An offshore bank is a bank that is operated and regulated under international banking license, which usually prohibits the bank from establishing any business activities in the jurisdiction of establishment. Due to less regulation and transparency, accounts with offshore banks were often used to hide undeclared income. Since the 1980s, jurisdictions that provide financial services to nonresidents on a big scale can be referred to as offshore financial centres. OFCs often also levy little or no corporation tax and/or personal income and high direct taxes such as duty, making the cost of living high.

A transaction account, also called a checking account, chequing account, current account, demand deposit account, or share draft account at credit unions, is a deposit account or bank account held at a bank or other financial institution. It is available to the account owner "on demand" and is available for frequent and immediate access by the account owner or to others as the account owner may direct. Access may be in a variety of ways, such as cash withdrawals, use of debit cards, cheques and electronic transfer. In economic terms, the funds held in a transaction account are regarded as liquid funds. In accounting terms, they are considered as cash.

Online banking, also known as internet banking, virtual banking, web banking or home banking, is a system that enables customers of a bank or other financial institution to conduct a range of financial transactions through the financial institution's website or mobile app. Since the early 2000s this has become the most common way that customers access their bank accounts.

Account aggregation sometimes also known as financial data aggregation is a method that involves compiling information from different accounts, which may include bank accounts, credit card accounts, investment accounts, and other consumer or business accounts, into a single place. This may be provided through connecting via an API to the financial institution or provided through "screen scraping" where a user provides the requisite account-access information for an automated system to gather and compile the information into a single page. The security of the account access details as well as the financial information is key to users having confidence in the service.

A remittance is a non-commercial transfer of money by a foreign worker, a member of a diaspora community, or a citizen with familial ties abroad, for household income in their home country or homeland. Money sent home by migrants competes with international aid as one of the largest financial inflows to developing countries. Workers' remittances are a significant part of international capital flows, especially with regard to labor-exporting countries.

A payment is the tender of something of value, such as money or its equivalent, by one party to another in exchange for goods or services provided by them, or to fulfill a legal obligation or philanthropy desire. The party making the payment is commonly called the payer, while the payee is the party receiving the payment. Whilst payments are often made voluntarily, some payments are compulsory, such as payment of a fine.

Mobile banking is a service provided by a bank or other financial institution that allows its customers to conduct financial transactions remotely using a mobile device such as a smartphone or tablet. Unlike the related internet banking it uses software, usually called an app, provided by the financial institution for the purpose. Mobile banking is usually available on a 24-hour basis. Some financial institutions have restrictions on which accounts may be accessed through mobile banking, as well as a limit on the amount that can be transacted. Mobile banking is dependent on the availability of an internet or data connection to the mobile device.

Safaricom PLC is a listed Kenyan mobile network operator headquartered at Safaricom House in Nairobi, Kenya. It is the largest telecommunications provider in Kenya, and one of the most profitable companies in the East and Central Africa region. The company offers mobile telephony, mobile money transfer, consumer electronics, ecommerce, cloud computing, data, music streaming, and fibre optic services. It is most renowned as the home of M-PESA, a mobile banking SMS-based service.

Euronet Worldwide is an American provider of global electronic payment services with headquarters in Leawood, Kansas. It offers automated teller machines (ATM), point of sale (POS) services, credit/debit card services, currency exchange and other electronic financial services and payments software. Among others, it provides the prepaid subsidiaries Transact, PaySpot, epay, Movilcarga, TeleRecarga and ATX.

The Internet in Africa is limited by a lower penetration rate when compared to the rest of the world. Measurable parameters such as the number of ISP subscriptions, overall number of hosts, IXP-traffic, and overall available bandwidth are indicators that Africa is far behind the "digital divide". Moreover, Africa itself exhibits an inner digital divide, with most Internet activity and infrastructure concentrated in South Africa, Morocco, Egypt as well as smaller economies like Mauritius and Seychelles. In general, only 24.4% of the African population have access to the Internet, as of 2018. Only 0.4% of the African population has a fixed-broadband subscription. The majority of internet users use it through mobile broadband.

