A Lindahl tax is a form of taxation conceived by Erik Lindahl in which individuals pay for public goods according to their marginal benefits. In other words, they pay according to the amount of satisfaction or utility they derive from the consumption of an additional unit of the public good. Lindahl taxation is designed to maximize efficiency for each individual and provide the optimal level of a public good.

Lindahl taxes can be seen as an individual's share of the collective tax burden of an economy. The optimal level of a public good is that quantity at which the willingness to pay for one more unit of the good, taken in totality for all the individuals is equal to the marginal cost of supplying that good. Lindahl tax is the optimal quantity times the willingness to pay for one more unit of that good at this quantity.[1]

History

The idea of using aggregate marginal utility in the analysis of public finance was not new in Europe. Knut Wicksell was one of the most prominent economists who studied this concept, eventually arguing that no individual should be forced to pay for any activity that does not give them utility.[2]Erik Lindahl was deeply influenced by Wicksell, who was his professor and mentor, and proposed a method for financing public goods in order to show that consensus politics is possible. As people are different in nature, their preferences are different, and consensus requires each individual to pay a somewhat different tax for every service, or good that he consumes. If each person's tax price is set equal to the marginal benefits received at the ideal service level, each person is made better off by provision of the public good and may accordingly agree to have that service level provided.

Lindahl equilibrium

A Lindahl equilibrium is a state of economic equilibrium under a Lindahl tax as well as a method for finding the optimum level for the supply of public goods or services that happens when the total per-unit price paid by each individual equals the total per-unit cost of the public good. It can be shown that an equilibrium exists for different environments.[3] Therefore, the Lindahl equilibrium describes how efficiency can be sustained in an economy with personalized prices. Leif Johansen gave the complete interpretation of the concept of "Lindahl equilibrium", which assumes that household consumption decisions are based on the share of the cost they must provide for the supply of the particular public good.[4]

This method of taxation for public goods is an equilibrium for two reasons. First, individuals are willing to pay the respective taxes for the quantity of public goods provided. Second, the cost of the public good is covered by the aggregate taxes. Therefore, the Lindahl pricing centers around the benefit principle, in which individuals are taxed based on their valuation of the benefit received from the good. This equilibrium is also the efficient level of public goods, as the social marginal benefit is equivalent to the social marginal cost.[5]

The importance of Lindahl equilibrium is that it fulfills the Samuelson condition and is therefore Pareto efficient,[3] despite the good in question being a public one. It also demonstrates how efficiency can be reached in an economy with public goods by the use of personalized prices. The personalized prices equate the individual valuation for a public good to the cost of the public good.[citation needed]

Lindahl equilibrium in an economy with only a public good

Lindahl and Samuelson defined the Lindahl equilibrium in a general economy, in which there are both public and private goods. Fain, Goel and Mungala[6] present a specialized definition, for the case in which there are only public goods.

There is a fixed budget B, and k types of divisible public goods.

The goal is to decide on an allocation x of the budget, such that x1+...+xk = B.

There are n agents; each agent i has a utility function Ui over possible allocations of the budget.

An allocation x is a Lindahl equilibrium if there exist personal price-vectors p1,...,pn such that the following two conditions hold:

For every agent i, the allocation x maximizes the utility Ui(x) subject to . That is: x is the best bundle that agent i could buy with his proportional share of the budget and his personal prices. In other words: if each agent chooses the best public bundle he can afford given his personal prices, then all agents unanimously choose the same public bundle.

The allocation x maximizes the profit, defined as . Intuitively, it is assumed that some producer can produce public goods in cost 1, and he sells them to the public; his profit is the total amount of money he gains from selling the goods in the given prices, minus the total cost of production.

The personalized price-vector pi can be interpreted as the Lindahl tax on agent i.

In a Fisher market equilibrium, there is a single price-vector for all agents, but each agent has a different bundle

In a Lindahl equilibrium, there is a personal price-vector for each agent, but all agents have the same bundle.

A Lindahl equilibrium allocation in a market of public goods has a characterization without the price-vectors.[6]:Thm.2.1 Specifically, an allocation x is a Lindahl equilibrium if and only if, for every good j, , where the inequality becomes an equality when .

Existence

Foley[7] proved that, If the utility functions have continuous derivatives, are strictly increasing, and are strictly concave, then a Lindahl equilibrium exists in the general case of mixed public and private goods, and moreover, it lies in the fractional core. However, his proof is existential and does not provide an efficient algorithm.

