An economic and monetary union (EMU) is a type of trade bloc that features a combination of a common market, customs union, and monetary union. Established via a trade pact, an EMU constitutes the sixth of seven stages in the process of economic integration. An EMU agreement usually combines a customs union with a common market. A typical EMU establishes free trade and a common external tariff throughout its jurisdiction. It is also designed to protect freedom in the movement of goods, services, and people. This arrangement is distinct from a monetary union, which does not usually involve a common market. As with the economic and monetary union established among the 27 member states of the European Union (EU), an EMU may affect different parts of its jurisdiction in different ways. Some areas are subject to separate customs regulations from other areas subject to the EMU. These various arrangements may be established in a formal agreement, or they may exist on a de facto basis. For example, not all EU member states use the Euro established by its currency union, and not all EU member states are part of the Schengen Area. Some EU members participate in both unions, and some in neither.

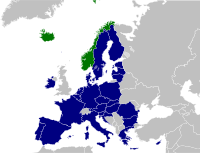

The euro area, commonly called the eurozone (EZ), is a currency union of 20 member states of the European Union (EU) that have adopted the euro (€) as their primary currency and sole legal tender, and have thus fully implemented EMU policies.

The Stability and Growth Pact (SGP) is an agreement, among all the 27 member states of the European Union (EU), to facilitate and maintain the stability of the Economic and Monetary Union (EMU). Based primarily on Articles 121 and 126 of the Treaty on the Functioning of the European Union, it consists of fiscal monitoring of member states by the European Commission and the Council of the European Union, and the issuing of a yearly Country-Specific Recommendation for fiscal policy actions to ensure a full compliance with the SGP also in the medium-term. If a member state breaches the SGP's outlined maximum limit for government deficit and debt, the surveillance and request for corrective action will intensify through the declaration of an Excessive Deficit Procedure (EDP); and if these corrective actions continue to remain absent after multiple warnings, a member state of the eurozone can ultimately also be issued economic sanctions. The pact was outlined by a European Council resolution in June 1997, and two Council regulations in July 1997. The first regulation "on the strengthening of the surveillance of budgetary positions and the surveillance and coordination of economic policies", known as the "preventive arm", entered into force 1 July 1998. The second regulation "on speeding up and clarifying the implementation of the excessive deficit procedure", sometimes referred to as the "dissuasive arm" but commonly known as the "corrective arm", entered into force 1 January 1999.

The euro came into existence on 1 January 1999, although it had been a goal of the European Union (EU) and its predecessors since the 1960s. After tough negotiations, the Maastricht Treaty entered into force in 1993 with the goal of creating an economic and monetary union (EMU) by 1999 for all EU states except the UK and Denmark.

The Executive Vice President of the European Commission for An Economy that Works for People is the member of the European Commission responsible for economic and financial affairs. The position was previously titled Commissioner for Economic and Monetary Affairs and the Euro and European Vice President for the Euro and Social Dialogue from 2014 to 2019. The current executive vice president is Valdis Dombrovskis (EPP).

The first Juncker–Asselborn Government was the government of Luxembourg between 31 July 2004 and 23 July 2009. It was led by, and named after, Prime Minister Jean-Claude Juncker and Deputy Prime Minister Jean Asselborn.

Lúcio Vinhas de Souza is a Brazilian Born-Portuguese economist. His main research areas are global macroeconomics, development economics, monetary economics, finance and country risk, with extensive work experience at the developed economies of the European Union and the US, and in several emerging market regions, from the former Soviet Union to East Asia, Africa and Latin America.

The economic and monetary union (EMU) of the European Union is a group of policies aimed at converging the economies of member states of the European Union at three stages.

Fiscal union is the integration of the fiscal policy of nations or states. In a fiscal union, decisions about the collection and expenditure of taxes are taken by common institutions, shared by the participating governments. A fiscal union does not imply the centralisation of spending and tax decisions at the supranational level. Centralisation of these decisions would open up not only the possibility of inherent risk sharing through the supranational tax and transfer system but also economic stabilisation through debt management at the supranational level. Proper management would reduce the effects of asymmetric shocks that would be shared both with other countries and with future generations. Fiscal union also implies that the debt would be financed not by individual countries but by a common bond.