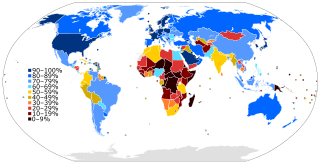

Financial inclusion is the availability and equality of opportunities to access financial services. It refers to a process by which individuals and businesses can access appropriate, affordable, and timely financial products and services which include banking, loan, equity, and insurance products. It is a path to enhance inclusiveness in economic growth by enabling the unbanked population to access the means for savings, investment, and insurance towards improving household income and reducing income inequality

The National Payments Corporation of India is an organization that operates retail payments and settlement systems in India. The organization is an initiative of the Reserve Bank of India (RBI) and Indian Banks’ Association (IBA) under the provisions of the Payment and Settlement Systems Act, 2007, for creating a robust Payment & Settlement Infrastructure in India.

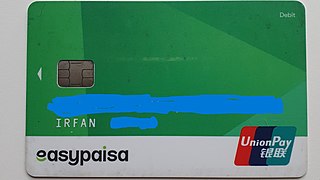

Easypaisa is a Pakistani mobile wallet, mobile payments and branchless banking services provider. It was founded in October 2009 by Telenor Pakistan. It also provides digital payment services through a QR code in partnership with Masterpass and it is the only GSMA mobile money certified service in Pakistan.

Mobile payments is a mode of payment using mobile phones. Instead of using methods like cash, cheque, and credit card, a customer can use a mobile phone to transfer money or to pay for goods and services. A customer can transfer money or pay for goods and services by sending an SMS, using a Java application over GPRS, a WAP service, over IVR or other mobile communication technologies. In India, this service is bank-led. Customers wishing to avail themselves of this service will have to register with banks which provide this service. Currently, this service is being offered by several major banks and is expected to grow further. Mobile Payment Forum of India (MPFI) is the umbrella organisation which is responsible for deploying mobile payments in India.

In financial services, open banking allows for financial data to be shared between banks and third-party service providers through the use of application programming interfaces (APIs). Traditionally, banks have kept customer financial data within their own closed systems. Open banking allows customers to share their financial information securely and electronically with other authorized organizations, such as fintech companies, payment providers, lenders, and other banks.

QIWI plc is a Russian company that provides payment and financial services in Russia and CIS countries. The group includes QIWI payment system, QIWI Bank, CONTACT money transfer system, Factoring PLUS, Flocktory, and RealWeb. The company has representative offices in three countries.

Revolut is a global neobank and financial technology company that offers banking services for retail customers and businesses. Headquartered in London, it was founded in 2015 by Nikolay Storonsky and Vlad Yatsenko. It offers products including banking services, currency exchange, debit and credit cards virtual cards, Apple Pay, interest-bearing "vaults", personal loans and BNPL, stock trading, crypto, commodities, human resources and other services.

Unified Payments Interface, commonly referred as UPI, is an Indian instant payment system developed by the National Payments Corporation of India (NPCI) in 2016. The interface facilitates inter-bank peer-to-peer (P2P) and person-to-merchant (P2M) transactions. It is used on mobile devices to instantly transfer funds between two bank accounts. The mobile number of the device is required to be registered with the bank. The UPI ID of the recipient can be used to transfer money. It runs as an open source application programming interface (API) on top of the Immediate Payment Service (IMPS), and is regulated by the Reserve Bank of India (RBI). Indian Banks started making their UPI-enabled apps available on the Google Play on 25 August 2016.

Simplii Financial is a Canadian direct bank and the digital banking division of the Canadian Imperial Bank of Commerce (CIBC). It offers no-fee chequing and savings accounts, a VISA credit card, Guaranteed Investment Certificates (GICs), mortgages and mutual funds. These savings and investment products are also eligible for registration under a Tax-Free Savings Account (TFSA) or a Registered Retirement Savings Plan (RRSP).

Leora F. Klapper is an American economist who currently works as a lead economist at the World Bank in the Finance and Private Sector research team as part of the Development Research group. Klapper has held government jobs in Washington, DC and Jerusalem, Israel in the Bank of Israel, as well as having held private sector jobs for Peter L. Bernstein and the Salomon Brothers firm in New York. She is also the founder of The Global Findex Database and Entrepreneurship Database.