Manipulation

The mechanism that, given agents' utilities, computes the Lindahl equilibrium, is not strategyproof, even in the setting with only public goods. This is a special case of the free-rider problem.

Computation

Fain, Goel and Mungala[6]:Thm.2.2 present an algorithm for computing the Lindahl equilibrium using convex programming, in the special case in which agents have scalar-separablenon-satiating utilities. Particularly:

If the agents' utilities are homogeneous of degree 1 and concave, the Lindahl equilibrium allocation can be computed by maxizing the Nash welfare .[6]:Cor.2.3 Moreover, the gradient of this objective function can be computed using quadratic voting.

For more general non-satiating utility functions, the Lindahl equilibrium can be computed by maximizing a potential function, that can be seen as a regularized version of the Nash welfare.

Discrete Lindahl equilibrium

Peters, PIerczynski, Shah and Skowron[8] present an adaptation of the concept of Lindahl equilibrium to a market with indivisible public goods. In this setting, a Lindahl equilibrium may be not Pareto-efficient.

Example: there are three goods (a, b1, b2) and two voters, where Alice values a, b1 at 1 and b2 at 0, and George values a, b2 at 1 and b1 at 0. The budget of each agent is 3, and the cost of each good is 2. Producing only {a} is a Lindahl equilibrium, with prices for Alice: 2-0.009, 2-0.006, 0.001 and prices for George: 2-0.009, 0.001, 2-0.006. This is because (1) it maximizes the profit: the producer would not gain from producing b1 or b2; (2) it maximizes the agents' utilities: no agent can afford another desirable good. But {a} is not efficient, since it is dominated by {a,b1,b2}.

If the definition is strengthened to require that the total payment for each public good exactly equals its cost, then the stronger Lindahl equilibrium notion is equivalent to a concept they call strict stable priceability. A stable-priceable committee does not always exist, but extensive simulation experiments show that an "almost" stable-priceable committee almost always exists. It is possible to check in polynomial time whether a given committee is stable-priceable.

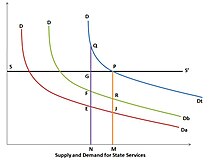

Lindahl Model

Lindahl's Model of Taxation

In the Lindahl Model, Dt represents the aggregate marginal benefit curve, which is the sum of Da and Db---the marginal benefits for the two individuals in the economy. In a Lindahl equilibrium, the optimal quantity of the public good will be where the social marginal benefit intersects the marginal cost (point P). Each individual's Lindahl tax rate will be based on their own marginal benefit curve. In this model, individual B will pay the price level at R and individual A will pay at point J.

Criticism

In theory, Lindahl pricing and taxation leads to an efficient provision of public goods. However, it requires the knowledge of the demand functions for each individual, and therefore is difficult to implement in practice. There are three main problems with the implementation of a Lindahl tax.

Preference revelation problem

When information about marginal benefits is available only from the individuals themselves, they tend to under report their valuation for a particular good. In doing this, an individual can lower his or her tax cost by under reporting the benefits derived from the public good or service. The incentive to lie is associated with the free rider problem; if an individual reports a lower benefit, he or she will pay less taxes, but only see a marginal decrease in the public good. This informational problem shows that survey-based Lindahl taxation is not incentive compatible. Incentives to understate or under report one's true benefits under Lindahl taxation resemble those of a traditional public goods game.[5]

Preference revelation mechanisms can be used to solve that problem,[9][10] although none of these has been shown to completely and satisfactorily address it. The Vickrey–Clarke–Groves mechanism is an example of this, ensuring true values are revealed and that a public good is provided only when it should be. The allocation of cost is taken as given and the consumers will report their net benefits (benefits-cost) the public good will be provided if the sum of the net benefits of all consumers is positive. If the public good is provided side payments will be made reflecting the fact that truth telling is costly. The side payments internalize the net benefit of the public good to other players. The side payments must be financed from outside the mechanism. In reality, preference revelation is difficult as the size of the population makes it costly both in terms of money and time.[11]

Preference knowledge problem

A second drawback to the Lindahl solution is that individuals may be unsure of their own valuation of a public good. Even if individuals are attempting to be honest with their willingness to pay, they may have no idea of their true value. This is especially true for public goods that individuals do not interact with on a day-to-day basis, like fireworks and national defense.[11]