The Euro-Plus Pact was adopted in March 2011 under EU's Open Method of Coordination, as an intergovernmental agreement between all member states of the European Union, in which concrete commitments were made to be working continuously within a new commonly agreed political general framework for the implementation of structural reforms intended to improve competitiveness, employment, financial stability and the fiscal strength of each country. The plan was advocated by the French and German governments as one of many needed political responses to strengthen the EMU in areas which the European sovereign-debt crisis had revealed as being too poorly constructed.

The European Monetary Agreement (EMA) was an economic arrangement signed by 17 European countries in Paris on the 5th of August 1955. It replaced the European Payments Union which ended in 1958. The EMA was administered by the Organisation for Economic Co-operation and Development (OECD). The OECD did this to achieve economic integration by coordinating the exchange rates of the 17 member countries. This allowed the countries to directly convert their currencies and integrate their balance of payments accounts, which promoted free trade. Due to advanced facilities offered by the International Monetary Fund, the EMA was ended in 1972. The European Economic Community oversaw the EMA aiming to achieve a greater level of economic integration within Europe. The European Economic Community was the legal successor at the time, however it has advanced and is now referred to as the European Union.

The Treaty on Stability, Coordination and Governance in the Economic and Monetary Union; also referred to as TSCG, or more plainly the Fiscal Stability Treaty is an intergovernmental treaty introduced as a new stricter version of the Stability and Growth Pact, signed on 2 March 2012 by all member states of the European Union (EU), except the Czech Republic and the United Kingdom. The treaty entered into force on 1 January 2013 for the 16 states which completed ratification prior to this date. As of 3 April 2019, it had been ratified and entered into force for all 25 signatories plus Croatia, which acceded to the EU in July 2013, and the Czech Republic.

Within the framework of EU economic governance, Sixpack describes a set of European legislative measures to reform the Stability and Growth Pact and introduces greater macroeconomic surveillance, in response to the European debt crisis of 2009. These measures were bundled into a "six pack" of regulations, introduced in September 2010 in two versions respectively by the European Commission and a European Council task force. In March 2011, the ECOFIN council reached a preliminary agreement for the content of the Sixpack with the commission, and negotiations for endorsement by the European Parliament then started. Ultimately it entered into force 13 December 2011, after one year of preceding negotiations. The six regulations aim at strengthening the procedures to reduce public deficits and address macroeconomic imbalances.

The proposed long-term solutions for the Eurozone crisis address ways to deal with the European debt crisis that took place in the European Union from 2009 till the late 2010s, including risks to Eurozone country governments and the Euro.

The Vienna initiative was a plan undertaken in January 2009 by European banks and governments during the height of the financial crisis to control the situation and work towards a joint solution specifically in developing regions of Europe. It has been created to avoid a bank crash that was threatening the region because of the subprime crisis as the liquidity in the CESEE countries depended on the Western ones. It is a forum where the representatives of the private and public economical sector from the Western countries but also Central, Eastern and South-Eastern European countries (CESEE) meet. This Initiative impacted much of those countries, notably Romania.

Pier Carlo Padoan is an Italian economist who served as Minister of Economy and Finance of Italy from 2014 to 2018.

The Troika is a term used to refer to the single decision group created by three entities, the European Commission (EC), the European Central Bank (ECB) and the International Monetary Fund (IMF). It was formed due to the European debt crisis as an ad hoc authority with a mandate to manage the bailouts of Cyprus, Greece, Ireland and Portugal, in the aftermath of their prospective insolvency caused by the world financial crisis of 2007–2008.

The European Semester of the European Union was established in 2010 as an annual cycle of economic and fiscal policy coordination. It provides a central framework of processes within the EU socio-economic governance. The European Semester is a core component of the Economic and Monetary Union (EMU) and it annually aggregates different processes of control, surveillance and coordination of budgetary, fiscal, economic and social policies. It also offers a large space for discussions and interactions between the European institutions and Member States. As a recurrent cycle of budgetary cooperation among the EU Member States, it runs from November to June and is preceded in each country by a national semester running from July to October in which the recommendations introduced by the Commission and approved by the Council are to be adopted by national parliaments and construed into national legislation.

Andrea Montanino is an Italian economist, and business executive, chairman of the Board of Istituto Italiano di Tecnologia and Chief Economist & Sector Strategy and Impact Director of Cassa Depositi e Prestiti.