accommodation is reduced from 19% to 7%.

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.