Preference aggregation problem

Even if individuals know their marginal willingness to pay, and are honest in their reporting, the government can have extreme difficulties aggregating this into a social value. In situations where few individuals are affected by the public good, like the example below, aggregation can be relatively simple. However, in the case of national defense in the United States, compiling the marginal willingness to pay for this public good of each individual would be nearly impossible.[11]

We assume that there are two goods in an economy:the first one is a "public good", and the second is "everything else". The price of the public good can be assumed to be Ppublic and the price of everything else can be Pelse. Person1 will choose his bundle such that:

α*P(public)/P(else) = MRS(person1)

This is just the usual price ratio/marginal rate of substitution deal; the only change is that we multiply Ppublic by α to allow for the price adjustment to the public good. Similarly, Person2 will choose his bundle such that:

(1-ɑ)*P(public)/P(else)= MRS(person2)

Now we have both individuals' utility maximizing. We know that in a competitive equilibrium, the marginal cost ratio or price ratio should be equal to the marginal rate of transformation, or

MC(public)/MC(else)=[P(public)/P(else)]=MRT

Example

Take for example a public park, with a constant marginal cost of $15 per acre. This public park will be available to two people, Sarah and Tom.

Figure 1: Sarah's marginal willingness to pay.

Figure 1 shows Sarah's marginal willingness to pay for a public park. For the first acre of the park, Sarah is willing to pay $20. For the 80th acre, her marginal willingness to pay has decreased down to zero.

Figure 2: Tom's marginal willingness to pay.

Figure 2 shows Tom's marginal willingness to pay for a public park. Unlike Sarah, for the first acre of park he is willing to pay $40, and for the 40th acre of park he has a marginal willingness to pay of $20. For the 80th acre of park his marginal willingness to pay is zero.

Figure 3: Aggregate marginal willingness to pay.

Figure 3 shows the aggregate marginal willingness to pay for the public park. As seen on the figure, Sarah and Tom together are willing to pay $60 for the first acre of park. This is higher than the marginal cost of the first acre ($15) and therefore this first acre of park should be produced. Sarah and Tom together are willing to pay $45 for the 20th acre, and $30 for the 40th acre, which are both again above the marginal cost of $15. The marginal cost curve intersects their aggregate willingness to pay curve at the 60th acre, when they are together willing to pay the $15 marginal cost. Thus, the Lindahl equilibrium involves charging Sarah $5 and Tom $10 for each of the 60 acres of park.[5]

↑ Roberts, Donald John (1974-02-01). "The Lindahl solution for economies with public goods". Journal of Public Economics. 3 (1): 23–42. doi:10.1016/0047-2727(74)90021-8. ISSN0047-2727.

1 2 3 Backhaus, Jürgen Georg, Wagner, Richard E. (2004). Handbook of Public Finance. ISBN978-1-4020-7863-7.{{cite book}}: CS1 maint: multiple names: authors list (link)

Lindahl, Erik (1958) [1919], "Just taxation – A positive solution", in Musgrave, R. A.; Peacock, A. T. (eds.), Classics in the Theory of Public Finance, London: Macmillan.

Salanié, Bernard (2000). "5.2.3 The Lindahl equilibrium". Microeconomics of market failures (English translation of the (1998) French Microéconomie: Les défaillances dumarché (Economica, Paris)ed.). Cambridge,MA: MITPress. pp.74–75. ISBN978-0-262-19443-3.

Microeconomics is a branch of economics that studies the behavior of individuals and firms in making decisions regarding the allocation of scarce resources and the interactions among these individuals and firms. Microeconomics focuses on the study of individual markets, sectors, or industries as opposed to the economy as a whole, which is studied in macroeconomics.

In welfare economics, a Pareto improvement formalizes the idea of an outcome being "better in every possible way". A change is called a Pareto improvement if it leaves at least one person in society better-off without leaving anyone else worse off than they were before. A situation is called Pareto efficient or Pareto optimal if all possible Pareto improvements have already been made; in other words, there are no longer any ways left to make one person better-off, without making some other person worse-off.

In economics, utility is a measure of a certain person's satisfaction from a certain state of the world. Over time, the term has been used with at least two meanings.

In economics, an externality or external cost is an indirect cost or benefit to an uninvolved third party that arises as an effect of another party's activity. Externalities can be considered as unpriced components that are involved in either consumer or producer market transactions. Air pollution from motor vehicles is one example. The cost of air pollution to society is not paid by either the producers or users of motorized transport to the rest of society. Water pollution from mills and factories is another example. All (water) consumers are made worse off by pollution but are not compensated by the market for this damage. A positive externality is when an individual's consumption in a market increases the well-being of others, but the individual does not charge the third party for the benefit. The third party is essentially getting a free product or service. An example of this might be the apartment above a bakery receiving some free heat in winter. The people who live in the apartment do not compensate the bakery for this benefit.

This aims to be a complete article list of economics topics:

In economics, a public good is a good that is both non-excludable and non-rivalrous. Use by one person neither prevents access by other people, nor does it reduce availability to others. Therefore, the good can be used simultaneously by more than one person. This is in contrast to a common good, such as wild fish stocks in the ocean, which is non-excludable but rivalrous to a certain degree. If too many fish were harvested, the stocks would deplete, limiting the access of fish for others. A public good must be valuable to more than one user, otherwise, its simultaneous availability to more than one person would be economically irrelevant.

The theory of consumer choice is the branch of microeconomics that relates preferences to consumption expenditures and to consumer demand curves. It analyzes how consumers maximize the desirability of their consumption, by maximizing utility subject to a consumer budget constraint. Factors influencing consumers' evaluation of the utility of goods include: income level, cultural factors, product information and physio-psychological factors.

Welfare economics is a field of economics that applies microeconomic techniques to evaluate the overall well-being (welfare) of a society.

Allocative efficiency is a state of the economy in which production is aligned with the preferences of consumers and producers; in particular, the set of outputs is chosen so as to maximize the social welfare of society. This is achieved if every produced good or service has a marginal benefit equal to the marginal cost of production.

Erik Lindahl was a Swedish economist. He was professor of economics at Uppsala University 1942–58 and in 1956–59 he was the President of the International Economic Association. He was an also an advisor to the Swedish government and the central bank, and in 1943 was elected as a member of the Royal Swedish Academy of Sciences. Lindahl posed the question of financing public goods in accordance with individual benefits. The quantity of the public good satisfies the requirement that the aggregate marginal benefit equals the marginal cost of providing the good.

There are two fundamental theorems of welfare economics. The first states that in economic equilibrium, a set of complete markets, with complete information, and in perfect competition, will be Pareto optimal. The requirements for perfect competition are these:

There are no externalities and each actor has perfect information.

Firms and consumers take prices as given.

The Ramsey problem, or Ramsey pricing, or Ramsey–Boiteux pricing, is a second-best policy problem concerning what prices a public monopoly should charge for the various products it sells in order to maximize social welfare while earning enough revenue to cover its fixed costs.

The Samuelson condition, due to Paul Samuelson, in the theory of public economics, is a condition for optimal provision of public goods.

Competitive equilibrium is a concept of economic equilibrium, introduced by Kenneth Arrow and Gérard Debreu in 1951, appropriate for the analysis of commodity markets with flexible prices and many traders, and serving as the benchmark of efficiency in economic analysis. It relies crucially on the assumption of a competitive environment where each trader decides upon a quantity that is so small compared to the total quantity traded in the market that their individual transactions have no influence on the prices. Competitive markets are an ideal standard by which other market structures are evaluated.

Several theories of taxation exist in public economics. Governments at all levels need to raise revenue from a variety of sources to finance public-sector expenditures.

Fair item allocation is a kind of the fair division problem in which the items to divide are discrete rather than continuous. The items have to be divided among several partners who potentially value them differently, and each item has to be given as a whole to a single person. This situation arises in various real-life scenarios:

In economics and consumer theory, a linear utility function is a function of the form:

This glossary of economics is a list of definitions containing terms and concepts used in economics, its sub-disciplines, and related fields.

Market equilibrium computation is a computational problem in the intersection of economics and computer science. The input to this problem is a market, consisting of a set of resources and a set of agents. There are various kinds of markets, such as Fisher market and Arrow–Debreu market, with divisible or indivisible resources. The required output is a competitive equilibrium, consisting of a price-vector, and an allocation, such that each agent gets the best bundle possible given the budget, and the market clears.

Fair allocation of items and money is a class of fair item allocation problems in which, during the allocation process, it is possible to give or take money from some of the participants. Without money, it may be impossible to allocate indivisible items fairly. For example, if there is one item and two people, and the item must be given entirely to one of them, the allocation will be unfair towards the other one. Monetary payments make it possible to attain fairness, as explained below.

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.